When you deal with loans, you inevitably stumble across two terms: borrowing rate and effective interest rate. At first glance, they may seem similar, but the difference is huge – and can end up costing you a lot of money.

The real crux of the matter lies in what these two interest rates contain. You could say: one shows only half the truth, the other the whole picture.

Why are there two interest rates at all?

It is no coincidence that banks have to provide two interest rates at the same time and certainly not an attempt to confuse you. On the contrary: it is a legal requirement designed to ensure greater clarity and fairness. The idea behind this is to provide you, the borrower, with a truly honest picture of the total costs.

Think of the borrowing rate (sometimes also called the nominal interest rate) as the net price of a product. It indicates how much the bank charges just for lending the money – i.e. the pure interest on the loan amount. Because this interest rate is lower, it is of course often emphasized in marketing. It simply looks more tempting.

The APR, on the other hand, is the gross price. It is the honest price tag of the loan. It includes not only the pure debit interest, but also all other costs that are necessarily associated with the loan. These can be, for example, processing fees, costs for a mandatory account or brokerage commissions.

What really matters when comparing loans

This is the crux of the matter: a low borrowing rate can mislead you if the additional costs are high. The supposedly favorable offer then quickly turns out to be expensive fun.

There is therefore only one reliable parameter for a fair and realistic comparison of different loan offers: the effective interest rate. Only this shows you what the loan will really cost you per year in the end.

Fortunately, you don’t have to worry about this. The legislator has created clear rules with the Price Indication Ordinance (PAngV). Banks in Germany are obliged to always state the APR prominently. This protects us consumers and creates a comparable basis.

To get to the heart of the differences, here is a brief overview.

Debit interest vs effective interest rate at a glance

This direct comparison of the core features helps you to immediately identify the key differences and correctly evaluate loans.

| Feature | Debit interest | Effective interest rate |

|---|---|---|

| What’s inside? | Only the pure interest on the amount borrowed. | Debit interest plus all mandatory ancillary costs. |

| What is it good for? | Used to calculate the pure interest burden per month. | Shows the real total costs of the loan per year. |

| For the comparison? | Absolutely unsuitable, as it hides costs. | The only reliable indicator for a fair comparison. |

| How high is it? | Almost always lower and therefore looks more attractive. | Practically always higher than the borrowing rate. |

In short: the borrowing rate is the decoy, the effective interest rate is the truth. Always pay attention to the effective interest rate for every offer – it’s your best friend when comparing loans.

Understanding the debit interest rate and its drivers

In a way, the borrowing rate is the price tag for borrowed money, but how does this price actually come about? It’s best to think of it as the pure “rent” you pay to the bank. However, this interest rate is only the basis – it is shaped by many invisible forces before other costs are added that ultimately make up the difference between the borrowing rate and the effective interest rate.

These forces can be divided into two large camps: Firstly, there are the external market factors, over which none of us have any influence. And then there is your very personal, individual situation. In the end, these two factors together decide which borrowing rate the bank proposes to you.

What drives interest rates in the background

Above all, the general interest rate environment sets the pace. The most important conductor in this orchestra is clearly the key interest rate of the European Central Bank (ECB).

If the ECB raises the prime rate, the banks also have to pay more to borrow money. They naturally pass these additional costs on to their customers in the form of higher borrowing rates. The reverse is also true: if the ECB lowers the prime rate, there is a good chance that loans for us consumers will also become cheaper again.

Your financial situation is the decisive factor

However, your personal circumstances have a much more direct and tangible influence on the borrowing rate. For the bank, this is nothing more than a risk assessment: how certain is it that it will get its money back?

The most important parameters are

- Your creditworthiness: this is the absolute linchpin. A clean SCHUFA score and impeccable payment history are a signal to the bank that you are a reliable partner. They reward this with a lower borrowing rate.

- Your income: A stable, high income – preferably from a permanent job – gives the bank a lot of peace of mind and reduces the risk of default.

- Loan amount and term: Even the key data of the loan have an influence. Longer terms mean a longer risk for the bank, which is often reflected in a slightly higher borrowing rate.

Let’s assume: Two people need a loan of 15,000 euros. Person A has a top SCHUFA score and a secure, high salary. Person B is getting by on a fixed-term contract and their credit score is only average. Although they both request exactly the same amount, person A will almost certainly be offered a significantly lower borrowing rate. The risk for the bank is simply much lower.

This small example makes it clear that the borrowing rate is anything but a one-size-fits-all figure. It is a value that is individually tailored to you. Find out how you can improve your financial situation to get the best conditions for installment loans in our comprehensive guide.

