Basically, construction financing is a simple deal: you bring your own money(equity) and a bank lends you the rest(borrowed capital). You then pay a monthly installment for this loan over many years, which consists of interest and the actual repayment, the amortization. The special thing about it? Your future property serves as collateral for the bank, which usually significantly reduces the interest rate compared to a normal installment loan.

The basic principle of construction financing – simply explained

Imagine your dream home as a huge, sturdy piece of furniture that you really want but can’t afford out of petty cash. Construction financing is like a strong partner who lends a hand. Everyone brings something to the project.

Your share is the equity. This is the money you already have on the high edge. The more of it you bring in, the more stable your foundation is from the outset and the less money you have to borrow. Logical, right?

The missing amount is the borrowed capital – i.e. the loan from the bank. The bank gives you the money because it knows exactly that your property has a high value and will serve as solid collateral if the worst comes to the worst.

What does the borrowed money cost?

Of course, the bank also wants to see something for its money. Your monthly installment that you transfer to the bank is always made up of two parts:

- Interest: This is effectively the “loan fee” for the money. The bank is paid for making the capital available to you.

- Repayment: This is the actual repayment of your loan. With each installment, your mountain of debt shrinks a little and another brick of the house is rightfully yours.

Imagine it like this: Each monthly installment is a brushstroke on the wall of your house. Part of the paint (the interest) goes to the bank as a fee. The other, larger part (the repayment) paints a piece of the house in your personal color – until everything is yours in the end.

This simple interplay of four building blocks is at the heart of every real estate financing solution. Anyone who understands how these cogwheels interlock has already mastered the most important step on the way to home ownership. To get the best conditions, a thorough comparison is the be-all and end-all. Find out more about why a careful comparison can save you money when it comes to real estate financing.

The four pillars of your mortgage at a glance

To make the whole thing even more tangible, let’s take a look at the four main players in an overview. This table summarizes the fundamental components of a mortgage and explains their respective roles in the financing process.

| Component | Function in the financing process | Practical tip |

|---|---|---|

| Equity | Your financial base; reduces the loan requirement and the risk for the bank, which leads to better interest rates. | Try to save at least 20% of the total costs as equity. This is a solid basis. |

| Debt capital | The bank loan that closes the gap between equity and purchase price. | Always obtain several offers. The differences in interest rates over the term can be enormous. |

| Interest | The fee you pay to the bank for lending the money. It is the price you pay for the money. | A long fixed interest rate gives you planning security over many years and protects you from rising interest rates. |

| Repayment | The actual repayment of the loan. The higher the repayment, the faster you will be debt-free. | Start with at least 2% repayment per year. Anything less will unnecessarily prolong the repayment period. |

With this knowledge, you are ideally equipped to not only look at the banks’ offers, but to really understand them and make the right decisions for your project.

