Put simply, debt restructuring is worthwhile as soon as the interest savings from the new, cheaper loan exceed the costs of switching. The key point is the loan rescheduling comparison: if you find an offer with significantly lower interest rates than your old loan, you can significantly reduce your monthly installment. This eases the strain on your budget and can save you hundreds or even thousands of euros over the term of the loan.

When a loan restructuring really pays off

Debt restructuring is much more than just a financial product – it is a strategic decision to regain full control of your own finances. However, this step is not suitable for everyone and in every situation. The trick is to find the perfect time when the benefits clearly outweigh the potential costs.

The most common and at the same time strongest motivation for debt restructuring is a change in the interest rate environment. Perhaps you took out your loan a few years ago at a very high interest rate, but market interest rates have fallen significantly since then? If so, there is an enormous savings potential here that you should exploit.

Using the current interest rate environment as an opportunity

The interest rate trend is actually playing into your hands at the moment. Current data from the German Bundesbank shows that interest rates for new consumer loans are trending downwards. For example: In October 2025, the average APR was 7.33 percent. If the interest rate on your old loan is significantly higher than this, now could be the ideal time to save money by restructuring your debt. If you want to know exactly, you can find the details in the Bundesbank’s interest rate statistics.

Debt restructuring makes particular sense in these three core scenarios:

- Interest rate reduction: You replace an expensive old loan with a new one with a noticeably lower interest rate.

- Installment reduction: You extend the term of the new loan in order to reduce the monthly charge and thus create a greater financial buffer.

- Loan bundling: You bundle several loans – for example an old installment loan, the overdraft facility and the credit card bill – into a single, clear loan with just one installment.

A reality check before the comparison

Before you plunge into a direct comparison, you need to take an honest inventory. A loan rescheduling comparison is only useful if you have a crystal-clear picture of your starting position.

The key to success is to keep an eye on the total costs. A lower monthly payment alone is no guarantee of real savings if the term is disproportionately longer. Real financial relief comes when you reduce the total interest burden over the entire term.

Let’s take a look at the specific situations in which debt restructuring can be particularly advantageous and what is important in detail.

| Scenario | Main objective | Ideal for … | What to look out for |

|---|---|---|---|

| Repay individual loan | Minimize interest costs | Borrowers with expensive old contracts who want to benefit from a lower interest rate environment. | The interest savings must significantly exceed any early repayment penalty. |

| Reduce monthly installment | Increase liquidity | People whose financial situation has changed and who need more room for maneuver each month. | A longer term can increase the overall costs. The rate should not be set too low. |

| Bundle several loans | Create an overview & save interest | People with several small liabilities (overdrafts, installment purchases) to regain an overview. | The new total interest rate should be noticeably lower than the average interest rate of the old loans. |

Each of these goals requires a slightly different approach when comparing offers. It’s not just about chasing the lowest interest rate, but finding the terms that fit your personal financial plan exactly. If you want to dive deeper into the basics, we recommend our guide on the art of financing and installment loans.

Compare loan offers: What really matters

Anyone thinking about debt restructuring is often faced with a mountain of offers. At first glance, many of them look tempting, but as is so often the case, the devil is in the detail. In my practice, I have seen countless cases where people have been blinded by the high interest rate alone – a mistake that can end up being really expensive.

A good loan rescheduling comparison is more than just hunting for the lowest interest rate. It’s about finding the total package that is not only favorable today, but also flexible enough for what comes tomorrow.

