Yes, debt restructuring is possible despite a negative Schufa entry. What’s more, it is often the smartest step to free yourself from the interest trap of expensive old loans. Even if your bank may turn you down, there are specialized providers and brokers who take a different approach. They don’t just look stubbornly at your Schufa score, but assess your financial situation more holistically, for example by using alternative collateral. The aim is always the same: to turn many expensive installments into a single, affordable installment and give you financial breathing space again.

How debt restructuring really works despite negative credit rating

A negative Schufa entry can feel like you’ve landed in a financial cul-de-sac. It becomes particularly overwhelming when old loans with outrageously high interest rates tear a deep hole in your budget every month. But there is a pragmatic way out that will make it easier for you to breathe again.

The logic behind debt restructuring is actually quite simple: you take out a new loan to pay off all your expensive old loans in one go. Ideally, the new loan will have significantly better conditions.

Just imagine what often comes together:

- The expensive overdraft facility, where interest rates often climb above 12%.

- An old installment loan that you took out years ago on bad terms.

- Several credit cards where you have lost track of the outstanding amounts.

Each of these debts has its own installment, interest rate and maturity date. Debt restructuring packs all of this into a single, clear package.

The tangible advantage in everyday life

The result is immediately noticeable: in the end, you only have one single installment to transfer each month and only one contact person. This not only reduces mental stress, but in the best-case scenario also lowers your monthly burden in concrete terms.

A Schufa entry is not a final judgment. Think of it as an impetus to reorganize your finances. Clever debt restructuring is often the first and most important step in regaining control.

An example taken from life

Let’s take a family that struggles every month: €150 goes towards the overdraft, €200 towards an old consumer loan and another €100 towards credit card debt. That’s €450 going to three different places.

Thanks to a debt restructuring loan, which was approved despite the Schufa problems, they were able to bundle these three items. Their new, single installment is now €380. The bottom line is that you not only save €70 per month, but you finally have an overview again. In our guide, we show you how you can improve your dealings with Schufa.

Unfortunately, such situations are not uncommon. The number of over-indebted people in Germany is rising, and with it the need for intelligent solutions. According to Creditreform’s Debtor Atlas Germany, 5.67 million people over the age of 18 are considered over-indebted. Many of them only have to deal with a handful of creditors – debt restructuring is often the perfect tool to reduce the financial burden. If you would like to read the details, you can find out more about current developments in the Debtor Atlas 2025 directly from Creditreform.

An honest look at your finances – the be-all and end-all for your success

Before you even think about comparing offers or filling out applications, we need to get down to the basics. The very first and most important step is to take stock of your finances. This is about being truly honest with yourself and being able to realistically assess your income situation. Without this clarity, any attempt at debt restructuring is doomed to failure from the outset.

Sit down and take a look at your accounts. It may sound trivial, but a complete budget statement is worth its weight in gold. Simply grab your bank statements for the last three months and list everything – without embellishing anything. The point is not to reproach yourself, but to create a solid data basis.

A simple comparison is often enough:

- What goes in? Your net salary, any child benefit, rental income, etc.

- What must be removed (fixed)? Rent, electricity, gas, insurance and of course the installments on your current loans.

- What else goes away (variable)? Expenses for food, the car, leisure activities, clothing.

This honest look shows you in black and white how much air you really have at the end of the month. It is often frighteningly little. A good budget planning guide can help you to uncover the hidden “money guzzlers”.

Your Schufa report: Understand, check and clear up

At the same time, you should take care of your Schufa information. Once a year, you can request a copy of this data free of charge – a right that you should definitely make use of. Once you have the document in front of you, the real detective work begins. Because not every negative entry is a knock-out criterion.

Banks often talk about “soft” and “hard” negative features here. A forgotten invoice that you paid quickly is usually a soft feature. A defaulted loan, a court order for payment or even an affidavit, on the other hand, are much more serious. These are the hard facts that make a loan approval extremely difficult.

Take the time to check every single entry in your credit report. Incorrect or outdated data can unnecessarily worsen your creditworthiness and can be corrected.

And what if you discover an error? Then you need to take action immediately. Perhaps there is an old claim listed that you have long since paid, but which is still considered outstanding. This happens more often than you might think.

This is how you proceed with a correction:

- Secure evidence: Dig out the transfer receipt or the creditor’s written confirmation that everything has been settled.

