A targeted loan comparison for the self-employed is not a luxury, but a pure necessity. Entrepreneurs who rely on standard offers quickly fall into a trap because they ignore the reality of fluctuating incomes. The result? Unnecessarily expensive conditions or outright rejection. The real key to success lies in finding providers who really understand the world of freelancers and entrepreneurs and offer suitable, flexible solutions.

Why a standard loan is often the wrong choice

For the self-employed, freelancers and founders, the search for a loan often feels like running the gauntlet. Unlike employees with their fixed monthly salary, many banks classify an irregular income as a high risk across the board. And so it happens again and again: a loan application that goes through without a hitch for an employee ends in a dead end for the entrepreneur.

The real challenge is that a superficial comparison of interest rates is far from sufficient. After all, a loan is much more than just a number – it’s a strategic tool that can make the difference between the growth or stagnation of your business.

The classic scenario of a freelancer

Imagine an IT consultant who has been successfully self-employed for three years. Suddenly a lucrative major contract beckons, but he has to pre-invest in new server hardware and software licenses for €25,000. His business model is absolutely solid, but his income is project-based and therefore naturally fluctuates.

So he goes to his bank. Although his annual profit is more than convincing, the bank rejects his application. The reason: the irregular incoming payments in recent months. This is one of the most typical hurdles – banks often rate short-term stability higher than long-term potential. A strategic loan comparison for the self-employed would have immediately shown him providers that specialize in precisely such business models.

A loan that really fits breathes with your business. It not only gives you capital, but also the flexibility to react to the market without immediately risking your liquidity.

More than just the interest rate counts

A smart comparison reveals the subtle but decisive differences between the offers – precisely the points that make the difference for you as a self-employed person.

| Criterion | Standard offer (mostly unsuitable) | Specialized offer (the better choice) |

|---|---|---|

| Flexibility | Fixed, unchangeable monthly installments | Possibility to suspend installments |

| Repayment | Special repayments often expensive or impossible | Free unscheduled repayments are usually included |

| Rating | Focused on the last 3-6 months | Takes into account the last 2-3 years (BWA) |

| Process | Often lengthy and paper-heavy | Mostly digital and significantly faster |

For the self-employed, it is also crucial to keep an eye on the big picture. This includes knowing how to cleverly optimize business expenses – for example, by learning how to deduct office furniture for tax purposes to reduce the overall financial burden. This guide will take you by the hand so that you can find the best conditions and master the entire process with confidence.

What really matters when comparing loans for the self-employed

The first thing that self-employed people often look at when comparing loans is the APR. Understandable, but unfortunately too short-sighted. If you are only guided by this one figure, you overlook the pitfalls that can make the difference between financial breathing space and an oppressive burden in everyday business life. What makes a good loan is usually found in the small print.

Let’s take a look at the decisive criteria from a practical perspective. It’s about finding financing that not only provides money, but also adapts to your entrepreneurial rhythm – with all its ups and downs.

More than just the effective annual interest rate

Of course, the APR is the most important parameter. It packs almost all costs – from the pure borrowing rate to possible fees – into a single percentage and makes offers comparable at first glance.

But its informative value has limits. What it doesn’t tell you is how flexible the contract is. And it is precisely this flexibility that is worth its weight in gold for self-employed people with fluctuating income. A supposedly cheap loan can quickly turn out to be a golden cage if it leaves you no entrepreneurial leeway.

A low interest rate is a good start, but the true quality of a loan is revealed in the details. The ability to react to unexpected business developments is often worth more than a few tenths of a percentage point in interest rates.

