First things first: the widespread assumption that a loan during the probationary period is an impossibility is simply not true. Sure, it’s not quite as easy as having a permanent contract in your pocket, but it’s absolutely feasible. You just have to know what makes banks tick and prepare yourself accordingly. The trick is to refute the higher risk for the bank with solid arguments.

Is a loan during the probationary period really a realistic option?

For many, the thought of applying for a loan during the probationary period feels like trying to climb a mountain without any equipment. Fortunately, the reality is different, as countless such applications are approved every year. The myth of impossibility often stems from not fully understanding the bank’s perspective.

Why banks take such a close look at the probationary period

From a bank’s perspective, the probationary period is a phase of uncertainty. The Dismissal Protection Act does not usually apply in the first six months. This means that your boss can dismiss you with a short notice period of just two weeks without having to give reasons.

This is precisely the risk for the lender: if your salary suddenly disappears, the punctual repayment of the installments is at risk. Think of it like a test drive: The bank first wants to make sure that your financial “engine” – i.e. your income – is running smoothly and, above all, permanently before it invests money in you.

What the figures say in practice

Despite this hurdle, the data clearly shows that a loan during the trial period is feasible. An analysis of comparison portals showed, for example, that 731 customers were able to successfully take out a loan during their probationary period between January 2025 and December 2025 on Verivox alone.

The average effective interest rate for them was 8.13%, while borrowers without a trial period only paid an average of 6.39%. This interest premium of around 1.74 percentage points is, so to speak, the risk premium that the bank charges for the uncertainty.

So the most important thing is: banks don’t reject loans across the board. They assess the overall risk and charge a slightly higher interest rate. Their task is to make this risk as small as possible for the bank.

What really counts for banks

Your chances depend on a mix of different factors. The bank looks at your entire profile to assess your financial stability. In addition to the probationary period, these are above all

- Your net income: The higher your regular salary, the better. A solid income is the be-all and end-all.

- Your Schufa report: A spotless Schufa score without negative entries is an absolute must.

- Possible collateral: A second borrower, a guarantor or existing assets can be real door openers.

- Your industry and the employer: If you work in a crisis-proof industry for a well-known company, you immediately earn trust points.

This table summarizes the most important factors that determine whether a loan is approved during the probationary period and provides initial recommendations for action.

Checklist of your credit opportunities during the probationary period

| Factor | Importance for the bank | How to increase your chances |

|---|---|---|

| Net income | Decisive for the ability to pay installments. | Provide current proof of salary. The higher, the better. |

| Schufa score | The most important indicator of your payment behavior. | Check your score in advance and correct any incorrect entries. |

| Employer/industry | A stable environment reduces the risk of dismissal. | Emphasize the stability of your employer (e.g. public sector, large corporation). |

| Additional collateral | Minimize the default risk for the bank considerably. | Bring a second borrower or a solvent guarantor into play. |

| Existing relationship | Your bank knows your financial history. | First talk to your main bank, where you have been a customer for a long time. |

So with the right strategy and the right evidence, you can systematically dispel the bank’s concerns.

And if you’re in a particular hurry, an instant loan can be the solution. You can find out more about this in our detailed guide to comparing instant loans.

Why the probationary period is a risk for banks

To understand how you can still get a loan during the probationary period, we need to change our perspective for a moment and look at the whole thing from the bank’s point of view. For every bank, lending money is basically a bet on the future. They lend you money because they firmly believe that you will repay it reliably and on time.

This is where the probationary period comes into play and casts a considerable shadow over this calculation. Legally speaking, it is a phase of uncertainty. Your employment relationship can be terminated with a short notice period of just 14 days – and the employer doesn’t even have to give reasons. From a banking perspective, this is a clear, tangible default risk.

The core problem: the lack of income security

Your salary is the be-all and end-all of any loan. It is the engine that keeps the monthly installments running. If this engine suddenly breaks down, the whole financing system starts to falter.

Think of the bank as an architect planning a stable house. Your income is the foundation of this house. For the architect, a trial period is like a foundation of freshly poured concrete that is not yet completely dry. He will hesitate to build a complete house on it because he does not know whether it will withstand the pressure.