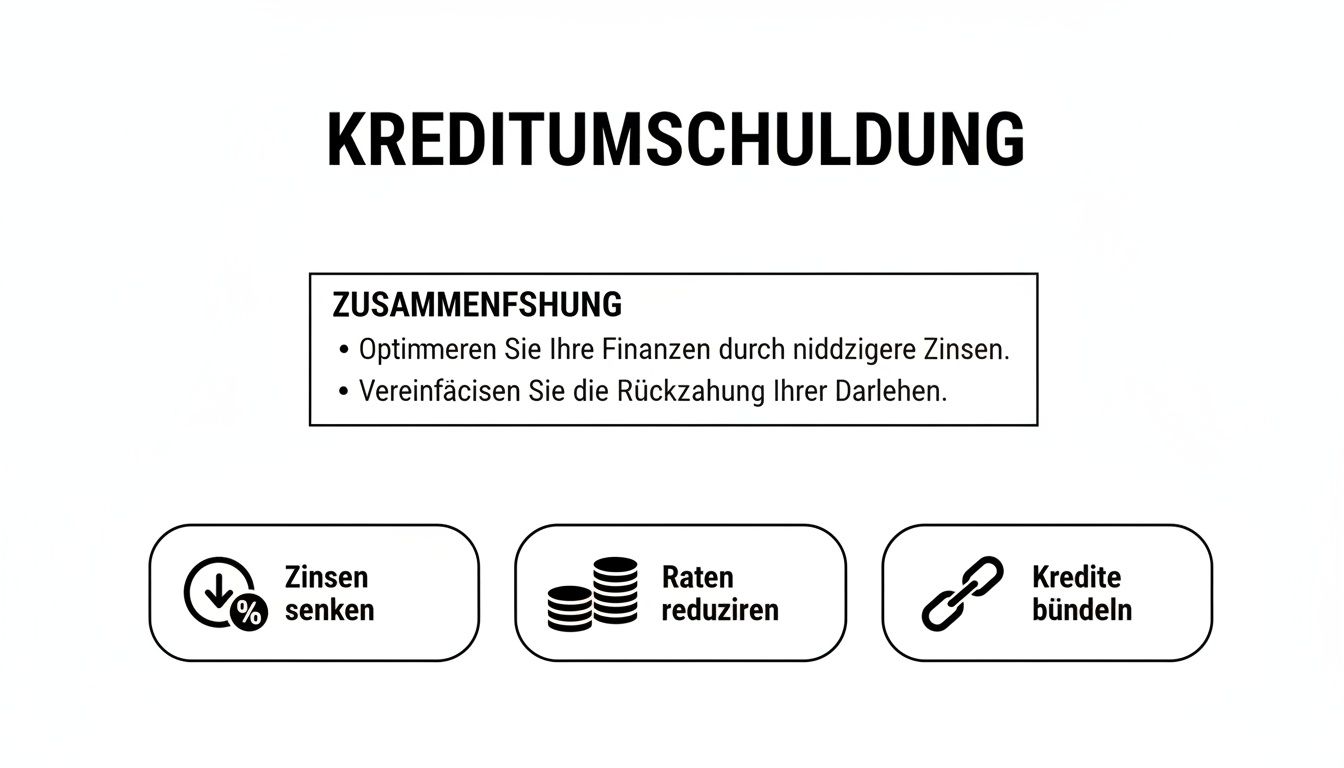

Most people want to achieve three things with debt restructuring, as the chart nicely summarizes.

You can see straight away that it’s not always just about saving. The aim is often to reduce the monthly burden or to finally get a clear overview of your finances again by bundling several loans into one.

More than just the borrowing rate

Of course, the first thing everyone looks at is the interest rate. But this is exactly where the first trap lurks. Banks like to advertise the borrowing rate because it looks lower and therefore more attractive. But this is only half the story, because it only describes the pure cost of the money borrowed.

In the end, only one figure counts for you: the APR. It is the truly honest currency when comparing loans. Required by law, it includes almost all costs incurred – such as processing fees. This is the only way to get a realistic picture of what the loan will actually cost you per year.

A low borrowing rate is often just a decoy. When comparing offers, only look at the effective interest rate. This is the only value that tells you the true costs.

Flexibility as a priceless advantage

Life rarely sticks to plans. An unexpected bonus at work, a small inheritance or a broken washing machine can change your financial situation from one day to the next. And it is precisely at such moments that it becomes clear whether you are holding a good or just a cheap loan agreement in your hand.

You should therefore pay very close attention to the option for free unscheduled repayments. Can you pay in extra money at any time to get out of debt faster and save interest? Some providers only allow this up to a certain amount per year or charge annoying fees.

Installment breaks can be just as valuable. If you run into a bottleneck through no fault of your own – whether due to short-time work or a high vet bill – the option to skip one or two installments can be a huge relief. A flexible contract gives you this safety net.

