Debt restructuring is a smart move if it saves you money at the end of the day. This can be the case if you replace an old loan with high interest rates with a new, significantly cheaper one or if you bundle several expensive loans into a single, manageable installment. It’s basically a strategic financial move that will help you reduce your monthly burden and regain control of your finances.

What debt restructuring means for you personally

Think of your current loans as a rucksack that you carry around with you every day. Every single loan is a stone in it. Debt restructuring is like completely repacking this rucksack: you throw out the heavy, unwieldy stones and replace them with a single, lighter one. The aim? To lighten the load noticeably.

Ultimately, the aim is to improve your financial situation. This usually happens in three ways:

- More favorable interest rates: You replace an old, expensive loan agreement with the usual interest rates at the time and secure the much better conditions currently available.

- More overview, less chaos: instead of many small installments from different accounts, you only have one single direct debit and one contact person. This creates clarity.

- Suitable conditions: You can arrange the new term so that the monthly installment fits your budget better – or you can pay off the loan faster if you can afford it.

A financial lifeline in uncertain times

Especially when the economic situation is tense, the burden of old loans is felt particularly keenly. The latest Debtor Atlas Germany from Creditreform paints a clear picture here: 5.67 million people in Germany are over-indebted, which corresponds to an increase of 2.0 percent compared to the previous year. Experts often believe that the reason for this is that many people have simply used up their financial buffer. This is precisely where debt restructuring can be an effective way of reducing monthly fixed costs and giving you room to breathe again.

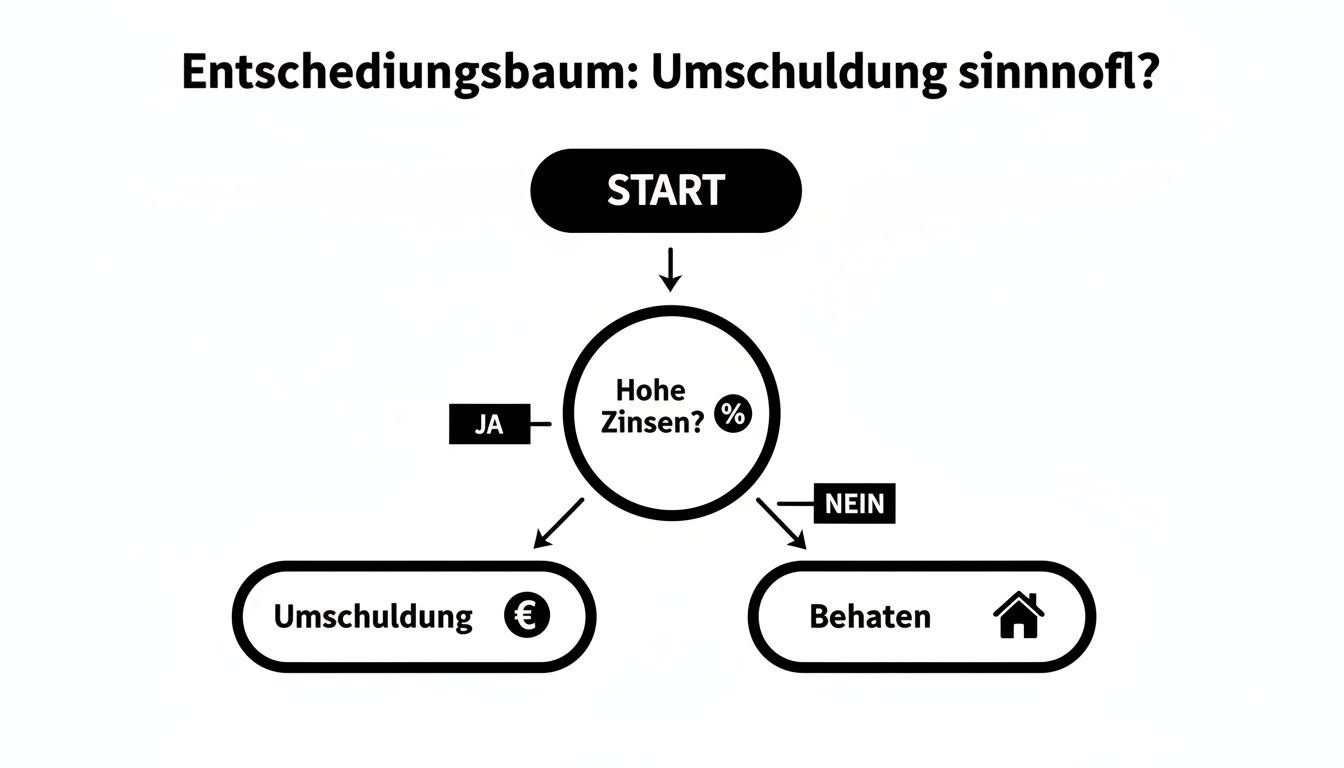

The key question is actually quite simple. The following decision tree gets to the heart of the matter.

