Your wallet is empty, an unexpected bill has arrived and, to make matters worse, you have a negative Schufa entry in the back of your mind – a dilemma that sends many people looking for a “mini loan without Schufa”. The idea of getting money quickly and easily naturally sounds extremely tempting in such a situation. But I have to be honest here: a truly credit-free loan from a reputable provider is simply not legally feasible in Germany. And that’s a good thing in the end, because this regulation primarily protects you.

The myth of quick money without a Schufa check

Anyone looking for a mini loan without Schufa is usually in an acute emergency. The washing machine breaks down, the car goes on strike – and the fear of not having a chance with any bank because of an old entry is huge. This fear is precisely the business model of many dubious online providers. They advertise with promises that sound too good to be true and lure people seeking help straight into expensive cost traps.

However, the reality is quite different: Every reputable lender in Germany is legally obliged to check the creditworthiness (credit rating) of applicants. This is not harassment, but an indispensable protective mechanism designed to prevent you from overextending yourself financially and slipping into excessive debt. The good news is that a negative entry does not automatically mean the end of all credit opportunities.

Why the search is so widespread

The demand for loans in Germany remains high, which naturally fuels the hunt for quick solutions. According to Statista data, the number of loans taken out has more than doubled since 2006, not least thanks to digital platforms that enable quick comparisons. The targeted search for a “mini loan without Schufa” has a tangible reason: after all, around 6 million Germans are affected by negative entries at Schufa Holding AG. That’s around 7-8% of the population living with negative features in their credit file.

This guide looks behind the façade of these bait-and-switch offers for you. We don’t want to give you false hope, but show you a real, viable way forward:

- We expose the typical scams and cost traps of the black sheep.

- We explain why a fair credit check is also an advantage for you.

- We present you with tried-and-tested and really fair alternatives.

- We give you clear instructions on how to overcome financial hurdles safely.

Come along and find out how you can really achieve your financial goals instead of falling into a debt trap. An honest and fair approach to your financial situation is always the best first step. You can also read our other articles to help you better understand the topic of Schufa.

Why a credit check is mandatory in Germany

The idea of submitting a loan application that is simply waved through – without any tedious checks – sounds tempting, doesn’t it? In the real world, however, such a promise is a huge red flag. Because in Germany it is simply forbidden. A credit check is not a harassment of the banks, but a protective mechanism enshrined in law.

Think of it like building a bridge. You want to get safely to the other side, i.e. overcome your financial bottleneck. The lender, in turn, needs to be sure that the bridge – i.e. the loan – is stable enough to carry you without collapsing in the middle. The credit check is the static calculation that ensures that the bridge is safe for both sides.

The German Banking Act (KWG) is crystal clear here: every reputable lender must check the creditworthiness of an applicant. There is a very simple aim behind this: to prevent you from becoming over-indebted. A loan that you can’t pay back in the end is no help. It will only drag you deeper into debt. This check therefore not only protects the bank from a loss, but first and foremost protects you from a burden that could crush you.

The role of Schufa and Co

When you hear “credit check”, you almost automatically think of Schufa. Although Schufa Holding AG is the best-known name, it is by no means the only player on the field. There are also other credit agencies such as Creditreform Boniversum, CRIF or Arvato Infoscore, which also collect data on the payment behavior of all of us.

You can think of these companies as having a financial memory. They store information that their partners – banks, mobile phone providers or online stores – report to them.

- Positive entries: These are, for example, loans that have been repaid on time, a current account that has been well managed for years or a cell phone contract where everything has always run smoothly.

- Negative entries: These are unpaid bills despite reminders, defaulted loans, personal insolvency or even an arrest warrant for debt.

A score is then calculated from all these pieces of the puzzle. This value is a forecast of how likely it is that you will meet your payments. A score above 97.5% is considered top and indicates an extremely low risk. However, if the score is below 90 %, it can be difficult to get a loan. The exact formula behind the calculation is a trade secret, but one thing is certain: a responsible approach to your own finances always pays off in the end. If you want to delve deeper into the subject, you can find more details in our articles on credit checks.

What reputable providers really check

Many people mistakenly believe that a negative Schufa entry means the immediate end of any loan application. This is not true. Reputable banks and lenders look at your overall financial situation and do not blindly stare at a single number. The Schufa report is only part of the overall picture.

A single negative entry from the past does not have to determine your present financial situation. The decisive factor is the overall stability of your current situation.

Modern credit decisions are more complex. The following points often weigh much more heavily than an old misstep:

- A regular income: A steady, permanent job is and remains the best proof that you are able to make the installments.