The hidden cost trap: residual debt insurance

It comes up in almost every loan discussion: residual debt insurance (RSV). It is intended to cover you if you are no longer able to make your repayments due to unemployment, illness or death. It sounds caring, but in reality it is often an overpriced additional benefit.

The problem is that the costs for RSV are usually simply added to the loan amount and co-financed. This not only drives up the installment, but also the total costs. What’s more, the insurance conditions are often full of exclusion clauses. So think carefully about whether you really need this protection – especially if you already have term life or occupational disability insurance.

If you would like to delve even deeper into the subject, take a look at our guide Loan comparison made easy: How to find the best deal. You’ll find more valuable practical tips there.

To help you keep track of your comparison, I have summarized the key points in a matrix. Think of it as your personal checklist for putting loan offers through their paces.

Comparison matrix for debt rescheduling loans

This table compares the most important criteria for comparing debt rescheduling loans and helps you to separate the wheat from the chaff.

| Criterion | What you should look out for | Finanz-Fox recommendation |

|---|---|---|

| Effective annual interest rate | Only compare this value. It must include all significant costs. | The lowest effective interest rate is often the best offer, but only in combination with suitable conditions. |

| Special repayments | Are these free of charge and unlimited? Are there annual limits? | Look for offers that give you maximum flexibility in repayment without additional costs. |

| Rate breaks | Is it possible to suspend installments in the event of financial bottlenecks? | A contract with the option of installment breaks provides an important safety net for unforeseen events. |

| Runtime | Does the term suit your life planning? A shorter term saves interest. | Choose the shortest possible term with an installment that you can comfortably afford. |

| Residual debt insurance | Is it optional? Have the costs been included transparently in the effective interest rate? | In most cases, refuse RSV unless an individual risk analysis shows a clear necessity. |

With these criteria in mind, you are well equipped to find a loan offer that really helps you and doesn’t have any nasty surprises in store.

How to calculate your personal savings potential

Theory about interest rates and terms is one thing. But actually seeing what’s left in your account at the end of the month – that’s what counts. So let’s leave the dry figures behind us and take a look at what’s in it for you in practice. Using two very typical examples, I’ll show you how you can significantly improve your financial situation with a targeted loan restructuring comparison.

These calculations are like a template that you can use to easily understand your own potential savings. The point is to get a feel for what is really possible and how the mechanics behind it work.

Scenario 1 The classic redemption of an expensive old loan

Imagine this: Three years ago, you took out an installment loan for €15,000. Term 60 months, effective interest rate 7.5% – a completely normal offer at the time. Your monthly installment is just under €299. After 36 months, a good portion has already been paid off, but there is still a residual debt of €6,450 on the books.

Now you discover a much better offer by making a comparison: another bank would finance the remaining debt for a mere 4.5% APR for the remaining 24 months.

Let’s take a closer look at the figures:

- Old loan: In the next 24 months you would still pay interest of € 526.

- New loan: With the new offer, interest is only €305.

- Early repayment penalty: Your old bank charges a small fee for early repayment. By law, this is limited to a maximum of 1% of the remaining debt, i.e. €64.50.

The calculation is very simple: € 526 (old interest) – € 305 (new interest) – € 64.50 (costs) = € 156.50 savings. That’s over €150 that you save without any extra effort, just by making a clever switch. A nice side effect: your monthly installment also drops slightly to around €281.

Scenario 2 Clever bundling of multiple liabilities

This scenario is a little more complex, but this is often where the greatest savings potential lies hidden. Let’s assume your everyday financial life looks like this:

- Installment loan: Remaining debt €4,000 at 9.0% interest, installment €150

- Overdraft facility: permanently €2,500 in the red at 12.5% interest

- Credit card: A balance of €1,500 is paid off at an expensive 14.0% interest rate

It adds up quite a bit every month and you quickly lose track of everything. You pull the ripcord and decide to bundle everything into a single new loan for €8,000. Using a comparison portal such as Finanz-Fox, you find an offer with an APR of 5.5% and a term of 60 months.