The credit check as a risk barometer

To assess this risk, banks carry out a detailed credit check. This is much more than just a quick look at your Schufa score. It’s a comprehensive analysis of your financial health and reliability, based on two pillars:

- External data: Information from credit agencies such as SCHUFA plays a particularly important role here. They show your previous payment history, whether you have already had loans or whether you have been in arrears with payments in the past.

- Internal scoring models: Each bank has its own, rather complex algorithms. These evaluate countless factors such as your age, your profession, the sector in which you work, your living situation and, of course, the ratio of income to expenditure.

The central question that the bank asks itself is: What is the statistical probability that this customer will pay his installments on time – despite the uncertain trial period?

A practical example: Max and his car loan

Let’s take a look at a concrete example. Max, 28, is an IT specialist and has just started a new, well-paid job at a large tech company. He urgently needs a car to get to work and applies for a loan of 15,000 euros. The problem: he is still in his probationary period.

At first glance, the red “probationary period” warning light comes on at the bank. But then the clerk takes a closer look:

- Professional stability: Max works in the IT industry, a sector in which skilled workers are desperately sought after. The risk of being unemployed for a long time after being made redundant is therefore minimal.

- Impeccable payment history: His Schufa score is spotless. He repaid his old student loan on time and never had any problems.

- Solid income: His salary is above average, the monthly installment would only make up a small part of his net income. So there is plenty of buffer.

- Well-known employer: His new employer is a stable, well-known company, which further strengthens the bank’s trust.

In this case, the positive aspects more than outweigh the risk of the trial period. The bank sees that Max’s overall financial profile is extremely strong. It will very likely give him the loan, perhaps with a slightly higher interest rate to cover the minimal residual risk. This example clearly shows that it always depends on the overall package.

Would you like to find out more about the basics of such financing? In our guide, we explain everything you need to know about installment loans.

How your credit rating becomes the key to financing

If the probationary period stands before you like a hurdle, your credit rating is the lever you can use to overcome it. Think of your credit rating as a kind of financial business card. It shows the bank at a glance how reliable you are with your finances and whether you are likely to repay a loan without any problems.

Banks take a closer look, especially when it comes to a loan during the probationary period. A spotless credit rating can almost completely offset the risk of a fresh employment relationship in the eyes of the lender. This proves that you have always been a reliable financial partner in the past.

The three pillars of your creditworthiness

Your financial business card stands on three crucial pillars. Only if all three are stable do you have the best chance of being accepted.

-

A flawless Schufa score: Your Schufa entry is your financial reputation. It documents how punctually you have paid bills and loan installments to date. Negative entries are an absolute knock-out criterion here.

-

A stable and sufficient income: The bank needs to see that your salary not only flows reliably into your account, but is also high enough to easily meet the monthly installment. A decisive factor for your creditworthiness is proof of income, which shows banks your financial stability.

-

A low level of debt: Do you already have other loans, leasing agreements or a heavily used overdraft facility? All of this reduces your financial leeway. A healthy upper limit is debt of less than 40% of your net income.

If you actively maintain these three areas, you will create a strong foundation for your loan application.

The role of attachable income

One term that comes up again and again in the lending process is attachable income. This is the part of your net income that remains after the statutory garnishment allowance has been deducted. This allowance is intended to secure your minimum subsistence level and is off-limits to creditors.

For a bank, this attachable portion is worth its weight in gold. It shows how much money would theoretically be available to pay off the debt in a worst-case scenario. The higher this amount is, the more secure the bank feels and the more money it is prepared to lend you.

Remember: your maximum loan installment must never be higher than your attachable income. This is an iron rule that almost all banks adhere to.

The amount of the possible loan therefore depends directly on your salary. If your net income is only just above the garnishment-free limit of 1,491.75 euros (as of 2024), you can usually only hope for a small loan. A higher income, on the other hand, creates significantly more leeway. With 2,000 euros net per month, for example, loans of up to 17,979 euros are theoretically conceivable, as there is simply a larger buffer here.

Practical steps to strengthen your credit rating

Your credit rating is not something you have to accept – you can actively shape it. With the following measures, you can improve your starting position for your loan application.