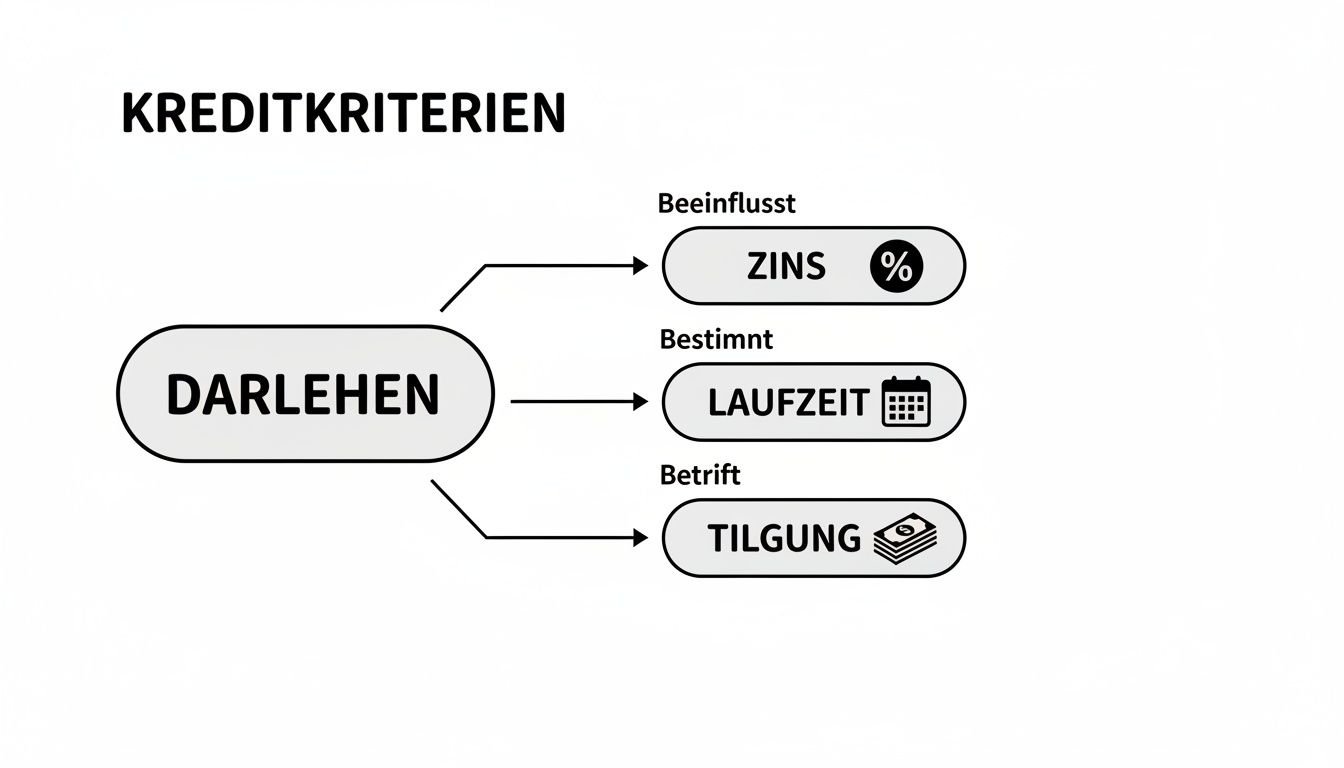

The following graphic puts it in a nutshell: the three most important building blocks of a loan must be in balance.

You can see immediately that interest, term and repayment are inextricably linked. Together, they determine how high your monthly repayments are and how flexible you remain.

Runtime: a strategic tool

The term determines how much time you take to repay the loan. A long term means lower monthly installments – this protects liquidity in day-to-day business. The catch: you pay more interest on the bottom line because the money is “borrowed” for longer.

A short term drives up the installments, but reduces the overall costs noticeably. So what is right? That depends entirely on your situation. Are you planning an investment that will only bear fruit in a few months’ time? Then a longer term can take the pressure off in the initial phase.

-

Scenario 1: The web designer

A web designer needs €15,000 for new office furniture and technology. Her income is stable, but she does not expect any sudden jumps in profits. A term of 60 months (5 years) ensures an installment that she can afford even if an order falls through. -

Scenario 2: The e-commerce retailer

An online retailer needs €50,000 to replenish its stock before the Christmas shopping season. He expects high sales in a short space of time. He therefore chooses a tight term of 24 months to save on interest costs and quickly become debt-free again.

The power of flexible repayment options

For the self-employed, there is hardly anything more valuable than the option of special repayments. A major project has been completed and the last quarter went brilliantly? Perfect. With an unscheduled payment, you can reduce the remaining debt in one fell swoop. This not only shortens the term, but also significantly reduces the overall interest burden.

Take a close look: are unscheduled repayments free of charge and if so, how much? Many banks cap them at a certain percentage per year. The best offers even allow you to repay the loan in full at any time and at no extra cost.

