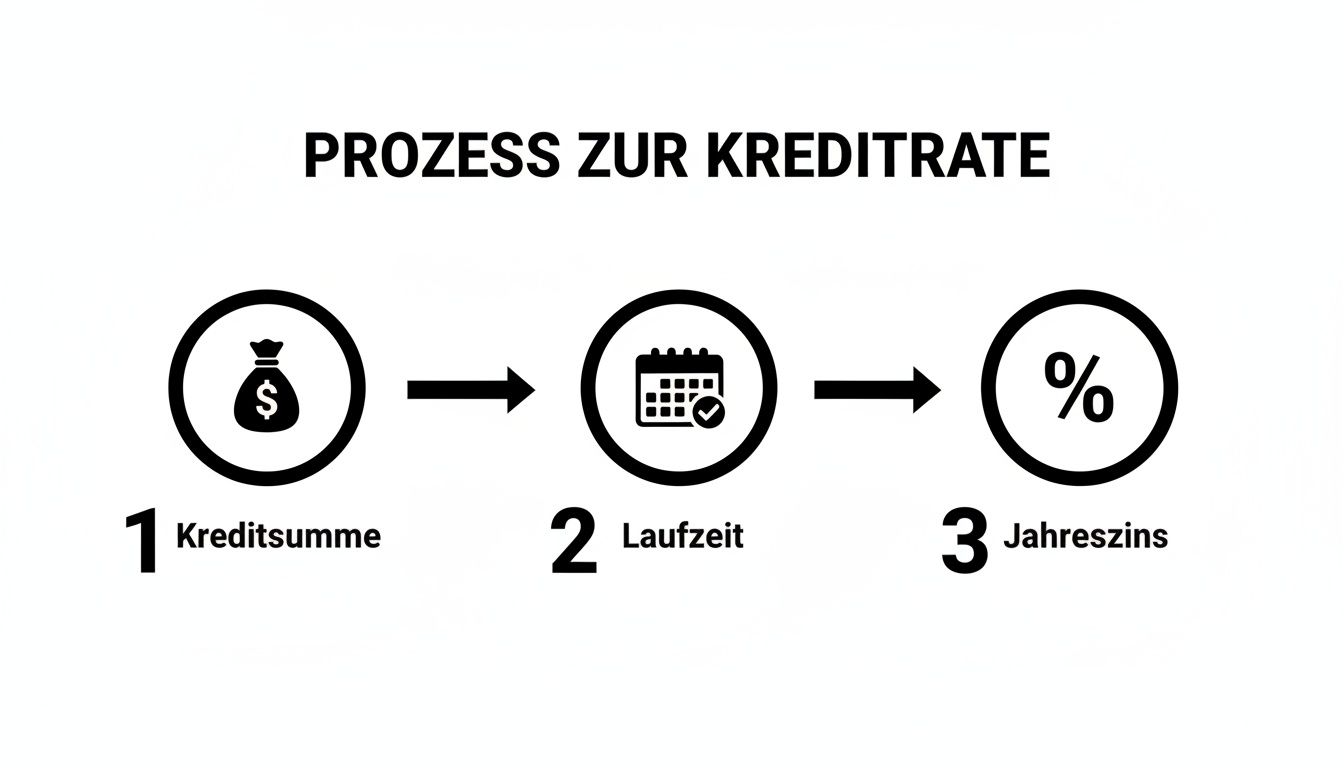

Fortunately, calculating the monthly loan installment is not rocket science. Basically, it all depends on just three factors: the loan amount, the term and the APR. If you understand these three factors, you have already taken the most important step towards making a sound financial decision.

What your monthly rate really amounts to

Before even signing a loan agreement, one thing must be crystal clear: How high is the monthly charge? This rate does not fall from the sky, but is the result of the interplay of three fundamental building blocks. Each of them has a direct influence on what you pay at the end of the month – and how expensive the loan will be overall.

If you have an overview here, you can really compare offers, whether from SWK Bank or Giromatch, and make a smart decision for your own financial situation.