-

Request a Schufa self-disclosure: Order your free data copy from Schufa at least once a year. Go through every single entry meticulously and check whether everything is correct.

-

Have incorrect entries corrected: Have you discovered an error or an outdated negative entry? Contact the company that made the entry immediately and request its deletion in writing. Then provide proof of the correction to Schufa.

-

Be honest in your application: Never try to omit the probationary period from your loan application. Banks will check your employment contract anyway and the truth will inevitably come to light. Such dishonesty not only leads to immediate rejection, but can even be seen as attempted fraud.

Openness creates trust. If you state the trial period honestly and at the same time score points with an excellent credit rating and perhaps even additional collateral, you send a strong signal of reliability to the bank.

Would you like to delve deeper into the topic? Find out more about the importance and improvement of creditworthiness in our other articles.

Four ways to significantly improve your chances of getting a loan during the trial period

A loan rejection during the probationary period is initially a damper, but it is not a knockout blow. Look at it sportingly: it is a request from the bank to refine your application. With the right tactics, you can specifically refute the bank’s concerns and show that you are a reliable partner. Essentially, it’s about reducing the risk for the lender and building trust.

The following four strategies have proven themselves in practice and can open doors at the bank again. Each approach is different, but all aim to enhance your financial profile for the loan decision.

1. get a co-applicant on board

This is probably the strongest lever you have: Don’t apply for the loan alone. If a second borrower – often the partner with a permanent, permanent job – also signs, this changes the rules of the game for the bank from the ground up.

Why? The co-applicant is fully liable for the loan with you. Suddenly the bank has two incomes and two debtors to fall back on in an emergency. This shared risk not only catapults the chances of approval upwards, but often also leads to noticeably better interest rates. The default risk for the bank is simply drastically reduced.

A typical case: Lena needs a loan for her new kitchen during her trial period. She is turned down on her own. But when she submits the application together with her husband, who has been in the job for five years, she is approved immediately – and with a 1.5% lower interest rate.

2. find a guarantor to back you up

A guarantor is another excellent way of providing the bank with the necessary security. Unlike a co-applicant, the guarantor does not become the borrower themselves. Instead, they are your financial “safety net”. They are contractually obliged to cover the installments should you no longer be able to.

But one thing is also clear: a guarantor must be absolutely convincing financially. He or she needs a spotless credit rating and a stable, high income, because the bank will scrutinize him or her just as thoroughly as it will you. A guarantor is a huge responsibility, which is why only close family members or best friends usually take on this role.