An installment break can be just as important. Is a major customer paying late again or is an unexpected expense tearing a hole in the till? The option of suspending one or two installments can save lives at such times. This flexibility sometimes costs a little extra, but it pays for itself a thousand times over in an emergency.

Good financing adapts to your business rhythm. You can find more detailed information on this in our guide, which explains what you need to know about installment loans.

Direct comparison of loan features for the self-employed

The following table summarizes the most important credit criteria, explains their significance for the self-employed and shows what you should look out for when assessing your creditworthiness.

| Criterion | Significance for the self-employed | What you should look out for |

|---|---|---|

| Effective annual interest rate | The total cost of the loan in one figure. Most important comparative value. | Pay attention to the “2/3 interest rate” that applies to most customers. Is it close to the promotional interest rate? |

| Runtime | Determines the amount of the monthly installment and the total interest costs. | Longer term = lower rate, but higher total costs. Adjust the term to your investment objective. |

| Special repayments | Enables faster repayment in the event of unexpected income. | Are they free of charge? Is there an annual upper limit or is a complete redemption possible at any time? |

| Rate breaks | Creates a financial buffer in the event of unforeseen revenue shortfalls. | How often and under what conditions can installments be suspended? Does this result in additional costs? |

| Fees | Hidden costs that can make the loan more expensive. | Check for processing fees, account management fees or a high early repayment penalty. |

This overview helps you to evaluate offers not only according to the interest rate, but also according to their true practical suitability for your business.

Uncover hidden fees and costs

A transparent loan agreement is the be-all and end-all. In addition to the APR, you should always look out for any extra costs hidden in the small print.

- Processing fees: Now impermissible for normal consumer installment loans, they can still appear for special corporate loans.

- Early repayment penalty: This is a kind of “penalty fee” if you repay the loan in full early. Good contracts limit these costs or waive them completely.

- Account management fees: Sometimes there are monthly fees for the separate credit account. Every little helps.

A reputable loan comparison takes all these points into account. This way, you won’t experience any nasty surprises and can be sure that the promised interest rate really does correspond to the final costs.

Typical hurdles when taking out a loan – and how to overcome them

Anyone who is self-employed knows this all too well: you have a brilliant business idea, a well thought-out plan and the first customers are queuing up – but the path to suitable financing often feels like an obstacle course. Banks traditionally view the self-employed somewhat differently than employees. This has nothing to do with mistrust of your abilities, but is due to the banks’ fixed risk models, which are calibrated for stability and predictability. Exactly what is not always given in the dynamic everyday life of an entrepreneur.

But don’t worry: these hurdles are not insurmountable walls. With the right preparation and knowledge of what banks are really looking for, the typical stumbling blocks can be elegantly avoided. The key is to adopt the lender’s perspective and provide them with exactly the collateral and arguments they need to make a positive decision. In this way, you can turn supposed weaknesses into convincing strengths and act as a reliable business partner on an equal footing.

The dilemma of fluctuating income

Probably the most well-known hurdle for the self-employed is the irregular income. While employees receive a fixed salary every month, your income depends on projects, orders or the season. A strong sales month can be followed by a weaker one. For a bank consultant who calculates in fixed grids, this fluctuation signals a higher risk. The crucial question for him is: can the installment be paid on time even if a major customer makes a late payment?

To dispel this concern, a professionally prepared business management analysis (BWA) is your most powerful argument. A BWA that shows a positive and essentially stable profit trend over a longer period of time – ideally two to three years – is proof: Your business model works and is sustainably profitable despite fluctuations.

My practical tip: Don’t just submit the bare figures. Supplement your documents with a short accompanying letter in which you explain the development plausibly. Explain why certain months were weaker (e.g. due to seasonal effects in the Christmas business) and how you will secure future income. This shows entrepreneurial foresight and that you have your business firmly under control.

The current situation on the credit market is not making things any easier. An analysis shows that only 11% of small self-employed people had any credit discussions at all in the third quarter, compared to 26% in the economy as a whole. Many of them came away empty-handed, as 45% felt that lending practices were restrictive. Find out more about the background to this development at VGSD.

The demand for a long company history

Many banks want a company to have been successful on the market for at least two, often even three years. This is an enormous hurdle for founders and young companies. The reason for this is understandable: The bank wants to see from past figures that your business model is viable and that you have already established yourself.

