At first glance, the formula for calculating a loan often looks like a real monster. But don’t worry, there’s a very simple logic behind it that revolves around just three crucial factors: the amount you borrow, the bank’s interest rate and the term over which you repay everything.

These three components ultimately determine how high your monthly installment will be and how much the fun will cost you in the end.

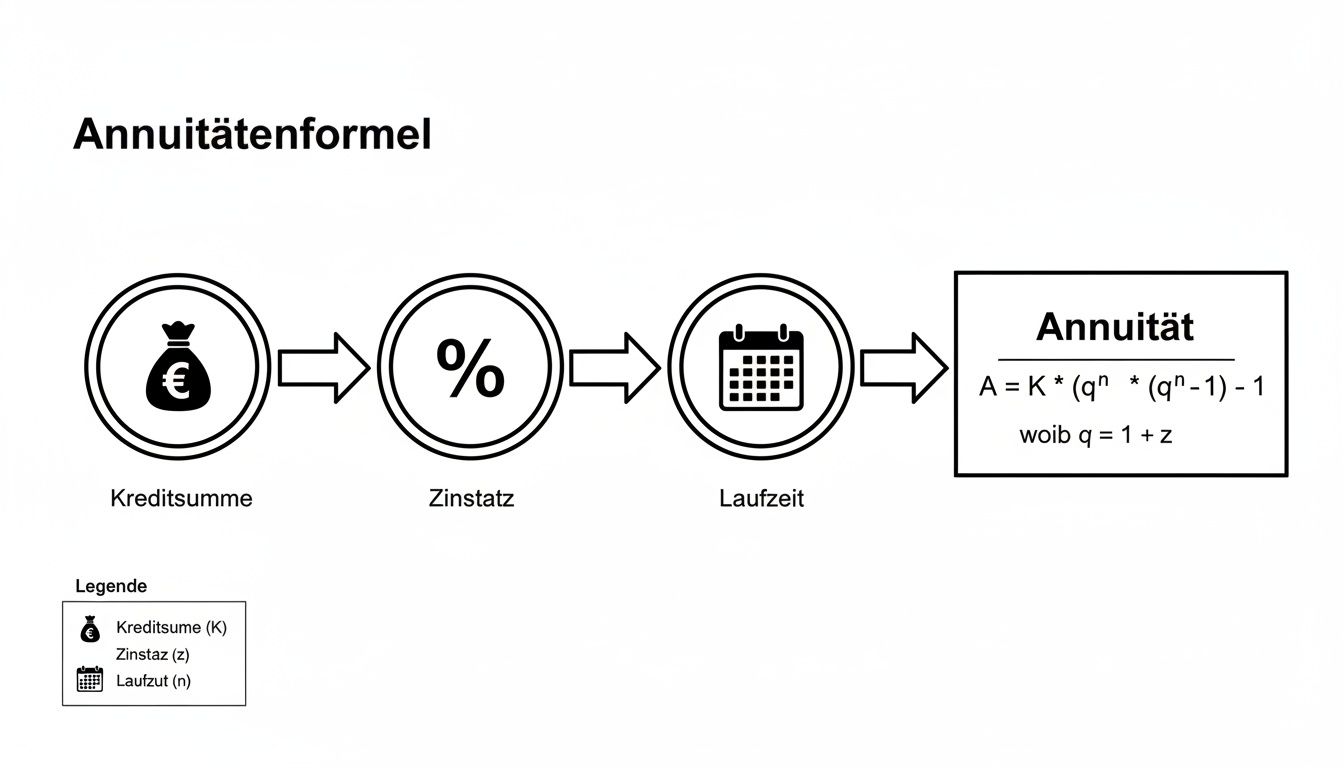

How the credit calculation really works

Many people shy away from the mathematics behind a loan agreement. But the principle behind it is easier to understand than you might think. Before we dive straight into the bare formula, it is much more important to get a feel for the connections first.

Think of the three factors like the sliders on a mixing console: If you turn one of them, the entire sound pattern – i.e. your monthly load – changes immediately.

The eternal balancing act: term and loan amount

Of course, a longer term initially means a lower monthly installment. This provides short-term breathing space in the budget and is incredibly tempting. The catch, however, is that you end up paying significantly more interest and the loan becomes more expensive as a result. This is logical, as the bank is lending you the money for a longer period of time.

Many people fall into the trap of thinking that the lowest possible rate is always the best deal. From my experience, I can say that it is often wiser to choose a shorter term. Even if the monthly charge is then a little on the tighter side, you often save thousands of euros in interest over the total term.