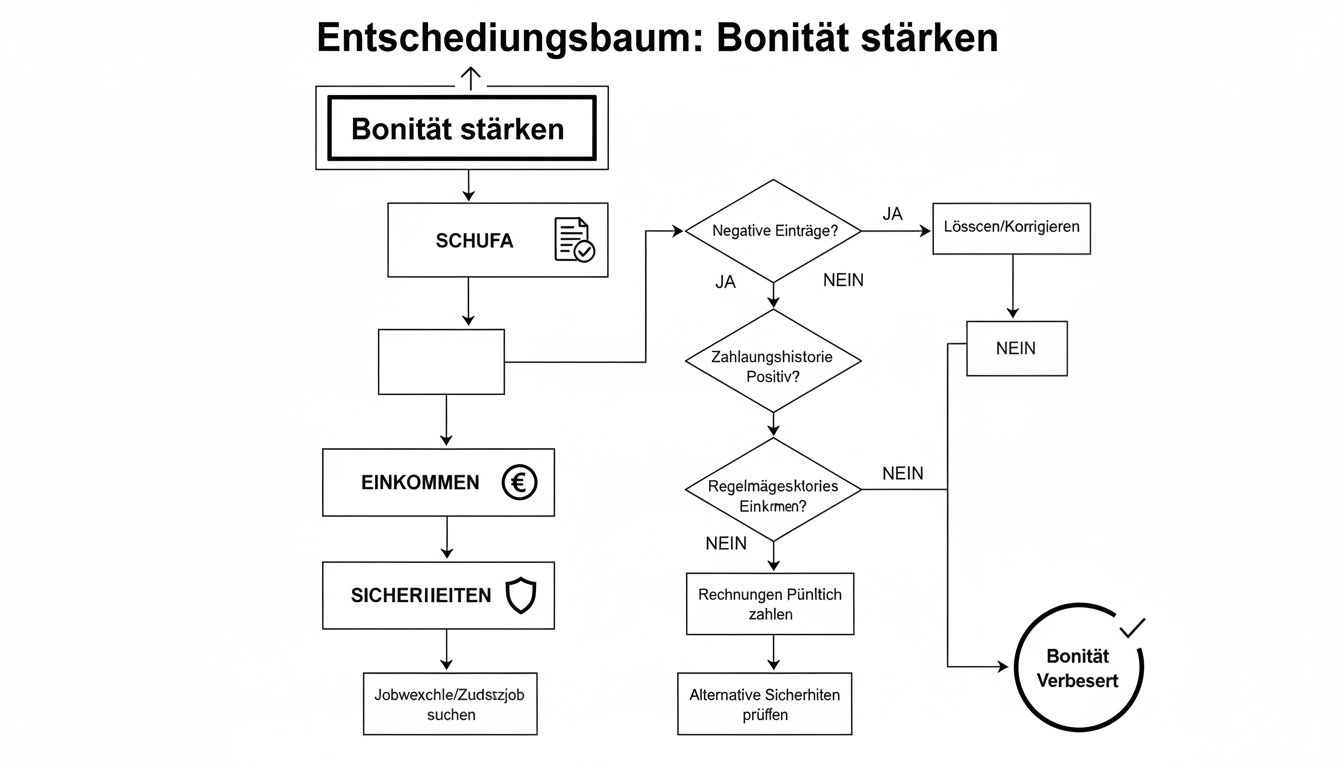

This decision tree shows how the various pieces of the puzzle fit together to strengthen your credit rating and therefore your chances of obtaining a loan.

The chart clearly shows that, in addition to a clean credit score and a solid income, additional collateral is often the decisive factor for success.

3. bring additional securities into play

Do you have tangible assets? Perfect! These can serve as valuable collateral and provide the bank with exactly the tangible countervalue it is looking for to minimize risk.

What banks typically accept:

- Transferring ownership of a car by way of security: If you own a debt-free vehicle, you can deposit the vehicle registration certificate (registration certificate part II) with the bank as collateral. The car still belongs to you, but serves as collateral for the bank.

- Life or pension insurance policies: Capital-forming policies with a corresponding surrender value are also an attractive form of security for banks.

- Securities accounts or savings deposits: These can also be pledged to offset the credit default risk for the bank.

4. readjust the loan amount and term

Sometimes the solution lies in the obvious. A loan amount that is too high or a term that is too short can lead to a monthly installment that the bank simply finds too tricky during the trial period. There are two simple adjustments you can make here:

- Smaller loan amount: think again: do you really need the full amount? A reduction of 10-20% is often enough to bring you back into the green zone of the bank’s internal debit limits.

- Longer term: By stretching the repayment over a longer period, the monthly installment is noticeably reduced. A lower installment means less pressure on your budget and therefore less risk for the bank – and this increases your chances of getting a loan during the trial period enormously.

Each of these strategies has its own strengths and requirements. The following table will help you to find the right path for you.

Comparison of strategies to increase opportunities

This table compares the strategies presented in terms of their effectiveness, prerequisites and potential disadvantages.

| Strategy | Impact on the bank | Prerequisites | Possible disadvantages |

|---|---|---|---|

| Co-applicant | Very high (double income, double liability) | Creditworthy partner with fixed income | Partner is fully liable; decision must be made jointly |

| Bürge | High (strong safety net) | Guarantor with a strong credit rating who is prepared to assume responsibility | High moral and legal responsibility for the guarantor; often only possible in the closest circle |

| Collateral | Medium to high (tangible equivalent value) | Existing, unencumbered assets (car, deposit, insurance) | Asset is tied up and can be realized by the bank in an emergency |

| Adjustment total/term | Medium (lower monthly charge) | Flexibility in the loan amount and willingness for a longer term | Total costs of the loan increase due to longer term; may not be sufficient for the financing purpose |

As you can see, there is no one perfect solution. The best strategy always depends on your personal situation – whether you have a strong partner at your side, have assets or are flexible with the loan amount. A combination is often the smartest way to achieve your goal.