The three pillars of credit calculation

Ultimately, it is always these three components that determine your financial commitment:

- Loan amount (net loan amount): Quite simply, this is the amount you borrow from the bank. The more money you borrow, the higher the installment will logically be if the other conditions remain the same.

- Term: This is the period over which you repay the loan, usually expressed in months. A longer term makes the monthly installment look smaller, but be careful: you will also pay more interest over the years, which makes the loan more expensive overall.

- Effective annual interest rate: This percentage is crucial. It shows the actual annual cost of the loan and often includes more than just the borrowing rate. A low effective interest rate should always be your primary goal.

Many people make the mistake of only looking for the lowest possible monthly installment. However, this is often bought with an extremely long term, which in the end drives up the loan unnecessarily.

With this knowledge, you are well prepared. However, it is also important to understand how external factors influence your conditions. Find out, for example, how SCHUFA influences the granting of loans in Germany, as a good score can secure you significantly better interest rates.

The German credit market is huge, which makes a precise comparison all the more important. The volume of consumer loans to private households in Germany climbed to an impressive 197.3 billion euros by the end of December 2024. This impressive figure shows why comparison portals such as Kredit-Fuchs.de are so important for finding the right conditions in the jungle of offers. Anyone interested in the figures can find further insights in Statista’s data on credit volume.

The annuity formula in practice – how to calculate correctly

Sure, an online calculator is quick and convenient. But if you really want to understand what makes your loan tick and where the cost traps lurk, it’s worth taking a look behind the scenes. Calculating your loan rate manually may seem daunting at first, but it’s the best way to not only compare offers, but to really see through them.

Let’s tackle it together and break down the infamous annuity formula into its individual parts.

The formula explained clearly

Even if the formula looks like advanced mathematics at first glance, it is based on three simple building blocks that we already know: Loan amount, interest rate and term. Your task is to calculate a monthly installment (the annuity) that remains the same over the entire term.

The trick here is how this installment is made up. The ratio shifts with each payment: at the beginning, a large proportion goes towards interest, while later on more and more money goes directly towards paying off your debts.

Ultimately, it’s always these three levers that are used to determine your monthly charge.

The graphic makes it clear: the loan amount, term and annual interest rate are the key factors that shape your rate. If one of these values changes, your monthly payment will also change.

A concrete example from everyday life

Imagine you have found your dream car and need a loan of €15,000 for it. Your bank makes you an offer: a 60-month term (i.e. 5 years) with an effective annual interest rate of 4.5%.

To determine the monthly installment, we first need the monthly interest rate. That’s done quickly:

- Monthly interest rate: 4.5% divided by 12 months = 0.375% (or 0.00375 as a decimal)

If we enter this value together with the loan amount and the term into the annuity formula, it spits out a monthly installment of €279.64 for our example.

This is the crucial point: at the beginning, a large part of this €279.64 only covers the interest. Only over time, when the residual debt decreases, does the repayment portion increase noticeably and you pay off the loan faster and faster.

The repayment plan brings clarity

It is precisely this shift between interest and repayment that a repayment plan makes visible. For each individual installment, it lists how much money goes to the bank (interest) and how much actually reduces your debt (repayment).

Here you can see what this looks like for our example in the first few months:

Exemplary repayment plan for a €15,000 loan

This table shows the development of the interest and repayment portion as well as the residual debt for the first few months of a loan of € 15,000 at 4.5% interest and a term of 60 months.

| Month | Monthly installment | Interest portion | Repayment portion | Residual debt |

|---|---|---|---|---|

| 1 | 279,64 € | 56,25 € | 223,39 € | 14.776,61 € |

| 2 | 279,64 € | 55,41 € | 224,23 € | 14.552,38 € |

| 3 | 279,64 € | 54,57 € | 225,07 € | 14.327,31 € |

| 4 | 279,64 € | 53,73 € | 225,91 € | 14.101,40 € |

You can immediately see the principle: while the installment remains stubbornly at € 279.64, the interest portion decreases with each month and the repayment portion increases in return. In this way, the residual debt becomes smaller and smaller until it reaches zero at the end of the term.