- Confront the creditor: Ask the company in writing to report the entry to Schufa as “completed” and to initiate the deletion. Set a deadline.

- Inform Schufa: At the same time, send a copy of your evidence directly to Schufa. Ask for the incorrect entry to be checked and corrected.

This process can take a few weeks, but the effort is worth it a thousand times over. A clean Schufa entry can dramatically improve your chances of getting a fair debt restructuring loan despite Schufa. This is often the lever that separates an approval from a rejection. Only when you have done this homework are you really ready for the next steps.

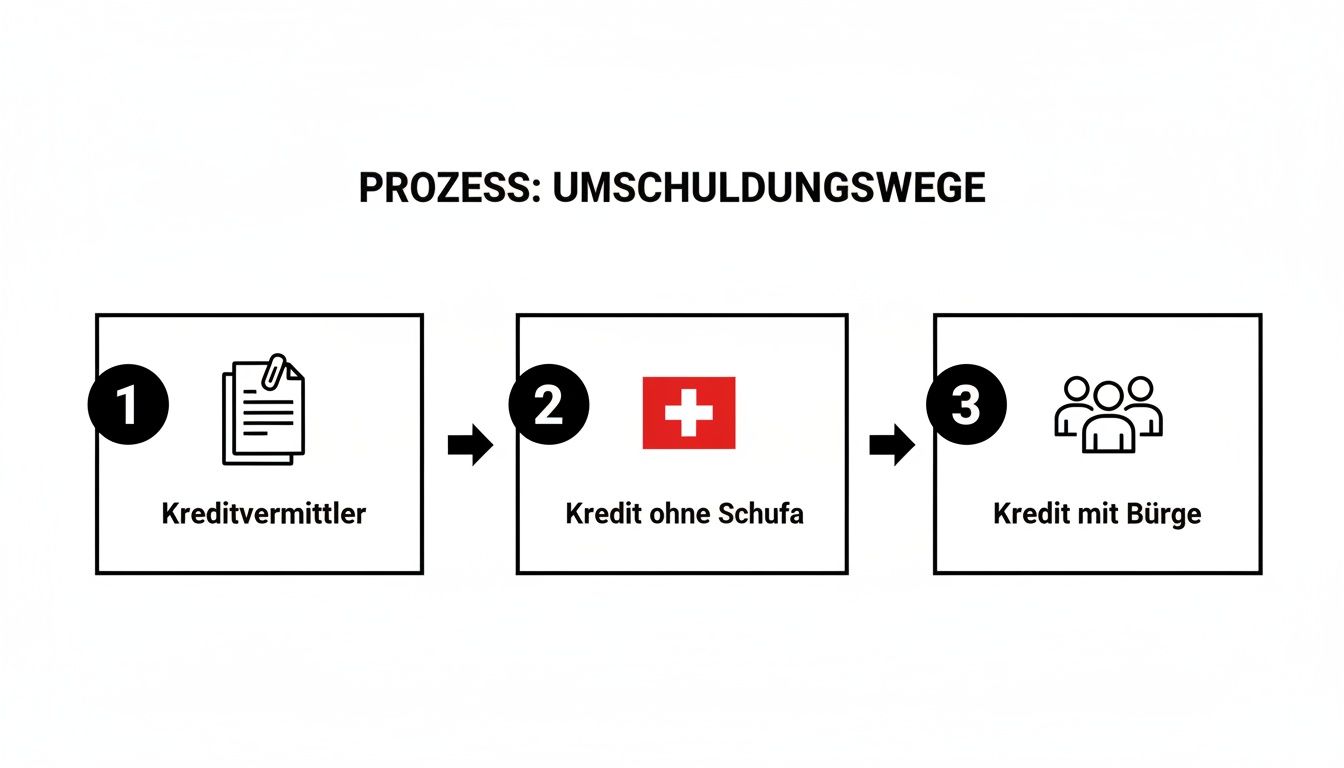

Discover specialized providers and alternative routes

When your bank says “no” because of a Schufa entry, it often feels like a dead end. But it usually isn’t. The financial market is much bigger and more creative than you might think at first glance. There are a whole range of specialists and channels out there that are made for just such cases. So instead of burying our heads in the sand, let’s take a closer look at these options.