- The budget calculation: the bank does the hard math: What is left of your income after rent, insurance and other fixed costs are paid? Is that enough for the loan installment?

- Existing debts: Are other loans or installment payments already running? How high is the total burden?

- The type of Schufa entry: There is a huge difference between a forgotten cell phone bill from three years ago and an ongoing personal insolvency.

A provider who gives you a loan despite a Schufa entry does not do so “without checking”. They carry out a fair and differentiated check. They understand that people make mistakes but can still be financially reliable.

The cost trap with dubious credit promises

When money is tight, an advertisement for a “guaranteed loan without Schufa” seems like a lifeline in stormy seas. But beware: behind these tempting promises often lurks a minefield of hidden fees and absurd demands. Unscrupulous providers deliberately exploit people’s desperation to force them into contracts that end up creating more problems than they solve.

Imagine the situation: You urgently need 500 euros. A provider promises you exactly this amount, supposedly without even looking at your credit file. What sounds like the perfect solution at first unfortunately all too often turns out to be an expensive nightmare. The tricks are varied and usually cleverly hidden in the small print, so that you only realize the true cost explosion when it is already too late.

These people know full well that their target group often feels they have no other choice. They are building a system that is not designed to help, but to make maximum profit from the plight of others.

How a cost trap is structured

Let’s take a look at a typical scenario to understand how quickly the costs can get out of hand. You apply online for a “credit-free” mini loan for 500 euros. But instead of a simple approval, a costly process begins that quickly eclipses the original amount required.

The methods are sophisticated and aim to take money out of your pocket at various stages of the process. Each step is designed so that you have already invested money before you even realize that you will never receive the promised loan.

A dubious loan offer is like a labyrinth with no exit. Every step you take leads you deeper into the costs, but never to the promised destination – the money.

The following items could suddenly end up on your bill:

- Upfront costs for documents: You are suddenly told that a fee of 80 euros is due for “checking and preparing your personal loan documents”. Of course, you have to pay this in advance to get the process started.

- Insurance imposed on you: In order to “secure” the loan, you are talked into taking out completely overpriced residual debt insurance. The cost of this – let’s say 120 euros – is often offset directly against the alleged loan amount.

- Intermediary fees: A “financial reorganizer” gets in touch and offers to sort out your finances. For a hefty commission of 150 euros, of course. He promises to obtain the loan, but this never happens.

- Cash on delivery charges: The contract documents will be sent cash on delivery and will cost you an extra 20 euros at the door.

At the end of the day, you haven’t received a single cent of credit. Instead, you are out 370 euros. So your original problem – the missing 500 euros – has almost doubled without you having made a single step forward.

Checklist: How to expose dubious offers

To avoid falling into such a trap, it is extremely important to know the typical warning signs. Think of this checklist as your personal protective shield. If even one of these points applies, you should keep your hands off the offer.

- Demand for upfront costs: Reputable providers never demand money before a loan agreement has been signed and the amount paid out. Fees for simply checking the application are a clear red flag.

- Guarantee promises: Statements such as “credit guaranteed for everyone” or “100% payout without verification” are sheer nonsense. Every responsible lender checks the financial situation of its customers.

- Sale of additional products: Are you being pressured to take out insurance, a building society savings contract or “financial advice” in order to get the loan? This is a classic scam to get additional commission.

- Unclear contract details: If interest, fees and the exact repayment conditions are not broken down clearly and comprehensibly, this is a bad sign. Transparency is the be-all and end-all here.

- Pressure and haste: someone is pressuring you to sign quickly? A reputable partner will always give you enough time to consider an offer at your leisure. A comprehensive instant loan comparison can help you get a feel for standard market conditions.

- Home visits and cash on delivery: Unannounced visits by brokers or the sending of documents by expensive cash on delivery are methods that have absolutely no place in serious lending.

If you keep these points in mind, you can separate the wheat from the chaff and protect yourself from financial adventures that would only make your situation worse in the end.

Safe alternatives when you need money quickly

A Schufa entry often feels like a slammed door, especially when you urgently need money. But that’s only half the truth. In reality, it’s just the moment when you learn to look for other, often even better ways. The good news is: there are a whole range of reputable and secure alternatives to the classic bank loan that are made precisely for situations like this.

The search for a “mini loan without Schufa” doesn’t have to lead you to dubious corners of the internet. Quite the opposite. There are absolutely responsible ways to bridge a financial bottleneck without falling into an expensive trap.

The trick is that these alternatives simply assess your financial situation differently – more fairly and with more focus on the here and now. Your current income often counts more here than a problem from the past.