But here too you can take active countermeasures:

- A convincing business plan: A detailed, realistic and well-researched business plan can go some way to making up for a lack of history. It must show crystal clear how you will generate sales and operate profitably.

- Prove your industry experience: Did you work as an employee in the same industry for years before becoming self-employed? Make sure you emphasize this! It underpins your expertise and reduces the risk in the eyes of the bank.

- equity: A solid equity ratio is a strong signal. It shows that you believe in your idea and are prepared to bear your own risk. A good benchmark is often 20% to 30%.

Our platform helps you to find exactly those providers who are also open to younger companies and whose criteria suit you.

This screenshot of the Finanz-Fox homepage shows how easy it is to access our loan comparison, which is specially designed to filter suitable offers for your individual situation.

The importance of a clean SCHUFA report

For the self-employed, a spotless SCHUFA credit report is even more important than for employees, as it is one of the few external credit assessment bodies. A negative entry almost always leads to an immediate rejection of the application.

You should therefore pay meticulous attention to maintaining an impeccable payment record, both for business and private purposes. It is worth checking your own SCHUFA information regularly to have outdated or incorrect entries corrected immediately. Good preparation really is half the battle here.

A well thought-out approach to applying for a loan can open many doors. Read our tips and tricks for a successful loan application to further improve your chances. If you are aware of these typical hurdles and prepare for them in a targeted manner, you will not come across as a supplicant, but as a competent negotiating partner who has his business under control.

What you should definitely have to hand for a smooth application

Imagine submitting a loan application that is incomplete or carelessly prepared. It’s like an application without a CV – it goes straight into the “no” pile. Especially for self-employed people, whose financial situation is often a closed book for banks, complete and meaningful documents are the absolute key to success. Think of your documents as your financial business card: they show the bank at first glance that you are a reliable partner with a healthy business.

But don’t worry, it’s not rocket science. With the right preparation and the knowledge of what information the bank draws from which paper, you can speed up the whole process enormously. It’s all about proactively ensuring transparency and giving the lender all the pieces of the puzzle for your economic performance on a silver platter.

Your checklist: The most important proofs at a glance

Each individual document tells a piece of your business story. Together they form the overall picture that the bank needs for its credit check. The following documents are almost always indispensable:

- Income tax assessment notices for the last 2-3 years: This is the bank’s official record of your taxed income over a longer period of time. It shows not only how high your profit was, but above all how constant it is.

- Current business analysis (BWA): The BWA, preferably fresh from your tax advisor, is like a current snapshot of your business. It shows at a glance how your turnover and costs are doing in the current year.

- Income statement (EÜR): Many freelancers use the EÜR instead of an elaborate balance sheet. It simply compares your income with your expenses and is the basis for your tax return.

- Bank statements for the last 3-6 months: Yes, the bank wants to see both your business and private account transactions. This gives them valuable insight into your cash flow, payment history and standard of living.

Properly compiling these documents is the be-all and end-all. You can also find detailed tips on preparation in our guide on the most important loan documents for your application.

A well-prepared application demonstrates more than just numbers. It signals professionalism and entrepreneurial diligence. Take the time to present everything completely and clearly – this saves annoying queries and makes a good impression right from the start.

Why every single document counts

Let’s imagine a scenario: Your current BWA shows fantastic profits for this year. At the same time, the tax assessments from previous years show solid, steady growth. This combination is worth its weight in gold for the bank. It signals that your success is not a flash in the pan, but is based on a sustainable business model.

Complete and accurate paperwork is essential for a quick and positive decision. A detailed guide to the components of the annual accounts for SMEs can help you ensure that you have all the financial documents that banks and lenders want to see.

In general, self-employed people often have to overcome higher hurdles. Of course, this includes the basics such as being of legal age, a German residence and a clean credit rating. However, the decisive factor is always proof of economic viability, which is mainly based on tax assessments and the BWA. Many banks also require that you have been self-employed for at least three years.

If you prepare your documents carefully and understand what story they tell the bank, the application process will turn from a chore into a strategic opportunity. You will demonstrate your financial strength and professionalism.

More than just the classic business loan: clever alternatives for the self-employed

Sure, a normal installment loan is the tried and tested classic. But let’s be honest: it’s not always the smartest or even the only solution when you need capital as a self-employed person. Sometimes entrepreneurial reality simply calls for a more creative approach. Fortunately, there are a whole range of strategic financing alternatives out there that are often much better tailored to the needs of freelancers and entrepreneurs.