Consolidating debt is more than just financial optimization. It is a liberating step that turns an opaque jumble of installments and interest into a single, clear and controllable liability.

Let’s do the math. Your new, single monthly payment is now €152. That alone is a huge relief when you consider that the installment loan alone used to cost €150 – not even counting the interest on the overdraft facility and credit card.

Over the entire five years, you will pay a total of €1,120 in interest on the new loan. If you had simply let the old debt continue, the interest costs would have been astronomical, especially because of the wickedly expensive overdraft and credit card interest. The savings here are quickly in the four-digit range.

These examples make it clear: a strategic loan rescheduling comparison is not rocket science, but a real, tangible tool for more financial control. Whether you want to optimize a single loan or reorganize your entire financial setup, calculating your savings potential is the first and most important step. If you want to delve deeper into how to set up your application correctly from the start, you’ll find valuable tips and tricks for a successful loan application in our guide.

How to skillfully navigate around the cost traps of debt restructuring

At first glance, debt rescheduling often promises the blue sky: lower interest rates, a lower monthly payment – simply more room to breathe. But if you don’t look closely, you can quickly fall into one of the many cost traps. The hoped-for financial advantage can then quickly turn into the opposite.

The truth is: a successful loan rescheduling comparison doesn’t just depend on comparing interest rates. You also need to understand the small print and know the typical pitfalls in order to make real savings.

The biggest chunk: The early repayment penalty

When we talk about costs, one item is almost always at the top of the list: the early repayment penalty. This is basically a form of compensation for the bank because it loses out on future interest income due to your early repayment. Many people are put off by the mere thought of it, but the amount of this fee is anything but arbitrary.

Fortunately, the legislator has drawn clear boundaries here:

- A maximum of 1% of the remaining debt if your loan has been outstanding for more than one year.

- A maximum of 0.5% of the residual debt if the remaining term is less than twelve months.

This statutory cap makes the costs calculable. The amount is often surprisingly manageable and should not deter you from debt restructuring. The key is to know this amount precisely and include it in your calculation. The rule of thumb is: the savings from the new, cheaper loan must significantly exceed the prepayment penalty.

Residual debt insurance – often an expensive extra

Another classic that you will come across when talking to the bank is residual debt insurance (RSV). It is designed to protect you if you are unable to pay your installments due to unemployment or illness. This sounds like a sensible thing at first, but on closer inspection it often turns out to be an overpriced product with lots of loopholes.

The catch: the costs for the RSV are usually added directly to the loan amount and interest is added over the entire term. This not only pushes up the total costs, but also your monthly expenses. So ask yourself honestly whether you really need this protection. Often, existing insurance policies, such as term life or occupational disability insurance, are already a much better and cheaper protection.

If you are offered residual debt insurance, don’t turn it down immediately, but be skeptical. Ask for a crystal-clear breakdown of the costs and rummage through the insurance conditions – pay particular attention to exclusion clauses. In the vast majority of cases, you will be much better off financially without this supplementary insurance.

The maturity trap: short-term relief, long-term costs

For many people, a lower monthly payment is the main aim of debt restructuring. Banks are happy to comply with this wish, often with a simple trick: they extend the term of the new loan. Absolute caution is advised here! Even if the monthly installment is lower, you may end up paying much more interest than before.

Imagine this: You pay off a loan with 36 months remaining and sign a new contract for 72 months. Even with a better interest rate, the doubled term can mean that the total interest costs end up being higher. Your monthly liquidity may have improved, but in the long term you have made a bad deal.

Your checklist for avoiding cost traps:

- Early repayment penalty in black and white: Ask your old bank for an exact calculation of the remaining debt and the compensation due. Do not rely on estimates.

- Compare total costs, not just the installment: do the math. What will the old loan cost you until the end (remaining interest + installments)? And what does the new loan cost (total interest + all fees)?

- Critically examine (and usually reject) residual debt insurance: Say no, unless an honest analysis of your personal situation shows that you are taking an incalculable risk without this protection.

- Consciously control the term: Always aim for the shortest possible term that you can afford. A longer term should be the absolute exception for a financial bottleneck, not the rule.