This chart clearly shows that if your current interest rates are noticeably higher than what is usual on the market today, you should definitely consider debt restructuring. It is almost always a smart financial move. Incidentally, such considerations are not only crucial for small loans, but also for large financings, as you can read in our guide to real estate financing.

Quick check whether debt rescheduling is advantageous for you

This table will help you to make a quick decision as to whether debt restructuring might make sense in your current situation.

| Your situation | Debt restructuring probably makes sense | Debt restructuring does not make sense |

|---|---|---|

| Interest rate level | Your current loan interest rates are significantly higher than the current market interest rates. | You already have a very favorable interest rate that is below the current level. |

| Number of loans | You have several installment loans, overdraft facilities or credit card debts. | You only service a single loan with good conditions. |

| Monthly installment | Your total monthly burden is too high and you need more financial leeway. | You can pay your current installment without any problems and are satisfied with the term. |

| Creditworthiness | Your credit rating has improved since you last took out a loan (e.g. higher income). | Your credit rating has deteriorated, which makes it more difficult to find more favorable offers. |

In short: the more points in the middle column that apply to you, the more seriously you should consider debt restructuring. It could be really worthwhile for you.

The three most important reasons for debt restructuring

Debt restructuring is not some hocus-pocus that simply makes debts disappear. But look at it this way: it’s an extremely clever tool to get your finances back on track and make the most of your situation. It’s about not just managing existing debt, but managing it more intelligently. Let’s take a look at the three classic scenarios in which debt restructuring makes sense and almost always pays off.

Each of these situations is a real opportunity to reduce your monthly burden, take back control and save a lot of money in the long run.

1st interest rate cut: The most obvious money advantage

The most common and at the same time simplest reason for debt restructuring? Quite clearly: to benefit from lower interest rates. If you took out your loan a few years ago, you are probably paying an interest rate that is simply no longer competitive on the market today. A difference of just a few percentage points can amount to savings of several thousand euros over the entire term.

Think of it like an old cell phone contract. You’ve been paying for ages for a package that is now much cheaper with a new provider. Switching saves you money month after month. Exactly the same principle applies to loans.

Debt restructuring is fully effective if the interest savings from the new loan significantly exceed the costs incurred, such as a possible early repayment penalty.

This idea is even gaining momentum at the moment. A survey by CBRE has shown that almost 80 percent of lenders in Europe want to grant more loans again. A huge refinancing requirement of around 70 billion euros is heating up the competition. What does that mean for you? There is a damn good chance of benefiting from attractive conditions and getting rid of expensive old loans.

2. tame credit chaos and regain control

Hand on heart: do you still have a complete overview? There’s the installment loan for the car, the constantly overdrawn overdraft, the financing for the new kitchen and perhaps an outstanding credit card bill. It all quickly adds up to a confusing financial jungle. Every month, different providers debit different amounts on different days – each with their own, often far too high interest rate.

Debt restructuring brings order back into the chaos. You consolidate all existing debts into a single, new loan. The benefits are immediate:

- One installment, one contact person: no more payment confusion. You now only have a single, clearly plannable monthly installment.

- Lower overall costs: Interest rates for overdraft facilities or credit cards are often outrageously high. A classic installment loan is almost always the much cheaper choice.

- Better credit rating: A single loan that you service reliably often looks better to credit agencies such as SCHUFA than many small, scattered debts.

This step not only simplifies your life, but can also noticeably reduce your total monthly burden. If you would like to delve deeper into the world of loans, you will find everything you need to know in our article on the art of financing with installment loans.

3. adjust the term and installment to your life

Life rarely stands still, and your financial situation changes with it. Perhaps you’ve had a pay rise and now want to get rid of your debts more quickly. Or there are unexpected expenses, your income has temporarily decreased and you simply need more breathing space in the short term.

This is exactly where debt restructuring shows its flexibility. You can adapt the conditions of your loan to your current phase of life. You can either shorten the term to be debt-free more quickly and save on interest costs. Or you can extend the term, thereby reducing the monthly installment and easing the strain on your budget. This makes debt restructuring a strategic tool that you can use to manage your finances with foresight.

This is how much you can save by rescheduling your debt

Theory is all well and good, but what really counts in the end is what’s left in your wallet at the end of the day. The best way to answer the question of whether debt restructuring makes sense is to see the savings potential in black and white. So let’s make things concrete and look at three typical everyday situations in which debt restructuring makes a real financial difference.