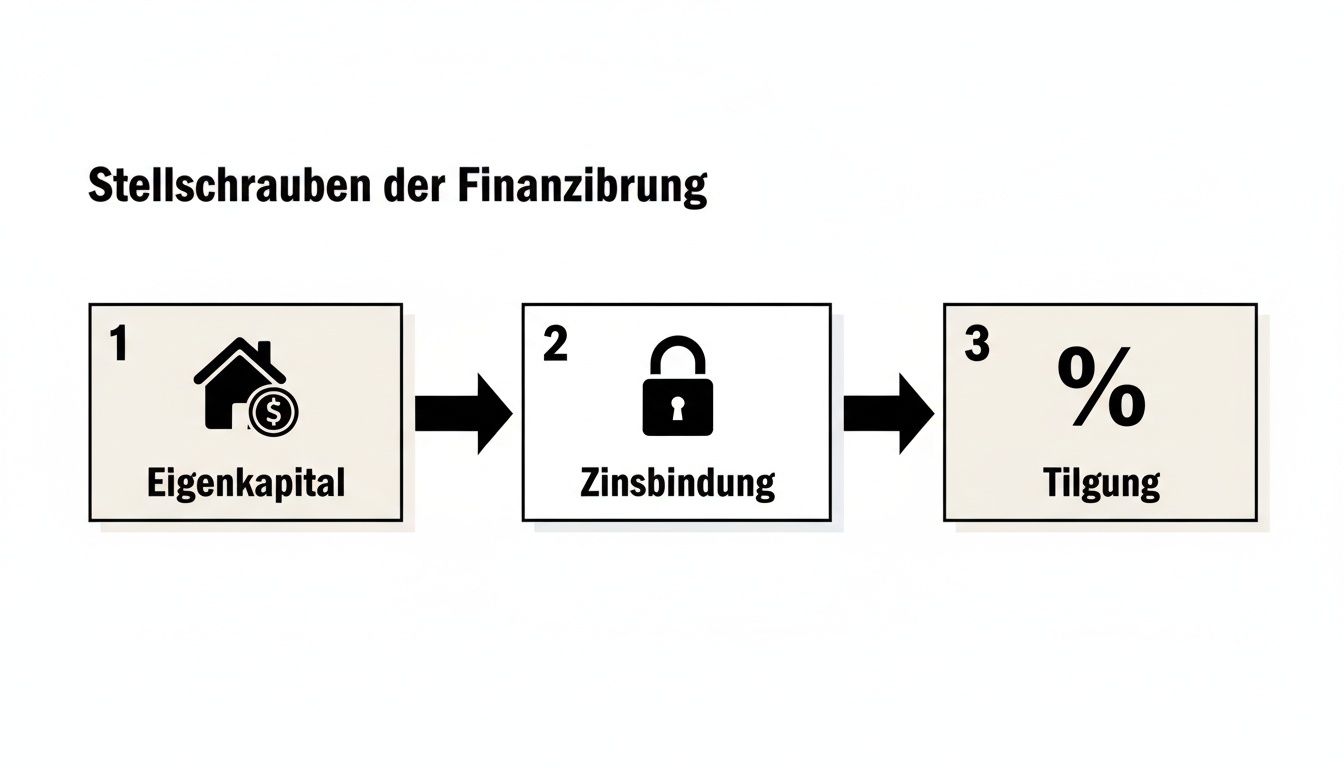

The decisive levers for your financing

So, the basic principle is in place. Now let’s delve a little deeper and take a look at the cockpit of your mortgage. Imagine it like this: You are at the wheel and have a few crucial levers in your hand. You use them to set the course for the coming decades.

These levers are your equity, the fixed interest rate and the repayment. Every single decision here shapes not only your monthly installment, but your entire financial journey. If you really understand these levers, you no longer just read bank offers – you analyze them. You go from being a passenger to being the pilot of your financing.

Equity: your strongest lever

Equity is so much more than just saved money. It is your strongest negotiating lever and a clear signal of trust to the bank. The more of your own money you bring with you, the lower the risk for the financing partner. They will almost always reward you with better interest rates.

The magic limit is often 20% of the total costs, i.e. purchase price plus ancillary costs. If you crack this mark, you usually get significantly more attractive interest rate offers. Why? Because it shows that you are financially disciplined and that your dream of owning your own home is based on a solid foundation.

There are basically two types of equity:

- Hard equity: This is anything that is liquid. This includes traditional savings, overnight and fixed-term deposits, the value of securities accounts or the balance from a building society savings contract.

- Soft equity: This is where the famous “muscle mortgage” comes into play – i.e. your own work on the construction. Even if no money flows here, your own contribution reduces the overall costs. Many banks recognize this as a form of equity.

A decent buffer of equity is your most important tool. It not only gives you a better hand in the interest rate game, but also the necessary security for unforeseen expenses that unfortunately arise from time to time during construction or renovation.

Fixed interest rates: Your protective shield against market fluctuations

The fixed interest rate is basically a price guarantee for borrowed money. You agree a fixed interest rate with the bank for a certain period – usually for 5, 10, 15 or even 20 years. During this time, your monthly installment remains absolutely constant, no matter what happens on the financial markets. Think of it as your personal shield against rising interest rates.

A long-term fixed interest rate is like a long-term rental agreement for your money at a price that is fixed today. It protects you from “rent increases” in the form of interest rate rises and gives you a reliable basis for calculation over many years.