Special providers for loans despite Schufa

The first and usually most direct route leads to financial service providers who specialize in precisely this: Small loans for people whose Schufa score is not perfect. These providers know from experience that a negative entry does not automatically mean that someone cannot pay their bills.

Their business model is clever and fair. Instead of just looking at the score, they check two things in particular:

- Your regular income: Can you prove with payslips that you have a steady job and a stable income? This is the most important basis.

- Your free budget: What is left over at the end of the month after rent, electricity and other fixed costs are paid? Is that enough for the loan installment?

The type of Schufa entry also plays a role. An entry that has long since been closed is completely different from an ongoing seizure.

These providers almost always work completely digitally. This makes the process incredibly fast. You often get a decision within minutes and the money can be in your account the same day.

P2P loans: from person to person

P2P lending platforms are a really interesting alternative. The abbreviation stands for “peer-to-peer”, i.e. from person to person. Here you don’t borrow money from a bank, but directly from private investors. The platform acts as a kind of marketplace, providing the necessary security and handling the entire process.

P2P platforms bring the people behind the numbers back into play. Here you have the chance to explain your situation and convince private lenders that your project is worth supporting. They often prefer to invest in a good story rather than a perfect score.

The biggest advantage is the flexibility. The lending criteria are often not as rigid as with a bank. A well-explained project or a comprehensible reason for the financial bottleneck can be the deciding factor here, even if the Schufa information is not flawless.

To avoid such bottlenecks in the future, good financial planning is the be-all and end-all. Looking at a realistic budget and saving tips can help you to get a better grip on your own spending.

The overdraft facility as an emergency band-aid

Sometimes it just has to be quick. For very short-term gaps in your budget, the overdraft facility on your current account can also be an option. It’s available immediately, without an application, without waiting.

But beware: an overdraft facility is almost always the most expensive way to borrow money. The interest rates are often dizzyingly high.

It is really only intended as an emergency solution for a few days. If you use your overdraft facility permanently, you will quickly slip into an expensive debt trap. See it for what it is: a financial band-aid for a minor wound, not a permanent treatment. We explain the best way to compare the various offers in our guide to comparing loans made easy.

Comparison of reputable credit alternatives

To make your decision easier, we have summarized the most important features of the alternatives discussed in an overview. This allows you to see at a glance which option might be best suited to your situation.

| Alternative | Typical loan amount | Advantages | Disadvantages |

|---|---|---|---|

| Credit despite Schufa | 100 € – 3.000 € | Very fast payout (often on the same day), straightforward online application, focus on current income | Higher interest rates than with traditional loans, often short terms |

| P2P loan | 500 € – 25.000 € | Fair opportunity even with medium creditworthiness, flexible conditions, personal project description possible | Payout can take longer, financing not always guaranteed |

| Overdraft facility | Depending on the salary received | Available immediately and without application, maximum repayment flexibility | Very high interest rates, high risk of permanent debt |

In the end, it’s all about finding a solution that really suits you and your current life situation. Each of these options has its advantages and disadvantages. Weigh up exactly what will help you the most now without burdening you financially in the future. The first step is always a no-obligation terms and conditions inquiry – that way you can find out what is possible for you without any risk.

The right small loan in just a few steps

Okay, so you’ve found a reputable alternative to the classic bank loan that suits you? Perfect, that’s half the battle. Now it’s just a matter of getting the application through safely. Don’t worry, the days of complicated forms and opaque requirements are long gone with modern providers. The way to get the money today is usually surprisingly uncomplicated and completely digital.

I’m just going to take you by the hand and guide you through it. Think of it like a recipe: if all the ingredients are ready and you know the steps, the dish will turn out well in the end. Our aim is to prepare the application in such a way that there are no annoying queries and you receive the money as quickly as possible.