Unfortunately, many people are familiar with this scenario: House banks are increasingly tightening the thumbscrews when it comes to lending. A Bundesbank survey on the lending business clearly shows that rejection rates for personal loans are rising – even though demand is actually high. This is precisely what drives many people looking for a loan directly to the experts for debt restructuring loans despite Schufa. The complete results can be found in the Bundesbank’s press release.

Credit brokers as a bridge to new opportunities

A really pragmatic first step can be to go to a reputable credit broker. These are not banks, but rather matchmakers – they bring you together with a broad network of financing partners. The huge advantage for you is that these professionals know the market like the back of their hand and know exactly which banks are still willing to talk to you, even if your credit rating has been affected.

A good broker will take a close look at your financial situation and then forward your request to the institutions with the best chances. This not only saves a lot of time, but also prevents you from starting a chain of loan applications that would only drag your credit score down even further.

My practical tip: You can recognize reputable loan brokers by the fact that they never charge upfront costs. Their commission is only due when the loan agreement is successfully concluded and is then already included in the APR. Hands off anyone who wants to see money in advance!

Loans without Schufa: the solution from abroad?

Another option that is often discussed is the so-called “loans without Schufa”. As the name suggests, no credit check is carried out at all. Such loans almost always come from banks in neighboring countries, typically Switzerland or Liechtenstein.

However, this route has very clear rules:

- Income is everything: Because the Schufa is no longer a safeguard, these banks look extremely closely at your income. A regular and sufficiently high salary from a permanent job is an absolute must.

- Interest with a risk premium: The providers naturally pay for the higher risk. The interest rates for a no-obligation loan are usually significantly higher than those of a normal installment loan.

- No huge sums: In most cases, the loan amounts are limited to manageable sums such as €3,500, €5,000 or a maximum of €7,500.

This option is therefore particularly suitable if you want to pay off smaller, expensive old debts and have a really stable employment relationship. Sometimes this is also a good addition if you need to get money quickly, as is the case with an instant loan, which can be applied for quickly and cheaply online.

Bringing alternative collateral into play: Guarantee and pledge

But what if neither the intermediary nor the loan without Schufa works? Then there are still models that are not based on your creditworthiness, but on other collateral.

A real classic, which is unfortunately often forgotten, is the loan with a guarantor. Here, a second person with an impeccable credit rating – usually from your family or circle of friends – steps into the breach for you and is liable for the loan if you can no longer pay the installments.

Another option is the pledge loan. Here you deposit an item of value, for example your car or an endowment life insurance policy. The amount of the loan is then based on the value of this pledge. This is a very quick way to become liquid, but of course involves the risk of losing the item if you fall into arrears.

From paperwork to payment: this is how the application process works

Have you sorted out your finances and have a clear plan in mind? Perfect, now it’s time for the actual application. This may sound like a hurdle at first, but with the right preparation, it can become an absolutely doable process. Let’s go through together how to get from the paperwork to the money in your account with ease.

Incidentally, the market for debt restructuring is quite interesting at the moment. A report by CBRE shows that banks currently prefer to extend or reschedule existing loans rather than grant completely new ones. This means that although rejection rates for new loans are rising, well-prepared applicants for debt restructuring often have better cards. If you want to understand the background in more detail, you will find fascinating insights in the analysis of lending at Immobilienmanager.

Having the right documents to hand

In all honesty, clean and complete documentation is half the battle. This builds trust with potential lenders and immediately signals: “I have my finances under control and am a reliable partner.”

It is best to prepare everything in advance, either digitally as a scan or in a folder as a copy.

You will usually need the following:

- Proof of your income: These are the last three payslips. If you are self-employed, have your last tax assessment ready.

- Bank statements: The bank needs a complete overview of the last three months in order to track your income and expenditure.

- Old loan agreements: Grab the contracts of the loans you want to pay off. This will show you the exact remaining debt and the previous conditions.

- Your budget statement: The detailed list of all your monthly income and expenditure, which you have already created anyway.

Think of these documents as your financial business card. The tidier and more complete everything is, the quicker and smoother the audit will go.

The digital application – explained step by step

Nowadays, thanks to online platforms, the application process is fortunately no longer rocket science. In most cases, you are simply guided through a form on the website where you enter your personal details and financial information. A loan calculator is often also offered at this point.