The interest rate trend is the engine that determines how construction financing works in Germany and how high your mortgage will end up being. Current data shows that the average construction interest rate for a 10-year commitment was 3.68 percent in April and 3.82 percent for a 15-year commitment. In May, borrowing rates fluctuated between 3.5 and 4.0 percent, depending on creditworthiness and equity ratio. For the near future, experts are forecasting a corridor of 3.0 to 3.7 percent, which makes the strategic choice of fixed interest rates all the more important. You can find more in-depth insights into the current interest rate landscape in this analysis on Statista.com.

When does which binding make sense?

- Short fixed interest period (e.g. 5 years): This can be an option if you firmly expect interest rates to fall and want to remain flexible. However, be aware of the higher risk.

- Long fixed interest period (e.g. 15 years or longer): Ideal when interest rates are low. This secures you favorable conditions for a very long time and gives you maximum planning security.

Repayment: Your turbo to freedom from debt

The repayment is the part of your monthly installment with which you actively repay the loan. While the interest portion is the fee for the borrowed money and goes to the bank, the repayment portion directly reduces your debt mountain. A higher repayment simply means that you become debt-free more quickly and save a lot of interest over the entire term.

The difference between 1% and 3% initial amortization may not sound like much, but it has a huge impact.

Let’s take a look at an example:

With a loan of €300,000 and 3.5% interest:

- With a 1% repayment: you only pay off € 250 per month of the loan at the beginning. After 10 years, you will still have around €263,000 outstanding.

- With a 3% repayment: you are already paying back € 750 per month. After 10 years, the remaining debt has already fallen to around €204,000.

A higher repayment is the most direct route to debt freedom. Many contracts also allow unscheduled repayments – these are unscheduled payments, for example from a bonus payment or a small inheritance. These act like a real turbo, as they go 100% towards reducing the remaining debt and lower your interest burden immediately. A strategic loan comparison that takes such options into account is therefore essential.

Your path to home ownership step by step

Moving into your own four walls is not a sprint, but rather a well-planned marathon. You don’t make a decision like this overnight. Think of it like a mountain hike: Every step has to be right so that you reach the summit safely. We take you by the hand and guide you through the entire process – from the first vague idea to the moment when you finally hold the key in your hand.

So that the whole thing doesn’t remain so dry and theoretical, we look at the path of a fictitious family, the Müllers. This also makes the technical details tangible and much easier to understand.

Preparation: Cash flow analysis and property search

It all starts with an honest look at their own finances. Before the Müllers even browse through a single real estate ad, they sit down at the kitchen table and take a thorough look at their finances. What comes in each month, what goes out? What budget is really left over for a loan installment? And, very importantly, how much equity is on the high side?

Only when this financial framework was crystal clear did the search for a suitable home begin. This ensured from the outset that they only looked at houses that were really within their budget. This saves a lot of frustration and is the foundation for a successful application to the bank.

The following graphic shows the three main levers you can pull to tailor your financing perfectly to your life situation.

You can see immediately that each of these decisions has a direct influence on how quickly – and at what cost – you achieve your goal.

Compare offers and submit the application

With a dream property in mind, the Müllers obtain offers from various banks and financial brokers. This is a crucial point, because the first offer is rarely the best. They not only look at the interest rate, but also compare details such as the fixed interest rate, repayment amount and whether there are options for special repayments.

The market is on the move again, which makes a comparison all the more important. Demand for home loans is picking up again: In the first quarter, the vdp banks lent 24.4 billion euros for residential real estate – an increase of a whopping 31.9 percent. In the first half of the year as a whole, new business amounted to EUR 70.1 billion, of which EUR 46 billion (+22 percent) was attributable to residential construction alone. This shows that competition among banks has been revived and good conditions can be found. You can find out more about the latest developments on the financing market at pfandbrief.de.

Once the best offer has been found, the Müllers submit the official loan application. This requires a whole folder of documents: proof of income, bank statements, the exposé of the property and a list of their equity. The bank now checks their creditworthiness and the value of the property very carefully. A well-prepared application is worth its weight in gold here.