To make the whole thing a little more tangible, let’s take a look at some concrete figures. The following table shows how the monthly installment changes at an interest rate of 5%, depending on how much money you borrow and how long you pay it back.

Exemplary monthly installments at 5 % effective annual interest rate

This table shows how the monthly loan installment (annuity) changes depending on the loan amount and the selected term. This serves as an initial guide.

| Loan amount | Term 36 months | Term 60 months | Term 84 months |

|---|---|---|---|

| 10.000 € | 299,71 € | 188,71 € | 141,35 € |

| 20.000 € | 599,42 € | 377,42 € | 282,69 € |

| 30.000 € | 899,13 € | 566,14 € | 424,04 € |

The figures speak for themselves: doubling the term does not halve the installment. The compound interest effect over the longer term takes full effect here.

If you would like to delve deeper into the subject, you will find many more articles on the topic of financing in our guide section. With this basic knowledge, you are now well equipped to crack the formula behind it in the next step.

How to calculate your monthly loan installment – the annuity formula in plain language

Now it’s time to get down to business. The linchpin of every installment loan is the monthly installment, the so-called annuity. This installment remains the same over the entire term and is the figure that must be included in your budget at the end of the month. It is made up of an interest portion and a repayment portion.

At first glance, the formula behind it may look a little intimidating, but don’t worry. We’ll take it apart together now.

The annuity formula you use to calculate a loan is as follows:

Rate (R) = K * [ (i * (1 + i)^n) / ((1 + i)^n – 1) ]

This is basically the mathematical heart of every installment loan. The formula ensures that your monthly repayments remain constant, although the ratio of interest to repayment shifts with each individual payment. At the beginning you pay more interest, at the end almost only repayments.

Filling the placeholders of the formula with life

To use the formula for your personal loan, we just need to feed the variables with the correct values. This is easier than you might think.

- K stands for the loan amount – i.e. the amount you are borrowing.

- i is the monthly interest rate. And this is exactly where the most common source of error lurks!

- n is the number of installments, i.e. the term in months.

The crux of the matter is the interest rate i. Banks always state the interest rate as an annual value. However, we first have to convert this for our monthly installment.

A typical stumbling block: inserting the annual interest rate directly into the formula. Make it easy for yourself: divide the nominal annual interest rate by 12. For an annual interest rate of 5% (i.e. 0.05), calculate: 0.05 / 12 = 0.004167. This small value is your i.

A real-life example: a car loan for 20,000 euros

Let’s imagine you have found your dream car and need to finance it for €20,000. The bank makes you an offer with an APR of 4.5% and a term of 60 months (i.e. 5 years).

So we have everything we need:

- K: 20.000 €

- n: 60 months

- i: 0.045 / 12 = 0.00375 (our monthly interest rate)

Now we simply insert these figures into our formula:

Rate = 20,000 * [ (0.00375 * (1 + 0.00375)^60) / ((1 + 0.00375)^60 – 1) ]

Type it into the calculator once, and we get the result: a monthly installment of €372.89. With this specific sum, you can now realistically plan your monthly budget and see if everything fits.

By the way, if you ever need to bridge a smaller sum, the principle remains the same. You can find out more in our guide to mini-credits and small loans.

Debit interest or effective annual interest rate – what you need to look out for

One last, but crucial, practical tip: always compare offers on the basis of the effective annual interest rate. Don’t let yourself be blinded by the often smaller target interest rate (or nominal interest rate). This only reflects the pure interest costs for the borrowed capital.

The APR is the only honest figure. It includes all additional costs and fees that are incurred for the loan, such as processing fees. Only this figure shows you what the loan will really cost you in the end and makes different offers fairly comparable. A supposedly favorable offer with a low borrowing rate can quickly become a cost trap due to high fees.

The interplay of interest and repayment over time

The monthly installment that we have just calculated is a constant – it remains the same over the entire term. But what fundamentally changes with every single payment is the internal breakdown of this installment. And understanding this principle is the key to really understanding how to reduce your debt bit by bit.

The dynamics behind this are actually quite logical: at the beginning, your remaining debt is the highest, so the largest part of your installment goes to the bank as interest. Over time, however, the balance shifts more and more in your favor.

The invisible scale in your loan installment

Think of your installment as a scale. On one side is the interest portion, on the other the repayment portion. At the beginning of the term, the interest side pushes down heavily. But with each payment, you nibble away a small piece of your loan amount – the remaining debt.

A lower residual debt naturally means that less interest will be due next month. However, as your installment remains stubbornly high, the proportion that remains for the actual repayment (the redemption) increases automatically. This is an effect that even accelerates over time.

The following chart summarizes the components that are included in the calculation of your rate and thus create the basis for the division into interest and repayment.