These options are not stopgap solutions, but real professional tools in your financial toolbox. You can use them to reduce costs, improve your credit rating or gain access to money that you might not be able to access through traditional channels. It is therefore definitely worth broadening your horizons and considering these options in a comprehensive loan comparison for the self-employed.

Debt restructuring: reorganize and reduce the financial burden

Many self-employed people are familiar with this: the overdraft facility is a constant companion in everyday business life – flexible, but unfortunately also damn expensive. The interest on an overdrawn business account can quickly climb to 12% or more. This is often compounded by old, expensive loans for previous purchases. This is precisely where there is huge potential for savings.

Debt restructuring is the perfect solution. It packs all these expensive liabilities into a single, new loan, but on much better terms.

- Imagine this: A photographer is €8,000 in the red with his business account (at 13% interest) and still has an old loan for his equipment for €7,000 (at 9% interest).

- The solution: He takes out a new installment loan for €15,000, for which he only pays 5.5% APR. This enables him to pay off the two old debts in one go.

- The result: his monthly interest burden literally collapses. He has a fixed, predictable installment again and immediately regains his financial overview.

Debt restructuring is much more than just a new loan. It is a strategic new start. It frees up liquidity, improves your credit rating and puts you back in control of your finances.

Strengthen your own creditworthiness with a guarantor

The search for a loan can be a test of patience, especially when you are just starting out or the company’s history is still short. Is the bank hesitant because there is a lack of collateral or the earnings situation is not yet entirely convincing? Then a second person on board can make all the difference.

There are basically two tried and tested ways to do this:

- The guarantor: A third person, often a family member or friend, stands in for you. They contractually undertake to pay the installments if you default. Of course, the guarantor must have a top credit rating and a stable income.

- The second applicant: Here you do not take out the loan alone, but together with someone else – for example your spouse. In this case, both are equal borrowers and are jointly liable. This is often the stronger option because the bank takes the entire joint income as the basis for its decision.

No matter which route you choose: Absolute transparency and trust are the be-all and end-all. Anyone who vouches for you or takes out a loan with you is shouldering an enormous financial responsibility. But the chances of a commitment and significantly better interest rates increase enormously.

Promotional loans: the turbo for founders and investors

An often overlooked, but incredibly attractive alternative are government development loans. First and foremost those from the Kreditanstalt für Wiederaufbau (KfW). These loans are precisely designed to support start-ups, young companies and established self-employed people with important investments.

The advantages are obvious and are not bad at all:

- Unbeatably low interest rates: Interest rates are often miles below what commercial banks charge.

- Repayment-free start-up years: this is worth its weight in gold, especially in the start-up phase. Imagine you only have to pay the interest in the first year or two, but no repayments. This gives you enormous breathing space.

- Exemption from liability for the bank: In many cases, KfW assumes part of the risk if the loan falls through. This naturally makes it much easier for your house bank to say “yes”.

The route to a development loan is almost always via your house bank, which submits the application to the development bank on your behalf. Admittedly, the process is somewhat more complex and nothing works here without a solid business and financial plan. But the effort is more than worth it in most cases. A purchase such as a new company car can also be financed through such programs. Whether leasing or a car loan is the better choice must of course be considered on a case-by-case basis.

How the digital loan comparison works in four simple steps

Enough theory – how does a loan comparison for the self-employed work in practice today? Forget the old paperwork and endless bank appointments. The path to your financing is now surprisingly uncomplicated, fast and, above all, transparent. With the right digital tools, you can find out in just a few minutes which banks really suit you and your business.

This short roadmap will guide you through the entire process in four clear steps, from the initial consideration to the final application. I’ll show you how to get a complete overview of the market in just a few clicks, without compromising your credit rating. The aim is simple: to give you the tools you need to make the right decision for your company with confidence and the best possible information.

Step 1: What do you really need? The needs analysis

At the beginning there is always one question: What exactly do you need the money for and how much? Be as specific as possible here. Is it an investment in new technology, do you want to bridge a liquidity bottleneck or pay off an expensive old loan? A clear definition helps enormously.