Notary appointment and land register entry

As soon as the bank gives the green light and sends a financing commitment, the next major milestone is on the agenda: the notary appointment. This is where the buyer and seller sign the purchase contract, which then becomes legally binding. The notary then takes care of all the paperwork.

A notary acts like a neutral arbitrator in real estate transactions. He ensures that the contract is fair for both parties, clarifies all legal pitfalls and initiates the necessary entries in the land register. This ensures that the change of ownership is official and watertight.

A crucial step in this process is the entry of the land charge in the land register. This is the contractually agreed security for the bank. Only when the land charge has been registered does the bank have its security and pay out the loan – not a day earlier.

Disbursement of the loan

The money rarely flows all at once. When buying an existing property, the bank transfers the full purchase price directly to the seller, but only once the notary has confirmed that all conditions in the purchase contract have been met.

Things work differently for new builds. Here, the payment is made bit by bit, depending on the progress of construction. The bank only pays for what has already been completed – for example, when the shell of the building is finished or the windows have been installed. For the part of the loan that has not yet been drawn down, so-called commitment interest may be incurred. However, this process protects both sides, the builder and the bank, from financial risks.

With the last installment and the handing over of the keys, the exciting journey of construction financing ends and a whole new chapter in your own home begins. If you want even more security for your application, read our tips and tricks for a successful loan application.

What this means in practice: two families, two paths to home ownership

Theory is all well and good, but it’s only when you see how interest, repayment and equity are turned into a specific monthly installment that the topic of mortgage financing comes to life. No more dry figures! Let’s run through the whole thing using two typical examples from real life.

This will give you a feel for how your own decisions shape your financing – from the monthly charge to the residual debt in ten years’ time.

Scenario 1: The young family and the terraced house

Imagine the Schmidt family: two adults, one small child. Their dream is a second-hand terraced house for €400,000. They have saved consistently over the last few years and now have an impressive €60,000 in equity. That’s 15% of the purchase price.

The bank makes them an offer with a borrowing rate of 3.8% per year. In order to remain financially flexible at the beginning, the Schmidts choose an initial repayment of 2%.

Let’s take a look at the bill:

- Loan amount: € 400,000 purchase price – € 60,000 equity = € 340,000

- Annual interest costs: € 340,000 × 3.8 % = € 12,920

- Annual repayment: € 340,000 × 2.0 % = € 6,800

- Monthly installment: (€12,920 + €6,800) / 12 = €1,643

After the fixed interest period of ten years, the Schmidt family has already paid off a good portion of their loan. The remaining debt then amounts to around € 264,500.

Scenario 2: The experienced couple builds energy-efficiently

Now let’s take a look at the Müllers. Both in their mid-40s and financially stable, they are planning an energy-efficient new build for a total of €550,000. Their financial cushion has grown over the years, and they can use €150,000 of equity – that’s almost 27.3% of the total costs. This high proportion naturally secures them significantly better conditions with the bank.

Clever as they are, they also take advantage of a KfW subsidized loan of €50,000 at an extremely low interest rate.

State subsidies such as those from KfW are not a handout, but a real strategic tool. They noticeably reduce the interest burden and make energy-efficient construction projects in particular really worthwhile. Used correctly, they can reduce the total cost of financing by many thousands of euros.

For the remaining main loan of € 350,000, they get a top interest rate of just 3.4 % thanks to their high equity. Because they can afford it and want it, they choose a sporty initial repayment of 3%. Their goal: to be debt-free as quickly as possible.

The calculation for your main loan looks like this:

- Loan requirement: € 550,000 costs – € 150,000 equity – € 50,000 KfW = € 350,000

- Annual interest costs: € 350,000 × 3.4 % = € 11,900

- Annual repayment: € 350,000 × 3.0 % = € 10,500

- Monthly installment: (€ 11,900 + € 10,500) / 12 = € 1,867

After ten years, the residual debt here has already fallen to around € 236,200. The installment may be higher, but the mountain of debt is melting much faster. If you are interested in forms of financing that go beyond traditional construction financing, you will find valuable insights here: read more about the art of financing in our guide to installment loans.