A thorough debt restructuring comparison that takes these points into account will ensure that your debt restructuring is exactly what it should be: Your path to more financial freedom and real, tangible savings.

How to restructure your debt with Finanz-Fox – explained step by step

Debt restructuring that really pays off in the end doesn’t fall from the sky. It is the result of a well thought-out strategy. This is exactly where we come in. At Finanz-Fox, we have designed the process in such a way that it is not only easier for you, but above all crystal clear and comprehensible. Let’s walk the path together from the initial idea to the new, better loan.

The idea of getting rid of expensive old loans and saving money in the process is not a purely private matter. Even the German government is doing it and optimizing its finances in this way. The Federal Audit Office recently reported that the credit authorization for unscheduled debt rescheduling in the 2025 Budget Act was doubled from 15 to a whopping 30 billion euros. What is good for the state can only be right for you: Replacing old, expensive debt with new, cheaper debt is simply a clever financial move. If you want to find out more, you can find the details in the report by the Federal Audit Office.

Phase 1: Optimal preparation

To be honest, good preparation is half the battle. It not only saves time, but also nerves. So before you dive into the loan rescheduling comparison, take a moment to gather everything you need. If you then have everything ready in the application process, the bank can process your request at lightning speed.

Ideally, you should have these documents ready:

- Your old loan agreements: They contain all the important information such as the original loan amount, the interest rate and the contract number.

- The current residual debt: Ask your old bank for the current repayment amount. This is the exact amount you need for the new loan.

- Proof of income: The last three payslips are usually sufficient.

- Bank statements: Have the last one to three months’ statements showing your incoming salary ready.

- Identity card or passport: You will need this later for the identity check.

With this stack by your side, the next step is child’s play.

Phase 2: The comparison with the Finanz-Fox loan calculator

The heart of every debt restructuring is the tough comparison. Our Finanz-Fox loan calculator is designed to do just that – it makes it as easy as possible for you. It guides you intuitively through the necessary information and spits out a clear overview with suitable offers in just a few minutes.

How to get the best out of your computer:

- Select the intended purpose: Enter “debt restructuring” directly. This tells the banks immediately what you intend to do.

- Enter loan amount: Enter the exact remaining debt of your old loans here. No more and no less.

- Determine the term: Play around a little here until you find a term that leads to a monthly installment that is convenient for you.

You will see how easy it is to calculate different scenarios.

Here you can see the simple input mask of our calculator. You can adjust the loan amount and term and immediately see how the monthly installment changes. This gives you an initial feeling for the possible interest conditions.

Phase 3: The digital application and our experts at your side

Have you found an offer that suits you? Perfect, then it’s time for the digital application. At Finanz-Fox, you can complete everything conveniently online – your data is of course transmitted securely and encrypted. You can then complete the identity check, known as legitimation, from the comfort of your own home using Video-Ident.

And this is the part where our personal advice makes the real difference. As soon as we receive your application, your personal Finanz-Fox expert takes over. We go through your documents again, follow up with the banks for you and negotiate to get the best deal for you.

We see ourselves as your advocate with the banks. Our job is to make the entire process as stress-free as possible for you and to ensure that you end up signing the contract that fits your life perfectly. At Finanz-Fox, we combine smart digital processes with genuine, personal advice from person to person.

Debt restructuring and SCHUFA score: what you really need to know

The fear of ruining your SCHUFA score by rescheduling your debt runs deep for many people. So deep that they would rather forego better interest conditions than even think about it. But this worry is usually completely unfounded. Quite the opposite: a cleverly approached loan rescheduling comparison can even improve your credit rating in the long term.

The crux of the matter lies in the type of request. If you simply obtain and compare offers, this only triggers an “inquiry about credit conditions” at SCHUFA. This is absolutely neutral and has no negative impact on your score. You can therefore request several conditions with peace of mind. Only when you sign a loan agreement does it become a binding “credit inquiry”.

First a small setback, then the big leap forward

Of course, your SCHUFA score may go down a little in the short term immediately after taking out the new debt rescheduling loan. However, this is a completely normal, automated process. A newly taken out loan is initially a risk from a statistical point of view – until you prove otherwise by paying your installments on time.