What makes the effective interest rate the true cost

The borrowing rate is often the first thing that catches the eye in a loan offer – nice and low and tempting. But the truth about the total cost of a loan is told by another figure: the effective interest rate. It is almost always higher, and for good reason. It is the honest price tag that summarizes all mandatory costs.

The decisive difference between the borrowing rate and the effective interest rate therefore lies precisely in these additional costs. You could say that the borrowing rate is the pure “rent” for the money borrowed. The effective interest rate adds on everything else that the bank charges as mandatory fees.

What costs are included in the effective interest rate?

The list of possible costs that make a loan more expensive can be quite long and differs from bank to bank. If you understand the various items, you can estimate the financial burden much better. A good example of how the true costs are made up can be found in the analysis of Amex costs, including annual fees, hidden charges and interest.

The typical suspects that drive up the effective interest rate include:

- Processing fees: Although the Federal Court of Justice has put a stop to this for normal consumer loans, they can still be charged for other types of loan.

- Account management fees: Some banks link the loan to the condition of holding a special, chargeable account with them.

- Intermediary commissions: If a credit broker is involved, their costs must also be taken into account.

- Disagio (payout discount): A nasty trick. You don’t get the full loan amount paid out, but have to pay interest and repay the full amount. This difference noticeably increases the effective costs.

- Insurance premiums: You have to take a close look here. Only if insurance, such as residual debt insurance, is a mandatory requirement for taking out a loan will its costs be included in the effective interest rate.

An important practical tip: Optional additional services, such as voluntary residual debt insurance, do not have to be shown in the effective interest rate. Nevertheless, they can massively increase the total cost of your loan. Therefore, always ask specifically which services are mandatory and which you can confidently decline.

An example from everyday life

Imagine you find an offer for an installment loan of 10,000 euros with a term of 60 months. The advertised borrowing rate is a super-favorable 4.0 percent. Sounds fantastic, doesn’t it?

But a look at the effective interest rate reveals the whole truth: it is 4.13 percent. This difference is no coincidence. While the borrowing rate only shows the pure interest costs, the effective interest rate includes all other obligatory items such as a processing fee or a discount.

This small difference of 0.13 percentage points may seem like a trifle at first glance. However, over the entire term of five years, it adds up to a noticeable amount. This is precisely why it is a legal requirement to state the annual percentage rate of charge. It creates a transparent and fair basis for comparison and protects you as a consumer from hidden costs. This is the only way you can really judge which offer is the most favorable at the end of the day.

How the effective interest rate is calculated

The formula for the effective interest rate often looks quite intimidating at first glance, I know. But don’t let that put you off! Basically, there is a very simple logic behind it: you simply add up all the costs incurred for the loan and spread them over the entire term. The result is then an honest, comparable annual interest rate.

In Germany, the procedure for this is even laid down by law – the so-called uniform method. It ensures that banks cannot cheat and that all offers play by the same rules. This is what makes a fair comparison possible in the first place. You don’t have to become a financial mathematician to do this, but it helps tremendously to develop a feel for how a temptingly low borrowing rate ultimately turns into the real total costs.