You then enter this key data – i.e. the loan amount and the planned term – directly into a digital loan calculator. You also need to enter a few details about your self-employment. This first step is usually completed in under two minutes and forms the basis for everything that follows.

Step 2: The market check – SCHUFA-neutral and non-binding

Now comes the trick that makes modern loan comparisons so valuable. After you have entered your data, a request for conditions from a large number of banks starts in the background. This is absolutely SCHUFA-neutral and has no negative impact on your score. Guaranteed.

Unlike a direct loan application to your bank, the only thing that is checked here is which conditions would be suitable for you. It often only takes a few moments before you have an initial, personalized list of offers that are already roughly tailored to your financial situation.

SCHUFA neutrality is your greatest asset. You can sound out the market, obtain offers and compare them without multiple inquiries affecting your creditworthiness. This gives you the freedom to find the best option without risk.

Step 3: The details decide – the exact comparison

You now have a list of potential loan offers in your hands. Great! Now it’s time to get down to the nitty-gritty, namely the details that we have already looked at in detail.

- Compare not only the interest rates, but always the APR.

- How flexible are you with unscheduled repayments? Is this possible free of charge?

- Is there an option for installment breaks if a month is not going so well?

Choose the offer that not only has the lowest interest rate, but also offers the framework conditions that best suit your everyday business.

Step 4: Everything digital – upload and finalize documents

Once you have found your favorite, the rest is child’s play. You can upload the required documents, such as tax assessments and your current BWA, conveniently online. You can also carry out the identity check (usually via Video-Ident) and sign the contract (using a qualified electronic signature) completely digitally from your desk.

This end-to-end digital process saves an incredible amount of time and nerves. Instead of waiting days for the post, the application is often completed in less than an hour. That’s how easy and secure the path to suitable financing can be today.

Frequently asked questions that self-employed people ask us again and again

After we have gone through the details of interest rates, documents and alternatives, we are often left with a few specific questions. No problem, we know them all too well. Here I have compiled the most common points that are on the minds of self-employed people like you and provide you with clear, practical answers. In this way, we can clear the last stumbling blocks out of the way before you make your decision.

As a founder, can I get a loan at all?

In short: yes, but it’s a tough place. Most house banks wave you off at first because they want to see balance sheets and BWAs from at least two, often even three financial years. Without this history, they find it difficult to assess your risk.

But fortunately there are other ways. A very hot tip is always the state development loans, especially those from KfW Bank. These are precisely designed to help founders, often with unbeatably low interest rates and a grace period at the start. This gives you the breathing space you need.

Some modern FinTechs or specialized providers are also a good place to start. They not only look at the past, but also evaluate your potential. But beware: you need to present an absolutely watertight business plan and, ideally, some equity.

Only one thing counts for founders: the business plan. This is your bible. It must show crystal clear that you understand your business, know your market and how you will realistically earn money. It is the only substitute for missing figures from the past.

Will a credit comparison ruin my SCHUFA score?

I hear this concern all the time, but I can reassure you: A professional loan comparison for the self-employed is absolutely harmless for your SCHUFA score. The trick lies in the type of query that runs in the background.

- Condition inquiry (SCHUFA-neutral): When you compare online, the platforms make exactly this request. The bank only checks without obligation whether you are a suitable customer and on what terms. It’s like window shopping – it leaves no trace in your file.

- Credit application (score-relevant): Things only get really serious when you decide on an offer and make a binding application for the contract. This request is noted. If you do this with ten banks at the same time, it looks like panic to SCHUFA and your score may suffer.

You can therefore obtain various offers and study the small print with complete peace of mind. Only when you tick the box under an application does it become official.

How important is my private income really?

Extremely important. In the case of the self-employed, banks do not see a clear dividing line between company and person. Your business success and your personal financial discipline are two sides of the same coin for lenders.

The bank does the hard math: What is left over at the end of the month after rent, living costs, insurance and all business expenses have been paid? This amount must easily cover the loan installment. A clean housekeeping book and a good private SCHUFA score are therefore just as important as a shiny BWA. A second income, for example from your partner, is of course a real wild card and can massively increase your chances of approval.

Ready to find the right financing for your business? At Finanz-Fox, we have made the process as simple and transparent as possible for the self-employed – everything is digital. Find out now, without obligation, which conditions really suit you and your project. Lay the foundations for your next big project. Compare loan offers now.