My tip: Use this calculator extensively! Play through various scenarios. What happens to the monthly installment if you change the term? What effect does a slightly different loan amount have? This will help you find the combination that really fits your budget perfectly.

A very important professional tip: Make sure that you make a “condition inquiry” and not a fixed “credit inquiry” with every inquiry. A condition inquiry is Schufa-neutral, whereas several fixed credit inquiries in succession can actually worsen your score.

As soon as you have found the right conditions, simply upload your prepared documents. The provider will then check everything and hopefully give you the green light quickly. You can also improve your chances with the right tips for a successful loan application.

The following chart summarizes the most common ways to restructure your debt, especially if the direct route to your bank may not work.

Even if each of these channels has its own special features, the basic procedure with documents and application always remains very similar at its core.

Evaluate offers correctly and avoid typical pitfalls

The first offer that arrives for debt restructuring is rarely the best. The only problem is that if you have a negative Schufa entry, you tend to jump at the chance for fear of another rejection. However, this is a costly mistake that you should avoid at all costs.

Take the time to scrutinize each offer like a professional. Of course, the first thing you look at is the nominal interest rate, but this figure only tells half the story. Much, much more important is the APR. It is the only honest figure, because it really does include all the costs and fees associated with the loan.

The devil is in the small print

Even the APR can still hide a few stumbling blocks. It really is crucial to understand the small print before your signature lands on the paper. Pay close attention to these points – they often make the difference between a good deal and a really bad one:

- Special repayments: Are you allowed to put extra money towards repayments from time to time to get out of debt faster? And if so, is this free of charge or do you have to pay a fee?

- Installment breaks: What happens when things get really tight financially? Does the contract give you breathing space by allowing you to skip one or more installments?

- Residual debt insurance: Are you offered such insurance or is it even made a condition? Be careful! These policies often make a loan considerably more expensive and are only really useful in the rarest of cases.

These small details ultimately determine how flexible you are and how much your debt rescheduling loan despite Schufa really costs you. An interest rate that seems favorable at first glance can quickly become a burden due to rigid contractual conditions.

A reputable provider will never put you under pressure to sign immediately. Nor will they demand upfront costs. Always take enough time to think things over and don’t let anyone talk you into expensive additional products.

To make the differences tangible, let’s take a look at two fictitious offers. This quickly makes it clear what really matters in a real loan comparison, which is easy to do to find the best deal.

Compare loan offers in detail: What really matters

Let’s imagine you have two commitments in your hands for a debt rescheduling loan of €15,000. A direct comparison shows which key figures are decisive for the total costs in addition to the interest rate.

| Feature | Offer A (credit intermediary) | Offer B (direct bank) |

|---|---|---|

| Credit | 15.000 € | 15.000 € |

| Runtime | 84 months | 84 months |

| Nominal interest rate | 7.8 % p.a. | 7.5 % p.a. |

| Processing fee | 250 € | 0 € |

| Effective annual interest rate | 8.2 % p.a. | 7.8 % p.a. |

| Monthly installment | 231 € | 228 € |

| Total costs | 19.404 € | 19.152 € |

| Special repayment | Possible free of charge | 1 % fee (prepayment penalty) |

At first glance, offer B looks more tempting with its lower nominal interest rate. The APR confirms this impression: you would save €252 over the entire term.

But here’s the but: if flexibility is important to you because you might be expecting a bonus payment or a small inheritance, offer A could be the better choice despite the higher costs. The option to make a special repayment free of charge is worth cash. Careful consideration of your personal situation is the key to success here.

Done! And what comes after the debt restructuring?

Congratulations, you’ve made it! The debt restructuring is done, the expensive ballast of old loans is gone and the monthly installment is finally affordable again. That feels good, doesn’t it? But don’t see it as the finishing line, but as the starting signal for a new, financially healthier life. Now the real work begins – and it’s even fun.

Thanks to the new, lower interest rates and the combined installment, you have money left over every month. That’s your joker. Many people make the mistake of simply letting this extra money get lost in everyday life. But this money is far too valuable for that. Think of it as your own personal starting capital for a stable future.

Make the money you have freed up work for you

Instead of planning the savings for the next online purchase, give the money a fixed task. It’s best to focus on two things: building a safety net and getting rid of debt even faster. It’s about moving from reacting to bills to actively managing your finances.