This knowledge is worth its weight in gold when you are evaluating offers from different banks. And if you’re wondering how much credit you can actually afford: In our guide, we show you how to calculate your personal credit limit.

Why the APR really matters

When comparing loans, two terms often spring to mind: the borrowing rate and the effective interest rate. Banks like to advertise the lower borrowing rate, but only one figure is really decisive for you: the APR. It is the honest, unvarnished price for your borrowed money.

Why is that? Quite simply, the borrowing rate only covers the pure interest costs for the loan. The APR, on the other hand, includes almost all additional costs and shows you what the loan will really cost in the end.

What’s in the effective interest rate

Think of the effective interest rate as an “all-inclusive price” for your loan. The law stipulates that banks must include most of the ancillary costs incurred here.

These include, for example:

- Processing fees: Are charged less frequently today, but they still exist.

- Account management fees: Sometimes costs are incurred for the obligatory credit account.

- Intermediary commissions: If a credit broker is involved.

It is precisely these additional costs that turn a supposedly cheap offer into a realistic and, above all, comparable figure. So if you want to keep your monthly loan installment as low as possible, you should always look at the effective interest rate first.

A realistic comparison shows the truth

Let’s take a look at two typical offers for a €10,000 loan to illustrate the difference:

- Bank A: Lures you in with a low borrowing rate of 3.9%, but charges a processing fee of €200.

- Bank B: At first glance, offers a higher effective interest rate of 4.2%, but without any additional fees.

In this case, the APR of bank A would be significantly higher than that of bank B after taking the fee into account. What initially looked like a saving turns out to be a cost trap. This is why it is so important to always use the effective interest rate as the central criterion for comparison on portals such as Kredit-Fuchs.de.

A loan offer with a borrowing rate of 3.5 % and hidden fees can end up costing you more than an offer with a 3.8 % effective interest rate where everything is included. So never compare apples with pears – the effective interest rate is the common denominator.

If you want to delve deeper into the matter, our guide to loan interest rates in Germany explains the differences and their effects in detail.

Smart strategies to lower your credit rate

A lower monthly payment immediately gives you more financial leeway. But what’s the best way to get there without getting lost in complicated negotiations? Fortunately, there are a few really effective levers that you can use to actively reduce your monthly payment. If you know these tricks, you can not only calculate your rate, but also optimize it in a targeted manner.

The most obvious method is to extend the term. If you stretch the repayment over more months, the individual installment will naturally fall. But be careful: this is a classic compromise. The longer fixed interest period means you end up paying more interest overall. In other words, you trade a lower monthly payment for higher overall costs.

Brush up your credit rating and request together

A squeaky clean credit rating is your ticket to the best interest rates on the market. Before you even submit an application, take a look at your SCHUFA data. Look for errors and pay small, outstanding bills. Sometimes just a few months of absolutely punctual payments can noticeably improve your score and open the door to significantly more favorable conditions.

Another lever that is often underestimated is a second borrower. If you apply together with a partner who also has a stable income, banks see a much lower risk. The result? Often dramatically better interest rates, which translates directly into a lower monthly installment.

Practical experience: Many banks see a joint application not only as double security. They also see it as a sign of a stable, predictable life situation. This can be the decisive factor in obtaining top conditions that a single applicant might never have obtained.

Clever restructuring of existing loans

Are you still lugging around one or more expensive old loans? Then debt restructuring could work wonders. The idea is simple: you take out a new, cheaper loan to pay off the old, expensive debts in one go.

The advantages are obvious:

- Lower interest rate: You secure the often much more favorable current interest rate level.

- Only one installment: Instead of transferring several installments to different creditors, you only have one single payment. This gives you an enormous overview.

- Less strain: The lower rate immediately provides more breathing space in your monthly budget.

It is also interesting to note that even your place of residence can have an influence on the loan amount. There are sometimes considerable differences in Germany: In Bavaria, the average installment is a whopping 1,267.14 euros, while in Thuringia it is only 870.25 euros. This is often due to the higher cost of living and property prices, which make larger loans necessary.