These examples should give you a feel for where you might be and how much room for improvement there is in your financing. You will be amazed at what a simple adjustment can sometimes achieve.

Example 1: The Müller family’s expensive old loan

Imagine the Müller family. A few years ago, they bought new furniture and took out an installment loan for €15,000. The interest rates were okay back then, but from today’s perspective? Quite expensive. They are still paying an APR of 7.9%.

Now they have looked around and found a debt restructuring offer for an unbeatable 3.5% interest rate. The remaining term remains the same for both loans: 48 months. Let’s see what that means for the family fund.

The difference is immediately noticeable. Let’s take a look at the figures in direct comparison to illustrate the savings potential.

Before and after comparison using the müller family as an example

| Parameters | Old credit | New debt rescheduling loan |

|---|---|---|

| Credit | 15.000 € | 15.000 € |

| Interest rate | 7,9 % | 3,5 % |

| Remaining term | 48 months | 48 months |

| Monthly installment | approx. 365 € | approx. 335 € |

| Interest costs (remaining term) | approx. 2.520 € | approx. 1.080 € |

| Savings | – | 1.440 € |

The monthly installment immediately drops by €30, giving the family more financial leeway every month. But the real highlight is the total saving: over the remaining term, the Müller family saves over €1,400 in pure interest costs. An amount that easily recoups the small outlay for the comparison and the switch.

Example 2: Mr. Schmidt’s credit chaos is sorted out

Do you know this? A credit card here, an overdraft facility there – Mr. Schmidt has lost track over the years. His overdraft facility is constantly €3,000 in the red, at a horrendous 12% interest rate. Then there’s an outstanding credit card bill for €2,000, which costs 14%, and an old small loan for €5,000 with 8% interest.

Not only is his monthly burden high, it is also completely unmanageable. He pulls the ripcord and bundles everything into a single debt restructuring loan for €10,000. His new offer: a fair 4.5% interest rate with a term of 60 months.

The greatest leverage in debt restructuring often lies in replacing extremely expensive loans such as overdrafts or credit cards with a low-cost installment loan. This is where the greatest savings potential lies dormant.

Let’s do the math:

- Before: Interest costs of around €53 per month are incurred for the overdraft facility and credit card alone – without a single cent having been repaid! Then there’s the installment for the small loan. His financial situation is chaotic and expensive.

- Afterwards: He only has a single, clearly plannable installment of around €186 per month.

Mr. Schmidt thus not only drastically reduces his total monthly burden, but also regains control of his finances. Over the years, he will save thousands of euros in interest. Incidentally, our article on comparing loans reveals how to track down the best offers.

Example 3: Mrs. Weber’s desire to be debt-free more quickly

Mrs. Weber has everything under control. Her remaining debt is €10,000 with a solid interest rate of 5%. There are still 48 months to pay off. She recently got a pay rise and wants to use the money to get rid of her debt more quickly. Her goal: to be financially free sooner and save on interest.

She decides to reschedule her debt, reducing the term to 36 months. The interest rate remains the same, but the impact on the total costs is enormous.

- Original term (48 months): In the end, she would have paid a total of around €11,050 for her loan.

- Shortened term (36 months): With the new plan, the total costs fall to around €10,780.

Sure, her monthly installment increases slightly as a result. But the bottom line is that she saves almost €270 in interest and is debt-free a whole year earlier. This example shows impressively that debt restructuring is not only a tool for reducing installments, but also for strategically accelerating repayment.

What you should know about costs and pitfalls

Debt restructuring often sounds like the perfect solution on paper – and in many cases it is. But getting there can have a few unexpected pitfalls. Think of it as a shortcut that looks great on the map but is full of potholes in reality. If you know these stumbling blocks, you can skilfully avoid them and make sure that all the effort really pays off in the end.

By far the biggest hurdle on this path is often the so-called early repayment penalty. The word sounds cumbersome, but the idea behind it is quite simple: it is a kind of compensation for your old bank because it loses interest as a result of your early termination.

The sticking point: correctly estimating the early repayment penalty

Imagine you have taken out a cell phone contract for 24 months. If you want to cancel after a year, the provider will charge you for the lost income. Your bank thinks very similarly. It has firmly planned on the interest income over the entire term. If you repay the loan earlier, it will incur a financial loss that it will have to reimburse.

However, the bank may not proceed completely arbitrarily here. The legislator has set clear upper limits to protect consumers:

- 1.0% of the remaining debt: If your old loan is still outstanding for more than one year, the bank may demand a maximum of 1.0% of the remaining loan amount as compensation.