Two simple but extremely effective strategies have proven themselves in my experience:

- The nest egg – your financial airbag: set up a standing order to a separate call money account immediately. Start small, perhaps with €50 a month. The important thing is that it happens automatically. Your aim should be to gradually save up a cushion of three full net monthly salaries. This buffer is worth its weight in gold if the washing machine suddenly goes on strike – then you no longer have to resort to an expensive overdraft facility.

- Special repayments – the turbo for your freedom from debt: Take a direct look at your new loan agreement: are free special repayments possible? If so, take advantage of it! Even small extra payments, such as €500 from your Christmas bonus once a year, make a huge difference. They noticeably shorten the term and save you a lot of interest in the end.

With this dual strategy, you not only create security for unexpected events, but also see the light at the end of the debt tunnel much more quickly.

Debt restructuring gives you room to breathe. However, whether this will lead to long-term stable financial health depends solely on what you do with this newfound breathing space.

Breaking the vicious circle once and for all

The biggest trap after a successful debt restructuring? Falling back into old habits. The new, single installment feels so manageable that you quickly become careless. This is exactly why a simple but consistent budget is now more important than ever.

Keep an eye on your expenses. It doesn’t matter whether you use a simple app or a classic notebook. The main thing is that you know where your money is going. Set yourself clear limits for variable items such as going out, clothes or delivery services. This is the best way to prevent small liabilities from accumulating unnoticed and becoming the next big problem at some point.

A debt rescheduling loan despite Schufa was an important second chance for you. Now it’s up to you to really seize this opportunity. It’s no longer just about somehow managing debt. It’s about seeing financial freedom as a goal that you can actually achieve – and actively working towards it from today.

Your most pressing questions about debt rescheduling with a schufa entry

Do you still have a few question marks buzzing around in your head? That’s perfectly understandable, because debt restructuring is not an everyday step. To give you more certainty, I have compiled the answers to the most frequently asked questions that I come across time and again in practice when it comes to debt restructuring loans despite Schufa.

How long will a negative Schufa entry haunt me?

The good news first: a negative entry does not remain forever. Most entries, for example settled debts or paid-off loans, are deleted after a period of exactly three years. It is important to know that this period begins on the day after the debt has been paid in full.

A little practical tip: Check your credit report regularly. Sometimes outdated or even incorrect data creeps in. You can have these actively deleted and thus improve your score.

Will an application for a debt rescheduling loan worsen my score?

We have to take a very close look here, because it depends on the type of request. A pure “request for loan conditions” is completely invisible to your Schufa. You can therefore look around several banks and brokers to find the best offer without your score losing a single point.

But be careful: Only the binding “credit application” is noted at Schufa. If you submit several of these in a short space of time, banks could interpret this to mean that you have already been rejected several times. Of course, that doesn’t look good.

Can I also redeem my expensive overdraft facility with negative credit rating?

Yes, absolutely! In fact, it’s one of the smartest financial decisions you can make. With interest rates of often over 12%, overdraft facilities are one of the most expensive debt traps of all. If you replace it with a much cheaper installment loan, you will immediately feel the difference in your wallet because the interest burden drops rapidly.

Specialized brokers and banks that offer debt restructuring despite Schufa problems know this scenario only too well and often have suitable solutions ready to finally end this permanent financial burden.

What if I get a rejection everywhere?

A rejection is bitter, no question. But don’t see it as the final end, but as a wake-up call. It’s the time to pause and rethink your strategy. Here are a few options that are now open to you:

- Get professional help: Professional debt advice, for example from Caritas or Diakonie, is free of charge and completely confidential. The experts there will take a close look at your situation and work out a feasible plan with you.

- The hard but honest way: sometimes the best solution is not to take out a new loan. Draw up a tough budget plan, cut out everything that is not essential for survival and pay off your debts bit by bit under your own steam.

- Talking helps: Try to talk directly to the people you owe money to. If you explain your situation honestly, many creditors will be willing to accommodate you with an installment break or smaller monthly payments.

Are you ready to reorganize your finances and say goodbye to expensive old loans? At Finanz-Fox you can compare transparent loan offers and receive personal support to find the way that really suits your situation. Start your no-obligation comparison now at finanz-fox.de