As you can clearly see, the loan amount, interest rate and term are the decisive factors for your monthly annuity, but their composition is constantly changing.

How to crack the interest and repayment portion for each installment

Okay, but how do you calculate the exact interest and repayment portion for a specific installment? Don’t worry, there is a simple formula for this too. Let’s stick with our example of the car loan(€20,000, 4.5% annual interest, €372.89 installment).

First the interest portion:

The interest portion for a month is always calculated by multiplying the current residual debt by the monthly interest rate (i).

- The formula is:

Zinsanteil = Restschuld * i - For the very first installment, the remaining debt is of course still the full loan amount.

- The bill:

20.000 € * 0,00375 = 75,00 €

And then the repayment portion:

This is now quite simple – the repayment portion is simply the remainder of your installment.

- The formula:

Tilgungsanteil = Monatliche Rate - Zinsanteil - The bill:

372,89 € - 75,00 € = 297,89 €

In plain language, this means that €75.00 of your first payment of €372.89 goes to the bank as interest. Only the remaining € 297.89 will actually reduce your debt.

Experience the progress of the repayment plan live

The world already looks a little better with the second installment. Your new remaining debt is now only 20.000 € - 297,89 € = 19.702,11 €. Let’s do the math again:

- New interest component:

19.702,11 € * 0,00375 = 73,88 € - New redemption portion:

372,89 € - 73,88 € = 299,01 €

Can you see that? The interest portion has already fallen slightly, while your repayment portion has risen. This shift continues month after month. Knowing this principle is worth its weight in gold, especially when it comes to large lumps such as a mortgage. Find out more about why a precise comparison always pays off when it comes to real estate financing.

With every payment you make, you regain a little bit of financial freedom. Progress may seem slow at first, but knowing how your repayments are steadily increasing is a huge motivation on the road to debt freedom.

This principle is at the heart of every repayment plan and shows you with complete transparency where your money is actually going each month.

A typical installment loan calculated in practice

Gray theory is one thing, but what does it all look like in real life? Let’s get down to it. Imagine your old kitchen has finally had its day and you need a new one. After a bit of research and planning, you realize that you need a loan of €10,000.

A quick trip to the comparison portal spits out a pretty decent offer: a classic installment loan, 7.99% APR, spread over 60 months, i.e. five years. With these figures in hand, we can now feed our formulas and see what we really end up with. It’s not just about the monthly installment, but about the true cost of the whole thing.

Step by step to the monthly charge

First of all, we need to break down the annual interest rate to the month. This is done quickly: 0,0799 / 12 = 0,0066583. We enter this value together with the other data into our annuity formula. The result? A monthly installment of €202.76. This is the amount that will be permanently deducted from your account over the next five years.

But this figure alone is only half the battle. It gets really exciting when we calculate what the new kitchen will really cost you in the end. To do this, we take the monthly installment and multiply it by the term: 202,76 € * 60 = 12.165,60 €.

This is the total amount that you repay to the bank over the full five years.

The decisive “aha” moment comes when you subtract the loan amount from the total amount. Your interest costs amount to €2,165.60. That’s the price you pay for the money you borrowed – more than a fifth of the original loan amount.

This simple calculation makes it painfully clear why you should never be blinded by a seemingly small monthly payment. The total cost is the figure that really counts in the end.

Keeping an eye on the true costs

This calculation shows how important it is to understand the total cost of financing before you sign anything. The same principle also applies on a larger scale, of course, for example if you are financing private real estate and using our formulas to calculate the long-term burden.

In practice, the actual costs can of course vary slightly depending on the provider. Experts therefore advise you to always check the final total amount. A detailed analysis shows, for example, that the same conditions(€10,000, 60 months, 7.99% effective interest rate) can result in total costs of €2,083.17. You can see the exact breakdown behind this in this sample calculation on haushaltsfinanzen.de.

This little excursion into practice transforms an abstract formula into a powerful tool. One that will help you uncover the true cost of any financing and make a smart decision. If you want to delve deeper into the world of loans, you’ll find everything you need to know about installment loans in our guide.

What really counts besides the formula when taking out a loan

Mastering the formulas for calculating credit is one side of the coin. That is the tool of the trade. But making a really good credit decision? You can’t make it with a calculator alone. From my experience in countless consultations, I know that the “soft” factors are often just as decisive as the bare interest rate.

So before you even think about making an offer, you need to carry out a ruthlessly honest cash flow analysis. It’s not just about what’s possible on paper today. It’s about building in a buffer for the uncertainties of life.