- 0.5% of the remaining debt: If the remaining term is less than one year, this maximum rate is even reduced to just 0.5%.

So before you sign anything new, the first and most important step is to ask your old bank for the exact redemption amount, which already includes the early repayment penalty. This is the only way you can properly calculate whether the interest savings on the new loan will easily recoup these costs.

Caution: Hidden fees in the new loan agreement

Have you got a great offer on the table with a temptingly low interest rate? Congratulations! But take a moment to read the small print in the new contract. Sometimes there are additional costs lurking there that will eat up your nice savings.

Keep an eye out for processing fees, account management fees or expensive additional services. A well-prepared loan application helps to avoid such pitfalls from the outset. We show you how to significantly improve your chances of a successful application in our guide on how to finance properly.

Debt restructuring is only a win-win situation if the total cost of the new loan – i.e. including all fees and the early repayment penalty – is lower than the amount you would have had to pay for the old loan.

Incidentally, this principle is not just a private matter. Even the German government uses debt restructuring on a grand scale to optimize its finances. The Federal Audit Office recently reported a doubling of the credit authorization for unscheduled debt rescheduling to 30 billion euros because the volume is growing rapidly. This shows that replacing expensive debt with cheaper debt is a smart economic strategy – for governments as well as for you.

The residual debt insurance cost trap

Another point that should make you prick up your ears is residual debt insurance (RSV for short). When you take out a new debt rescheduling loan, you are often warmly recommended to take out a new, usually quite expensive insurance policy at the same time. Absolute caution is advised here.

Go through these three points before you sign:

- Do I really need this? Check whether you are already covered elsewhere, for example by term life or occupational disability insurance. Often, additional personal accident insurance is simply superfluous.

- Can I take my old insurance with me? Sometimes it is possible to simply transfer the protection of your old loan to the new one. This is almost always the cheaper option.

- How much does the fun cost? If new insurance is unavoidable, make sure you obtain comparative offers. The price differences are often enormous.

Don’t let yourself be put under pressure at this point. Unnecessary or overpriced residual debt insurance can wipe out all your savings. With this knowledge, however, you are well equipped to avoid the typical pitfalls and make a really smart decision for your finances.

Your roadmap to successful debt restructuring: explained step by step

Now let’s get started. You’ve realized that debt restructuring could be a real opportunity for you and you’re ready to get started. Perfect! I will take you by the hand and guide you through the entire process – from the initial, honest inventory to the final repayment of your old loans. Simply regard this guide as your personal navigation system that will take you safely to your financial destination.

The entire route is divided into five logical and easily digestible stages. This means you always have a complete overview and can be sure that you are making the right decision.

Step 1: Cash flow analysis – the honest inventory

Before you start looking for new offers, you need to know exactly where you stand. Absolute clarity about your finances is the be-all and end-all and the foundation for everything that follows. Grab a piece of paper and pen or a spreadsheet and list all your loans and liabilities.

Write down these points for each individual loan:

- Lender: With which bank or company does the loan run?

- Current residual debt: How much money still has to be repaid today?

- Effective annual interest rate: What does the loan really cost you? The effective interest rate is crucial!

- Monthly installment: What amount do you transfer each month?

- Remaining term: How many months are left until the last installment?

This overview is pure gold. You can immediately see at a glance where the biggest money guzzlers are lurking and how much the new loan needs to be in order to pay everything off.

Step 2: Ask for the exact redemption amount

Armed with your completed list, now call your existing banks. Ask for the exact repayment amount on a specific date in the near future. This amount is often a little higher than the remaining debt on your list.

The reason for this? A possible early repayment penalty, which we have already discussed. Only if you know the exact amount that will be due for the full repayment can you make a clear calculation later and know how much you will really save in the end.

Step 3: Compare offers like a pro

Now comes the most exciting part: the hunt for the best offer. Make sure you use an independent online comparison calculator for this. This step is absolutely crucial in order to get the full savings potential out of your debt restructuring.

A good comparison is always non-binding and SCHUFA-neutral. This means that you can run through various scenarios without any risk. Your credit rating is not negatively affected by these inquiries.

When comparing, don’t just look at the interest rate alone. Also pay attention to flexible conditions, such as the option to make free unscheduled repayments. If you are looking through the various options, our loan comparison guide is a valuable aid to finding the real gems among the offers.

Step 4: The digital application – very straightforward

Have you found the perfect offer? Great! Nowadays, the application process is usually completely digital and really simple. You fill out everything online and upload the necessary documents directly.