The two scenarios in direct comparison

These two stories make one thing very clear: the equity and repayments are decisive for how your financing will look in the end. The following table summarizes the most important key data once again.

Comparison of financing scenarios

Here you can see how different starting positions (equity, repayment rate) affect the monthly installment and the residual debt.

| Scenario | Purchase price | Equity | Interest rate | Initial repayment | Monthly installment | Residual debt after 10 years |

|---|---|---|---|---|---|---|

| The Schmidt family | 400.000 € | 60.000 € (15 %) | 3,8 % | 2,0 % | 1.643 € | approx. 264,500 € |

| The Müllers | 550.000 € | 150.000 € (27,3 %) | 3,4 % | 3,0 % | 1.867 €* | approx. 236,200 € |

| *plus the separate installment for the KfW loan |

The conclusion is clear: more equity brings better interest rates. A higher repayment accelerates the path to debt freedom enormously – even if this means a higher monthly burden. It is always a question of weighing up the current financial burden against the long-term goal.

Using state subsidies as a financing joker

Fortunately, you don’t have to shoulder the burden of your mortgage alone. Just think of the state as a silent partner that plays you a real financing joker – provided you know the right cards. There is a whole range of subsidy programs that can significantly reduce your financial burden and make the dream of owning your own home, which might otherwise seem unattainable, within reach.

This section is intended to be your personal guide through the German funding jungle. We will show you how you can tap into this valuable support for your project.

KfW as your most important partner

The Kreditanstalt für Wiederaufbau (KfW) is almost always at the heart of state funding. It is the first and most important point of contact for most builders and buyers. Its programs are designed to provide targeted support where it makes the most sense.

The system behind it is quite clever: KfW does not give you the loan directly, but channels it through your house bank. The result for you? A loan with extremely favorable interest rates or even hefty repayment subsidies that you don’t have to pay back. These building blocks are then simply integrated seamlessly into your main financing.

The focus is on two areas in particular:

- Energy-efficient construction and renovation: If you build sustainably or upgrade the energy efficiency of an old property, the state rewards you with top conditions.

- Home ownership for families: Special programs are designed to make it easier for families with children to buy their own home, usually by means of heavily subsidized loans.

Very important to know: With almost all subsidies, timing is everything. The application must always be submitted before the purchase contract is signed or the first sod is turned. If you try to do it later, the train has usually left the station.

Thinking outside the box: don’t forget regional programs

In addition to the nationwide KfW programs, it is also worth taking a closer look at what your federal state has to offer. Many state banks have their own funding pots, which are often overlooked but can make a huge difference. These are often linked to certain income limits or family size.

Especially now that the demand for financing has recovered after the interest rate fluctuations, such subsidies are more attractive than ever. A major broker such as Baufi24 recently reported a record volume of EUR 2.63 billion – a growth of 39.1 percent compared to the previous year. Between 2023 and 2025, the brokered volume even more than doubled. This shows how dynamic the market is and how important it is to really know every financing component in order to secure the best conditions. You can read more about this development in an article about the current record growth in the financing market at cash-online.de.

Careful research is worth its weight in gold here. An experienced financial advisor not only knows the KfW classics, but also has the regional particularities on screen and can thus put together a tailor-made package for you. Ask specifically and use every joker available to you.

Typical risks and how to avoid costly mistakes

A mortgage is one of the biggest decisions you will make in your life. That’s no exaggeration – it’s a commitment that will stay with you for decades. Think of it like a long sea voyage: With a good map and knowledge of potential storms, you will arrive safely in port. But if you set sail blindly, you run the risk of running aground.

So let’s talk openly about the pitfalls that need to be avoided. The good news first: there is a suitable strategy for each of these risks. It’s not about scaring you, but about making you the confident captain of your own financing.

The sword of Damocles at the end of the fixed interest period

Perhaps the biggest and often underestimated risk lurks at the end of your fixed interest period. After 10, 15 or perhaps 20 years, there is usually still a considerable residual debt. You will need follow-up financing for this amount – and nobody knows what the interest rates will then be.