The golden rule of financial sustainability

There is a tried-and-tested rule of thumb that helps you to realistically estimate your own repayment limit. In Germany, experts advise that monthly loan installments should never exceed 35 to 40 percent of net income.

This rule isn’t a rigid law, but it’s a damn good buffer to keep you from floundering at the first unexpected car repair or hefty utility bill.

To determine your personal margin, simply do the math: Take your monthly net income and deduct everything that is fixed – rent, utilities, insurance, savings rates and also the budget for leisure and hobbies. The amount that remains at the end is your disposable income. And you should then budget a maximum of 40% of this for the loan installment.

The best loan is not the one with the lowest interest rate, but the one that gives you room to breathe even in turbulent times. Always plan conservatively and not on the edge.

Flexibility in the contract is worth its weight in gold

Life rarely sticks to five-year plans. A change of job, a new addition to the family or an extended illness can completely redraw the financial map. This is precisely why flexible contract terms are so incredibly valuable.

Therefore, pay very close attention to clauses in loan offers that give you leeway:

- Special repayments: The ability to repay an additional amount once a year or more often without penalty interest is a powerful tool. Each unscheduled repayment shortens the term and noticeably reduces your overall interest costs.

- Installment breaks: Some banks offer to suspend one or two installments per year if things get really tight financially. This safety net can make all the difference in an emergency.

These options sometimes cost a tiny interest surcharge, but the security and flexibility they give you are almost always worth the price. If you’re unsure about the pitfalls that can lurk in the application process, you’ll find even more practical help in our article Valuable tips and tricks for a successful loan application.

Compare offers – wisely and independently

The biggest and most expensive mistake that many people make out of sheer convenience: they accept the first offer from their own bank. Although this is easy, it is rarely the best or even the cheapest option. Today, an independent comparison is more important than ever.

Use comparison calculators such as our Finance Fox to get a real overview of the market. There is often a difference of several percentage points between the offer from your bank and the best online deal – which can quickly add up to thousands of euros over the years. Metaplanet, which has secured a loan for Bitcoin acquisitions, is a modern example of how flexibly financing is handled these days.

In the end, only one thing counts: finding financing that is not only mathematically correct, but also perfectly suited to you and your life situation.

Still have questions? The most important answers at a glance

Finally, I would like to address a few questions that I encounter again and again in practice when it comes to calculating loans. Think of it as a little cheat sheet that clears up any last ambiguities and gives you certainty for your decision.

Why is the APR so important?

Many people ask me why they can’t simply compare offers based on the borrowing rate. The answer is simple, but extremely important: the borrowing rate is only half the truth. It only quantifies the “rent” for the borrowed money, i.e. the pure interest costs.

What he completely ignores, however, are all the other costs that a bank could charge for the loan – for example, processing or account management fees.

And that is precisely why the APR exists. It is the only honest benchmark. The law stipulates that it must include all mandatory costs. This is the only way to see at a glance what the loan will really cost you. An offer with a temptingly low borrowing rate can quickly turn out to be an expensive trap due to high additional costs.

Does this formula also apply to construction financing?

In principle, yes. The mathematical basis, i.e. the annuity formula, is exactly the same for a construction loan. A construction loan is basically nothing more than a huge annuity loan. In practice, however, things quickly become more complicated.

A few additional factors usually come into play with construction financing:

- Long fixed interest periods: We are often talking about 10, 15 or even 20 years. After that, there is a residual debt for which you need follow-up financing – at the then applicable interest rates.

- Variable repayment: Many contracts allow you to change the repayment rate during the term, which of course affects the installment.

- KfW funding: KfW development loans, which have their own rules and conditions, are often included.

Because of this complexity, it almost always makes more sense to use a specialized mortgage calculator directly when taking out a mortgage.

What are the real benefits of unscheduled repayments?

It’s simple: an unscheduled repayment is your sharpest weapon in the fight against interest costs. Every euro you pay out of turn goes 100% towards repaying your remaining debt.

See a special repayment as a direct blow against the mountain of debt. You bypass the interest component completely and repay the capital directly. This is the absolute turbo to become debt-free faster and save interest.

This direct attack on capital has two massive advantages:

- Shorter term: Your loan is paid off noticeably faster.

- Lower interest costs: Because interest is always calculated on the remaining debt, you save money with every unscheduled repayment. This adds up over the years.

Don’t underestimate this! Even small but regular extra payments can mean savings of several thousand euros over the term of the loan. So when you sign the contract, make sure that special repayments are possible free of charge.

Have you understood the formulas, but still need the right offer? The free and non-binding loan comparison from Finanz-Fox does the work for you and finds the best conditions for your project. Simply start your request – the next step towards your financial freedom is just a few clicks away.