As a rule, the bank needs the following documents from you:

- Proof of income: Your last payslips or the last tax assessment notice.

- Bank statements: So that the bank can track your income and expenditure.

- Existing loan agreements: The contracts of the loans you wish to redeem.

- Proof of identity: This is usually done quickly via Video-Ident on your cell phone or in the traditional way via Post-Ident.

The new bank will check your documents and give you the green light if the decision is positive – often within just a few hours.

Step 5: Lean back, relax and take a deep breath

Once your application has been approved, you can sit back and relax. You have done your part. The new bank will now take over the service for you and contact your old creditors directly.

It transfers the exact repayment amounts and redeems all the old loans for you. The result? From now on, you only pay a single, lower rate to a single contact person. You have successfully restructured your debt, tidied up your finances and noticeably reduced your monthly burden. Done

Conclusion: How to optimize your finances now

Our journey through the world of credit optimization has come to an end, and one thing has become clear: Debt restructuring is a real power tool, but only if you use it wisely. If tackled correctly, you can transform expensive old debts into a manageable and financially much easier future.

Think of it as a thorough spring clean for your finances. You muck out, reorganize and throw unnecessary ballast overboard. The biggest advantages are obvious: your monthly expenses are noticeably reduced, you regain an overview and finally take your financial planning back into your own hands.

Your path to financial relief

Debt restructuring doesn’t have to be a complicated feat of strength. See it as a conscious decision for a better financial situation. The key reasons for taking this path can be quickly summarized:

- Reduce interest costs: You swap an old, expensive loan for a new one with much better conditions. That’s money that stays in your pocket every month.

- Bundle loans: Instead of many small, confusing installments, you only have one. This creates order and predictability.

- Gain flexibility: Adjust the term and installment to suit your life today. Regardless of whether you want to be debt-free more quickly or simply reduce your monthly burden.

Of course, there are potential stumbling blocks such as the early repayment penalty. But as we have shown, in the vast majority of cases the savings from lower interest rates are significantly higher than these one-off costs. The key to success is an honest and transparent comparison of offers.

Don’t wait any longer for high interest rates to eat up your hard-earned money month after month. The best time to act is right now.

The first step is often the most important – and fortunately also the easiest. Get a clear overview of your current contracts. Use an independent loan calculator such as the one from Finanz-Foxto see your personal savings potential in black and white.

Start the comparison today and find the right partner to accompany you on your way to financial optimization. Take the first step towards a future with more financial freedom and noticeably less stress.

Still have questions? Here are the answers.

After all this information, you may still have one or two questions buzzing around in your head. This is perfectly understandable, as debt restructuring is an important financial decision. Here we clarify the most frequently asked questions that we come across again and again during our consultation, so that you have complete clarity at the end.

Will a debt restructuring affect my SCHUFA score?

I can reassure you here. Although the loan application itself can cause a minimal, temporary dip in your score in the short term, this is quickly forgotten. In the long term, smart debt restructuring almost always has a positive effect on your SCHUFA score. Why? Because you are demonstrating financial responsibility and foresight.

If you bundle several loans into one and then service it on time, you send the SCHUFA a signal: “I have my finances under control.” From their point of view, a well-managed loan is much better than a confusing pile of smaller debts. Your credit rating can improve noticeably and sustainably as a result.

A single, cleanly repaid loan sends a strong signal to future lenders: you actively manage your debts and are reliable. This is often worth its weight in gold for later financing projects.

Can I also refinance my dispokredit?

Yes, absolutely! To be honest, this is one of the smartest financial moves you can make. Paying off a constantly used overdraft facility is one of the most effective immediate measures you can take to get your finances back on track.

Think about it: The interest on overdraft facilities is often astronomically high, often in double figures. Every single day that your account is in the red costs you money. Swap this expensive overdraft facility for a fair installment loan, save interest from the very first moment and turn an expensive permanent debt into a manageable, predictable repayment.

How long does a debt restructuring actually take?

Fortunately, the days when you had to wait weeks for a decision from the bank are over. Thanks to modern, digital processes, everything is now pleasantly quick. It usually works like this:

- Inquiry & instant check: You make an inquiry online and often receive initial feedback after just a few minutes.

- Upload documents: Simply upload necessary documents such as salary statements digitally.

- Final check & payout: The bank carries out a final check and then initiates the repayment of your old loan.

All in all, it usually only takes between 3 and 7 working days from the first click to complete processing. This means that you benefit from better conditions within a very short time.

Are you ready to take control of your finances and benefit from lower interest rates? At Finanz-Fox you will not only find transparent comparison calculators, but also personal advisors who will accompany you on your way.