In the long term, however, the positive effects almost always outweigh the negative ones. As soon as your old loan is reported as “settled” and the installments for the new one flow on time, you send a strong signal of financial reliability. It is particularly advantageous if you bundle several small loans into one. This not only cleans up your finances, but is also seen by SCHUFA as clever and responsible financial management.

Debt restructuring is not a blemish on your SCHUFA file. Rather, it is a sign that you are proactively managing and optimizing your finances. It proves that you have your liabilities under control – a strong plus for your creditworthiness.

Financial stability is more important than ever, especially in today’s world. Over-indebtedness in Germany has risen again in 2025. The DebtorAtlas Germany 2025 shows that 5.67 million people are affected – that’s 111,000 more than in the previous year. As the latest analysis by Creditreform shows, debt restructuring is a powerful tool for reducing the monthly burden and actively preventing over-indebtedness.

However, your creditworthiness is more than just the SCHUFA score. There are other important credit agencies. So to maximize your chances of getting the best conditions, it may be worth learning how to improve your Creditreform score.

At the end of the day, a well thought-out debt restructuring will strengthen your financial fitness, which will also be reflected in your credit report. If you would like to delve deeper into the subject, you can find more valuable information in our articles on SCHUFA.

The most frequently asked questions about loan rescheduling – short and sweet answers

Finally, I would like to address the questions that I am asked time and again in consultations on the subject of debt restructuring. Here you will find clear answers from practical experience so that you can make your decision with a good feeling.

When is the right time for debt restructuring?

Quite simply, the best moment has come when the current market interest rates are noticeably lower than the interest rate on your old loan. This is the classic situation in which debt restructuring really pays off.

But other life circumstances can also be a good reason. Perhaps your income has changed and you need a lower monthly installment to give you more breathing space again. Or you’ve simply lost track of several small loans and want to bundle everything into a single, predictable installment.

As a rule of thumb, the savings from the new, lower interest rates should easily offset any costs incurred, such as a possible early repayment penalty. If there are only a few hundred euros left to pay off, the cost is usually no longer worth the benefit.

What costs should I expect for debt restructuring?

The largest item that may be incurred is the early repayment penalty. This is basically compensation for your old bank because it loses interest due to your early repayment. But don’t worry, this is not an arbitrary amount, it is clearly regulated by law:

- With a residual term of more than one year, the bank may demand a maximum of 1% of the residual debt.

- If the contract runs for less than one year, it is only a maximum of 0.5% of the remaining debt.

These costs are therefore transparent and can be calculated precisely. Furthermore, reputable providers generally do not charge any additional fees for the debt restructuring itself.

One of the biggest, often underestimated advantages of debt restructuring is the newfound order in your finances. Instead of a jumble of different installments, due dates and interest rates, you end up with a single, clear installment. This feeling of control alone is priceless for many people.

Will a debt restructuring worsen my SCHUFA score?

I can reassure you here: No, quite the opposite. If you start a comparison via portals such as Finanz-Fox, it is purely a request for conditions. This is absolutely SCHUFA-neutral and has no influence whatsoever on your score.

Once the debt restructuring has been completed, the score may fall slightly in the short term – this is a normal technical process – but it recovers very quickly.

In the long term, debt restructuring is even good for your credit rating. It shows that you are actively managing your finances. By combining several loans into one, you reduce the number of creditors. Punctual payments of the new, often lower installment then prove your reliability. This strengthens your reputation with banks instead of weakening it.

Can I actually refinance any loan?

In principle, yes: classic installment loans, car loans or even the expensive overdraft facility on your current account can usually be restructured without any problems. Things get a little trickier with mortgage loans, as completely different rules and often significantly higher early repayment penalties apply here.

The most important prerequisite is and remains your creditworthiness. The new bank will check whether you are creditworthy. However, as long as your financial situation is stable and you pay your bills on time, nothing should stand in the way of debt restructuring.

Are you ready to take your finances into your own hands and save money? The Finanz-Fox loan calculator is the perfect place to start. Find out how much you can save without obligation and compare the best offers on the market.

Start your free loan comparison here on finanz-fox.de