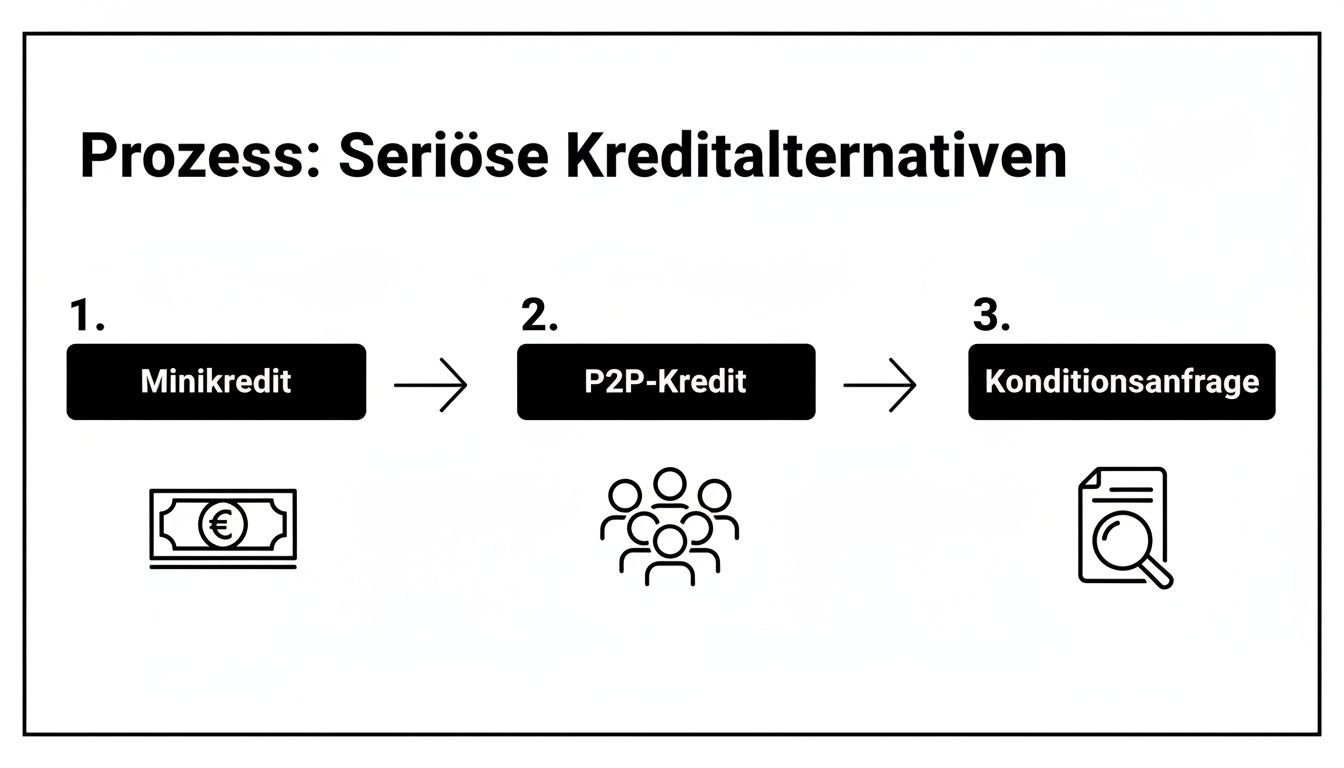

The graphic here shows quite well which serious ways there are if the house bank does not play along again.

As you can see, there are clear, structured paths from the right credit model to a non-binding review of the conditions.

Preparation is the key to success

Before you start the online application, it is best to have a few documents ready digitally. Good preparation can shorten the whole process from hours to just a few minutes. Reputable providers need to check your details in order to make a quick and fair decision. This is completely normal.

Most of the time you only need these three things:

- Have valid proof of identity ready: identity card or passport. Your identity will be checked later by video call.

- Current proof of income: The last two or three payslips are ideal. Pensioners use the current pension statement. Self-employed people usually use the business management analysis (BWA).

- Your bank details (IBAN): Logical, the provider needs to know where the money is to be transferred to.

Think of these documents as the keys to your loan. If you have all the right keys to hand, the door to fast disbursement will open without delay.

The digital application – explained step by step

As soon as everything is ready, you can get started. The application itself is really self-explanatory with most online providers and is divided into a few logical chunks.

- Enter your personal data: Start with the basics – name, address, date of birth. Just the usual.

- Explain your financial situation: This is where you provide details of your income and monthly expenses. Important: Be absolutely honest and accurate here. These figures will be compared with your supporting documents.

- Upload documents: Now upload the prepared files (payslip, ID card) securely to the provider’s portal.

- Confirm your identity (Video-Ident): This is the quickest way. You make a short video call with an employee who takes a look at your ID. The alternative is the Post-Ident procedure at a post office, but it takes longer.

- Sign digitally: Once everything has been checked, you can sign the loan agreement directly online with a qualified electronic signature (QES). That’s it.

This completely digital process is not only super convenient, but also absolutely secure. It makes a decision possible virtually in real time. You often know just a few minutes after applying whether your small loan has been approved.

If you would like to know more, you can find more tips and tricks for a successful loan application in our detailed guide.

If you internalize this procedure and prepare yourself well, you will avoid the typical pitfalls. Incorrect or incomplete information leads to time-consuming queries and can block a quick payout. By following these instructions, you have the best chance of being approved and the money will often be in your account the very next working day.