If the bank says “no”: these paths still lead to your goal

A rejection for a loan application during the trial period? At first it feels like a slammed door, but in reality it’s just a small detour. It doesn’t mean that your finances aren’t in order. It just means that the bank sees your employment as too uncertain a piece of the puzzle in the overall assessment.

But don’t worry, the game is far from over. There are a whole range of tried and tested alternatives that you can use to bridge financial bottlenecks or make an important purchase. Think of these options as clever interim solutions – as a bridge until your employment contract is terminated. Each has its own rules and costs. It is important that you look carefully to find the solution that is fair and really suits your situation.

The overdraft facility: quick help with your account

Almost every current account in this country has it: the overdraft facility, which we all just call the “overdraft facility”. It is the unbeaten champion when it comes to speed, because it is already there, approved and just waiting to be used. No application, no waiting time.

Its greatest strength is its absolute flexibility. You simply overdraw your account up to the agreed limit and only pay interest on the amount you actually use. As soon as the next salary arrives, the deficit is balanced out all by itself.

But beware, there is a cost trap lurking here: this convenience comes at a price. Overdraft rates are notoriously high, often in the double-digit range. An overdraft facility is therefore only an emergency solution for very short-term bottlenecks – think of a few days or a week to replace a broken washing machine until your wages arrive.

The mini loan: small sums, quick approval

Do you only need a few hundred euros, perhaps up to €1,500? Then a mini loan could be just the thing. These loans are the sprinters among loans, so to speak: designed for short distances with terms of often just 30 to 90 days.

The advantages are obvious:

- Lightning-fast decision: The test usually runs fully automatically. You often know the answer after just a few hours.

- Lower hurdles: Because small amounts and short terms are involved, the creditworthiness requirements are usually more relaxed than for a classic installment loan.

- Everything online: From application to payout, you can complete the entire process from the comfort of your own home.

This type of loan is perfect for bridging the gap until the end of your probationary period. In our guide to mini-loans as flexible financial helpers, we explain exactly how this works and what you should look out for.

The personal loan: help from family or friends

Sometimes the best bank is your own family or circle of friends. A loan from people who trust you is often unbeatably cheap – sometimes interest is even waived completely. This can be a huge relief, but also carries the risk of straining the relationship if something goes wrong.

To ensure that money does not suddenly turn into a dispute, approach the matter professionally. Make sure you draw up a written contract. This may sound excessive, but it protects both sides. The following points should be included:

- The exact loan amount

- The interest rate (even if it is 0%, this should be recorded)

- A clear repayment plan with installment amounts and due dates

- A regulation on what happens if you are unable to pay an installment on time

Such a contract creates clear conditions and ensures that a friendly service does not become a permanent nuisance.

The pledge loan: your valuable item as collateral

Do you have valuable jewelry, an expensive watch or high-quality electronics lying around unused? Then a pawn loan could be an unbureaucratic and lightning-fast solution. The best thing about it is that your personal credit rating or the fact that you need a loan during your probationary period doesn’t matter at all.

The principle has been the same for centuries: you deposit a valuable item in the pawnshop and receive immediate cash in return. The amount of the loan is based on the value of your pawn. As soon as you repay the money plus interest and fees within the agreed period, you get your item back intact. If repayment is not successful, the item will be auctioned off – but you will have no further debts.

How to find the right loan with Finanz-Fox

Theory is all well and good, but now it’s time to get specific: how do you actually get the right loan? This is where we at Finanz-Fox take you by the hand. We transform the often confusing search into a clear, comprehensible path. Our aim is not just to provide you with knowledge. We want to actively support you in finding the best financing for your personal situation – especially if you need a loan during your probationary period.

The biggest trump card up our sleeve is the Schufa-neutral loan comparison. What does that mean for you? It’s simple: with a single request, you can have the conditions of over 20 different banks checked without even a scratch on your Schufa score.

Think of it like relaxed window shopping. You look at everything, compare the offers at your leisure and only make a purchase when you have found the perfect item. Every inquiry you make with us is purely a conditional inquiry – it leaves no trace in your Schufa file.