In addition to optimizing loans, it is also worth keeping an eye on other financial products. For example, find out how you can cleverly manage and save on credit card costs.

In the end, a thorough loan comparison in Germany is the best way to realize the full potential of these strategies and find the financing that really suits you.

How to find your loan with the Kredit-Fuchs.de calculator

Enough of the gray theory about formulas and interest types – let’s get down to practice. By far the quickest and easiest way to find out your personal loan rate is to use a good online tool. Instead of pulling out a calculator, we use a tool that not only spits out a sample rate, but also provides you with a real market overview in seconds: the loan calculator from Kredit-Fuchs.de.

The whole process is pleasantly uncomplicated. You don’t have to be a financial professional to get a meaningful result. The aim is clear: to give you a reliable basis for your financial planning, based on real, up-to-date conditions.

The right rate in just a few steps

The calculator’s input screen is deliberately kept lean and only asks for the three key pieces of information we have already discussed. With this information, the system can simulate a request for conditions from a large number of banks in the background – without any obligation on your part.

Here you can see where to enter your desired data:

As you can see, the loan amount, term and intended use are all you need to start the comparison. Incidentally, the intended use is a real insider tip. Banks often offer significantly better interest rates for specific projects such as a car or modernization than for a loan for free disposal.

The decisive advantage over a pure formula calculation? You don’t just get a theoretical value. Instead, you will see a selection of customized offers from various banks. The calculator provides you with realistic conditions based on your data and does not tempt you with unrealistic window-dressing interest rates.

The biggest difference to a pure formula calculation is that a good online calculator takes your personal creditworthiness into account in the next step. It therefore not only provides you with a mathematically correct rate, but one that is really relevant to you personally.

If you are ready to see concrete and comparable offers, you can get started right away. The Kredit-Fuchs.de loan calculator is the fastest way to make an informed financial decision.

One last thought: turn your knowledge into money

You’ve done it. The formulas are deciphered, the difference between borrowing rate and effective interest rate is clear, and you know how to actively reduce your monthly burden. This is more than just dry theory – it is the basis for making smart financial decisions and ultimately for your financial independence.

The decisive moment has now arrived: implementation. Put your new knowledge to use. Question offers, compare them critically and don’t let yourself be dazzled by the first tempting offer. A careful, transparent loan comparison is not a luxury, but a must.

An optimized loan is not just a relief for your budget. Every euro you save on your installment is capital that can work for you – be it in shares, ETFs or other investments. If you want to invest in real estate, for example, you need to be able to calculate the cash flow from real estate. And the amount of your loan installment plays a central role in this.

Are you ready to find the financing that really suits you? Compare offers now, free of charge and without obligation, and secure the best rate for your project.

Calculate your individual loan installment now at Kredit-Fuchs.de

Frequently asked questions (FAQ)

What is the difference between borrowing rate and effective interest rate?

The borrowing rate (also known as the nominal interest rate) is the pure interest rate that the bank charges for lending the money. The APR, on the other hand, is the “all-inclusive price”: in addition to the borrowing rate, it also includes most additional costs such as processing fees or account management fees. The effective interest rate is therefore always decisive for a real comparison of loan offers.

How does the term affect my monthly installment?

The term is one of the biggest levers. A longer term leads to a lower monthly installment, which reduces the monthly burden. But be careful: because you pay interest for longer, the total cost of the loan increases significantly. A shorter term means higher monthly installments, but you will be out of debt faster and save on overall interest costs.

Can I change my monthly installment at a later date?

Once an installment has been agreed, it is usually fixed for the entire term. A reduction is usually only possible through debt restructuring, where you replace the old loan with a new, cheaper one. However, many modern loan agreements allow for free unscheduled repayments. This allows you to shorten the term and save on interest costs, even if the installment itself remains the same.

Is a condition request via an online calculator bad for my SCHUFA?

No, absolutely not. A request via a comparison calculator such as the one from Kredit-Fuchs.de is purely a request for conditions. This is SCHUFA-neutral, so it is not stored as a hard credit application feature and has no negative impact on your score. You can therefore run through various scenarios without hesitation.