A simple example: You took out your financing at a great interest rate of 3%. At the end of the fixed interest period, however, market interest rates have climbed to 6%. Suddenly, the interest portion of your installment doubles. This can quickly mean an additional monthly charge of several hundred euros and throw your entire household budget out of kilter.

A forward loan is basically like an umbrella that you buy on a sunny day. You secure today’s, perhaps very favorable interest rates for the future – up to five years in advance. So you can sleep soundly even when a storm is brewing on the financial market.

Life doesn’t always go according to plan: unexpected costs and personal risks

Another major risk are events that simply throw your careful calculations out of kilter. These can be roughly divided into two areas:

- Buffer, buffer, buffer: I cannot emphasize this often enough: Unforeseen costs always crop up when building or renovating. So plan a buffer of at least 10 % to 15 % of the construction costs right from the start. Nothing is more frustrating than running out of money before the painters have arrived.

- Protection against the uncertainties of life: what happens if the main breadwinner suddenly falls seriously ill or loses their job? Term life insurance and occupational disability insurance are not just nice extras, they are the safety net for your family and your home. They ensure that, in the worst-case scenario, your dream of owning your own home is not dashed.

In order to protect your investment in the long term and avoid potential mistakes in wealth planning, it can also make sense to look at more complex real estate concepts. Usufruct in real estate can be an interesting option to secure assets across generations.

With well thought-out planning that includes financial reserves and the right insurance cover, your construction financing will go from a risk to a rock-solid foundation for your future. Other valuable financing tips to minimize risks will help you to really think of everything.

The most frequently asked questions about construction financing: answers from the field

The dream of owning your own home is exciting, but also raises many questions. This is completely normal. To give you a little clarity along the way, I’ve put together the answers to the most frequently asked questions that I come across time and again in my day-to-day work. Think of it as your own personal cheat sheet.

How much equity do I really need?

There is no fixed rule, but I can say from practical experience that a good basis is 20% of the total costs, i.e. purchase price plus ancillary costs. Why? Because the banks see this as a signal that you are financially sound.

They often reward this with noticeably better interest rates. More equity therefore not only means less debt and a lower monthly installment for you, but it also makes your entire loan more affordable.

What happens when the fixed interest period ends?

Hardly any property is completely paid off after the first fixed interest period – let’s say after 10 or 15 years. What remains is the residual debt. And for this you need follow-up financing.

You then have two options: Either you extend the contract with your old bank (this is called a prolongation) or you look around the market and switch to a provider with better conditions (this is debt restructuring). My tip: start early, preferably one or two years before the contract expires. That way you won’t be under time pressure.

Many people underestimate the interest rate risk associated with follow-up financing. If market interest rates have risen in the meantime, the new installment can suddenly be significantly higher. With a forward loan, you can secure today’s possibly lower interest rates for the future. This gives you enormous planning security.

What documents does the bank want to see from me?

It’s simple: the bank wants to know who it is lending its money to and for what. Good preparation is half the battle here and speeds up the whole process immensely. The best thing to do is to create a folder with:

- Documents for you: identity card, the last three payslips and your last income tax statements.

- Proof of your money: account statements showing your equity – whether from a savings account, call money or a custody account.

- Documents relating to the house: The exposé, a current extract from the land register, the building plans and the calculation of the living space.

Can I change the rate later if something happens to me?

Yes, you can, but only if you agree this in the contract from the outset. Pay attention to two important keywords that can give you a lot of leeway later on:

- Special repayments: This is permission to put extra money into the loan in addition to the normal installment. Perfect if you receive a bonus payment or a small inheritance.

- Repayment rate change: Some banks allow you to change the repayment rate once or twice during the term free of charge. Super practical if you have more money after a salary increase or if you want to temporarily reduce the installment while on parental leave.

These two building blocks are worth their weight in gold when it comes to being able to react flexibly to life. So don’t just compare offers according to the interest rate, but also according to these options.

Would you like to know which financing really suits you and your plans? At Finanz-Fox, we translate the small print for you, compare understandable offers and are personally at your side – from the initial idea to handing over the keys. Find your tailor-made construction financing on finanz-fox.de now.