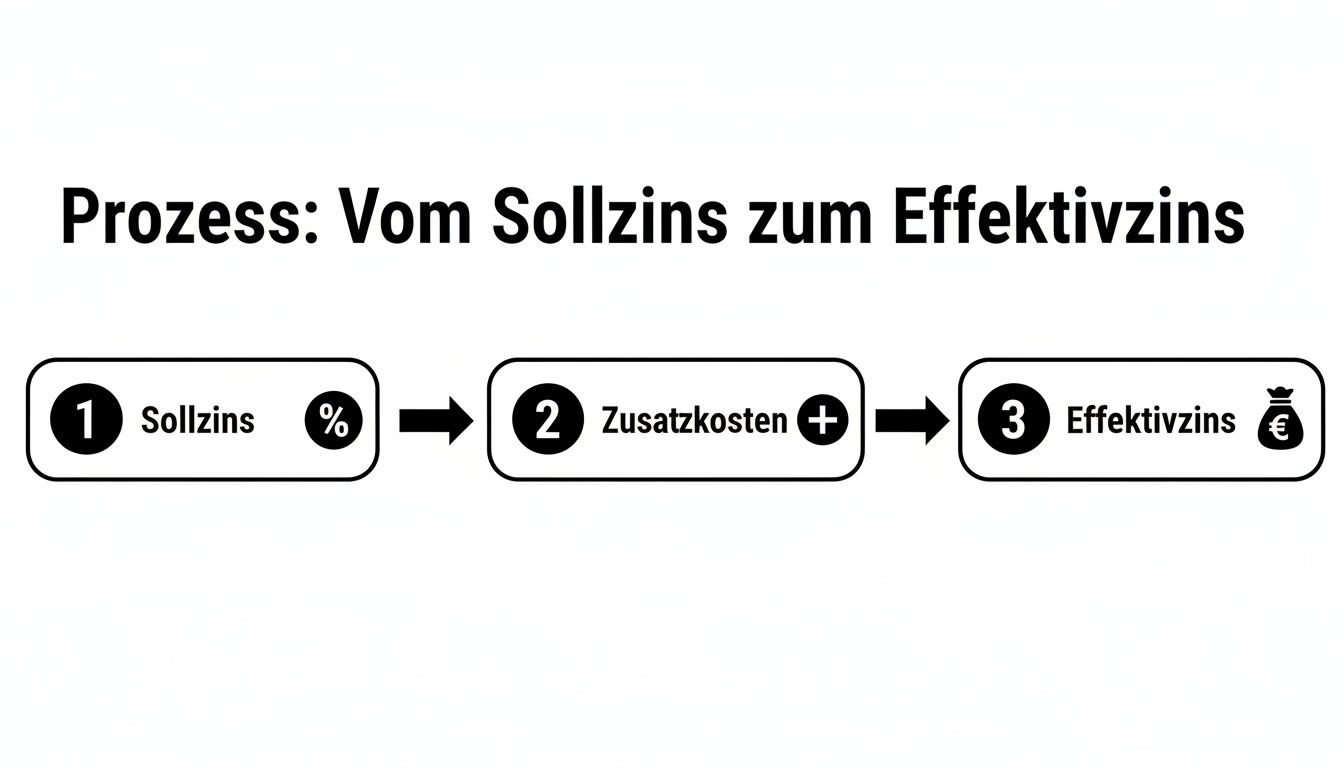

It is precisely this path from pure interest to the true costs that is the decisive point.

The graphic sums it up: the effective interest rate is always the result of the borrowing rate and all additional costs.

The formula explained step by step

The uniform method can of course also be put into a formula. Even if you never have to calculate it yourself, it helps you to really internalize the difference between the borrowing rate and the effective interest rate:

Effective interest rate = (loan costs × 2400) / (net loan amount × (term in months + 1))

Don’t panic, let’s take a look at the building blocks at our leisure:

- Loan costs: This is the total sum of all interest over the entire term plus all additional costs incurred (think of processing fees or a discount).

- Net loan amount: This is the amount that actually ends up in your account. If a discount has been agreed, this amount is smaller than the actual loan amount.

- Term in months: Pretty self-explanatory – the full duration of your loan.

- The factor 2400: This figure is simply an integral part of the formula. It ensures that a correct annual value is obtained at the end.

A brief example makes it more tangible: Imagine you borrow 10,000 euros(net loan amount). The borrowing rate is 4 percent and the term is 60 months. If you plug these figures into the formula, you get an effective interest rate of exactly 4.13 percent. This is the true price tag of your loan.

This small example shows you why even tiny fees or minimal interest rate adjustments can noticeably change the effective interest rate.

Especially for consumers who – like most users here at Finanz-Fox – are looking for an installment loan or mini loan, this knowledge is worth its weight in gold. It enables you to assess offers not only according to the advertised interest rate, but also according to the real costs. So when you compare current interest rates, always look at this value. Because in the end, the only thing that counts is what you actually pay at the end of the day – and only the APR can tell you that reliably.

When it comes to construction financing, it’s all about the bottom line: Why the difference in interest rates is crucial here

With a small installment loan, the difference between the borrowing rate and the effective interest rate may be annoying, but it is usually financially manageable. The situation is completely different with construction financing. Here we are talking about high six-figure amounts and terms that extend over decades. A small, subtle difference suddenly becomes a decisive factor for your financial success. Even tiny differences can add up over the years to sums that can bring tears to your eyes.

The reason for this is the many additional costs that come with real estate loans in particular. These additional costs flow directly into the effective interest rate and make it the only honest comparative figure. At Finanz-Fox, we arrange financing for construction, renovation or follow-up financing on a daily basis and see how dramatic the difference can be. An example: If the average effective interest rate for a 10-year fixed interest rate in November 2025 was 3.56 percent, this already included additional costs of around 273 euros per 100,000 euros loan. These costs show you the true price of money – and this is far higher than the pure borrowing rate. You can find out more about the current interest rate trend for mortgage loans in this overview.

What drives up the effective interest rate for construction financing

Unlike a straightforward consumer loan, some very specific items come into play with a home loan. It is precisely these factors that drive up the effective interest rate:

- Land register and notary costs: This is not an option, but a must. The land charge must be entered in the land register as security for the bank, and that costs money.