Your personal financial compass

Our loan calculator is more than just a slide rule; it is your personal financial compass. Here you can play through various scenarios to your heart’s content. What happens if I extend the term by a year? How will a smaller loan amount affect my monthly installment?

In this way, you can easily get a feel for which combination of loan amount, term and installment really fits into your monthly budget. You can see what is realistic and make a well-considered decision long before you submit a binding application. This step is worth its weight in gold, because a well-prepared application has a much higher chance of success.

Our promise: We will find you exactly the bank whose lending guidelines best suit your individual situation. In this way, we maximize your chances of a quick approval at fair interest rates.

From click to loan – digital and yet personal

Once you have discovered your desired offer, everything continues at lightning speed. The application process is completely digital. No annoying paperwork, no waiting for the letter carrier. You simply upload the necessary documents online and identify yourself via video call. This not only saves an enormous amount of time, but also speeds up the bank’s decision considerably.

But the real added value of Finanz-Fox is the personal support. With us, you are not an anonymous number in the system. Our loan specialists are with you every step of the way. They take a trained look at your application, provide valuable tips for optimization and help you to present your financial situation in the best possible light. It is precisely this human factor that often makes the small but subtle difference between an approval and a rejection.

We pave the way for you so that your loan does not remain an unfulfilled wish during the trial period.

If you want to delve even deeper into the world of loan comparisons, we recommend our guide on how to easily find the best deal with our loan comparison.

What else you need to know: Answers to the most frequently asked questions

Anyone dealing with the topic of credit during the probationary period often has very specific questions burning under their nails. You come across a lot of information, but the really important, practical answers are sometimes missing. This is exactly where we come in and clarify the typical uncertainties – briefly, comprehensibly and without technical jargon.

What papers does the bank want to see from me?

Expect the bank to take a closer look at you. This is completely normal, as they are not yet familiar with your new professional situation. Your task is to present a clear and trustworthy picture of your finances with the right documents.

It is best to have the following to hand:

- Your employment contract, complete and legible. It must clearly state the probationary period and, of course, your salary.

- The last one to three salary slips from your new job. If you don’t have any yet, that’s no problem; the employment contract is then all the more important.

- The bank statements for the last three months. This allows the bank to see that your salary is actually being received regularly.

- A copy of your identity card or passport for identification purposes.

- If available: Proof of additional income or collateral. This can be anything from rental income to the title of your car.

Does a credit comparison ruin my credit rating?

I can absolutely reassure you: No, not at all. When you use a comparison portal such as Finanz-Fox to obtain various offers, something very important happens in the background: a “request for loan conditions” is simply made.

This is the window shopping of the credit world, so to speak. You can view as many offers as you like, completely risk-free. These requests are 100% Schufa-neutral, other banks don’t even see them. Only when the nail is on the head, i.e. you decide on an offer and sign the contract, does the bank report a credit-relevant “credit inquiry” to Schufa.

Isn’t it smarter to simply wait until after the probationary period?

That is the crucial question, and the answer depends entirely on you and your urgency. If it’s not urgent and you can postpone the purchase for a few more months, waiting is often the smarter option.

As soon as you are taken on permanently, you are considered a much safer bank for the bank. This not only improves your chances of being approved, but often also significantly reduces interest rates.

However, if you need the car to get to your new job or the washing machine has broken down, then applying for a loan during the trial period is absolutely feasible. With the right preparation and the right collateral, it’s not rocket science.

Are there banks that specialize in loans during the probationary period?

There is no bank that advertises this directly. That would be far too small a niche. But practical experience clearly shows that modern direct and online banks are often much more flexible and open-minded than the long-established house bank around the corner. They often assess risk differently, based more on data and less on rigid rules.

This is exactly where a good comparison portal comes into its own. It knows the “personality” and acceptance criteria of the various banks and can therefore filter out the providers for you where an application during the trial period has the best chance of success. This saves you time, nerves and unnecessary rejections.

Do you now feel better informed and want to take the next step? The experts at Finanz-Fox will help you find the best solution for your individual situation. Start your non-binding and Schufa-neutral loan comparison now at https://www.finanz-fox.de.