How to recognize the black sheep immediately: a checklist for your safety

People who urgently need money are often vulnerable. This is precisely what dubious providers know and they exploit this emergency situation to lure people into expensive contract traps. Their promises sound tempting, but you end up paying for it.

The good news is that these “black sheep” almost always leave telltale traces. If you know what to look out for, you can expose the rip-off artists immediately and protect yourself. See the following points as your personal protective shield.

The biggest red flag: pre-tasting in any form

The number one warning signal that cannot be overlooked is the demand for advance payments. No matter what you call it – processing fee, file fee, consultation fee – the principle is the same. A reputable provider in Germany will never ask you to pay money before a loan agreement has even been concluded.

Sounds logical, doesn’t it? A lender earns its money through the interest that is due after the loan has been paid out. If someone holds out their hand beforehand, they don’t want to solve your credit problem, they just want to get their hands on your money quickly. Often you never see any of this fee or the promised loan again.

Let’s make it very clear: any form of advance payment is a no-go. As soon as someone asks for money in advance, break off contact immediately. That is the most important rule.

Other unmistakable alarm signals

In addition to the upfront costs, there are a whole series of other signs that should make you prick up your ears. Take this list to heart to avoid falling into a trap.

-

Guaranteed promises and advertising slogans: Don’t fall for slogans such as “Credit for everyone, guaranteed!” or “100% payout without verification”. This is not only dubious, it is simply a lie. As we have already clarified, every provider in Germany must carry out a credit check – that is the law.

-

Selling unnecessary additional products: You absolutely have to take out expensive residual debt insurance, a home loan and savings contract or an ominous “financial restructuring” in order to get the loan? Watch out! This is an old trick to sell you overpriced products from which only the broker makes money.

-

Documents sent cash on delivery: If important documents are supposedly sent to you by cash on delivery and the letter carrier suddenly demands money for them at the door, this is a clear warning sign. Reputable contracts are sent digitally or by normal post, never with a hidden fee on delivery.

-

Missing imprint: A trustworthy company has nothing to hide. You will always find a full legal notice on the website with the address, commercial register number and clear contact details. Is this missing or is it just a cell phone number? Hands off!

Never allow yourself to be put under pressure. A reputable partner will give you time to consider everything at your leisure. If an offer feels just a touch strange, it usually is. Your financial security has top priority.

Your most urgent questions about credit despite Schufa

Finally, we would like to clarify the questions that we encounter most frequently in practice when it comes to the topic of mini loans despite Schufa. Here you will find clear, straightforward answers that will hopefully dispel any remaining doubts and enable you to make a confident decision.

Is there really a mini loan without a credit check?

No, and that’s a good thing. No reputable provider in Germany will give you a loan without first getting a picture of your financial situation. This is prohibited by law, because every lender must ensure that you can afford the loan. This ultimately protects you from over-indebtedness.

If you come across offers that advertise “guaranteed commitment without verification”, you should immediately become skeptical. These are almost always dubious rip-offs or providers from abroad with extremely high costs and opaque conditions. Instead, look specifically for banks that offer a fair credit check and where a fixed income is more important than an old, negative Schufa entry.

How quickly will the money be in my account if I have a Schufa entry?

Often surprisingly quickly. The specialists for small loans in particular have now optimized their processes so that everything runs digitally and at lightning speed. If you already have the necessary documents to hand, for example your last payslip, it can really be lightning fast.

Basically, it usually works like this:

- Fill in the online form: It only takes a few minutes.

- Confirm your identity via video chat: Simply with your smartphone, from the comfort of your couch.

- Sign a contract digitally: No annoying paperwork, no waiting for the post office.

As soon as all this is done, the decision is often made within minutes. If you are approved, you will often receive the money in your account on the same day or the next working day at the latest.

Gone are the days when you had to wait days for a response for a loan. Thanks to digital processes, the money is often there before the letter of approval even arrives – even if your credit rating is not perfect.

Can a mini loan repaid on time improve my Schufa score?

Yes, absolutely! This is a positive side effect that many people don’t even realize. Every installment that you pay back on time and as agreed is a strong signal that you are financially reliable.

If the lender reports this small loan to Schufa, the successful repayment can actually improve your score over time. This is a practical way of showing that you can be trusted. But be careful: too many credit applications or several loans in parallel can have the opposite effect and be rated as negative.

Are you looking for financing that is fair and suits your current situation? At Finanz-Fox, we compare reputable offers for you and assist you personally to find the right loan – quickly, digitally and without detours. Start your no-obligation comparison now at finanz-fox.de.