- Commitment interest: If you buy an existing property, you usually draw down the loan in one go. However, if you are building, the money often flows in stages, depending on the progress of construction. The part of the money that the bank has “reserved” for you but not yet paid out is subject to commitment interest.

- Valuation fees: Before the bank lends you money, it wants to know what the property is worth. The costs for this appraisal are often passed on to the borrower.

Let’s imagine a very concrete scenario: A loan for 350,000 euros, fixed for 15 years. What at first glance appears to be a tiny difference of just 0.2 percentage points between the borrowing rate of one offer and the effective interest rate of another can add up to an additional charge of over 10,000 euros over the entire fixed interest period.

This example makes it clear why it is an expensive mistake to be blinded by the low borrowing rate for such long-term projects. The effective interest rate is not a marketing gimmick, but the only honest price tag for your dream home. A thorough comparison is therefore essential, especially when it comes to real estate financing, to avoid paying thousands of euros more than necessary in the end.

How to compare credit offers correctly

Now that you know the crucial difference between the borrowing rate and the effective interest rate, you are ready for the real world. The most important rule when comparing loans is actually quite simple, but absolutely crucial: leave the borrowing rate to one side and concentrate fully on the APR. Only this figure will show you what the loan will really cost you in the end.

Banks must always provide a so-called representative example in their offers in accordance with Section 17 of the Price Indication Ordinance (PAngV). This example shows the effective interest rate that at least two thirds of all customers receive for a particular loan. Take a close look at this figure – it is your most realistic anchor point.

Beware of hidden costs

A frequent stumbling block are optional additional products that drive up the total costs considerably, but do not have to appear in the effective interest rate. The classic product par excellence is residual debt insurance.

It may be justified in some situations, but in the vast majority of cases it is not compulsory. However, the costs can be considerable and increase your monthly rate significantly. Therefore, always ask directly which services are optional and what is really necessary for the contract.

A low effective interest rate is only half the battle. You can recognize a really good loan offer by the combination of a low effective interest rate and fair, flexible contract terms.

In order to evaluate offers with confidence, it is best to proceed with a small checklist in mind. In addition to the effective interest rate, be sure to pay attention to these points in order to put together the best overall package for you:

- Special repayment options: Can you transfer additional money free of charge to get rid of the loan more quickly?

- Installment breaks: Is there an option to suspend one or more installments in the event of a financial bottleneck?

- Contract flexibility: Is it possible to adjust the installment amount during the term if your situation changes?

If you keep these factors in mind, you won’t just find an offer that looks good on paper, but financing that really suits your life. A comprehensive loan comparison is the key to finding the best deal and saving money in the end.

Still have questions? Here are the answers.

After all this information, you often still have a few specific questions buzzing around in your head. No problem, that’s completely normal. Let us clear up the most common uncertainties about the borrowing rate and effective interest rate so that you can feel absolutely certain.

Is the borrowing rate really always lower than the effective interest rate?

Yes, in practice you can be sure of this. Theoretically, both interest rates could be identical, but only if a loan had absolutely no additional costs – i.e. no processing fees, no discount, simply nothing. However, you will hardly find such an offer in the real world.

So remember a simple rule of thumb: the effective interest rate is almost always higher. It is the more honest interest rate because it is more complete.

What interest rate determines my monthly installment?

This is an important point that often causes confusion. Your monthly installment, i.e. the amount that is debited from your account, is actually calculated on the basis of the borrowing rate. It determines how the installment is made up of repayment and interest.

However, the effective interest rate is the decisive factor in comparing the true total costs of loans. Because it allocates all additional costs to one year, it shows you which offer will cost you the least at the end of the day.

A quick practical tip: the bank uses the borrowing rate to calculate your installment. You use the effective interest rate to work out which offer is best for you.

Can the interest rates actually change during the term?

It all depends on the contract. With most installment loans and construction financing, you agree a fixed interest rate. This means that the borrowing rate and effective interest rate remain unchanged for the entire agreed term – giving you planning security.

The situation is different for loans with variable interest rates, such as overdraft facilities. Here, the bank can adjust the interest rate in line with general market developments.

Why are some costs missing from the effective interest rate?

The legislator has clearly defined which costs are included in the effective interest rate: namely all costs that are absolutely necessary to obtain the loan.

What is not included are optional items. Voluntary residual debt insurance, for example, or fees for an unscheduled unscheduled repayment are not included. Therefore, always actively ask during the consultation what additional costs may be incurred. This is the only way to get a complete picture of your financial burden.

Ready to put this knowledge into practice and find the best offer for your project? We at Finanz-Fox are here to help you. With our loan calculator, you can immediately see what’s important and our experts are on hand to help you. Compare real offers now and make a smart decision at https://www.finanz-fox.de.