If you’re thinking about changing your car insurance, you should keep one thing in mind above all: the notice period. This is usually November 30. It is just as important not to cancel the old contract until you are certain that the new one has been approved. And please don’t just look at the price – the benefits have to be right, otherwise there could be nasty surprises or an annoying insurance gap in the event of a claim.

Your roadmap to a smart insurance change

A sudden price increase, the desire for better services or simply the prospect of saving a few hundred euros every year – there are many reasons for switching. But how do you go about it without falling into one of the typical traps? Don’t worry, this guide is your personal roadmap. We’ll go through everything step by step so that you’re safe and well informed right from the start.

Think of this section as your personal quick start. We lay the foundations and answer the most pressing questions before diving deeper into the subject matter:

- The perfect time: when is the best time to get active?

- The most important deadlines: Which dates do you need to mark in red in your calendar?

- The special right of termination: how can you make clever use of a premium increase?

- Necessary documents: What papers should you have ready to ensure that everything runs smoothly?

Why a switch can be worth its weight in gold right now

The insurance market is constantly changing. If you don’t put out feelers and make comparisons from time to time, you’re leaving money on the street. You may already be familiar with the principle from other areas: Similar to electricity or gas, a targeted change of provider can save you a tidy sum. If you have already gained experience with this, you will know how simple and rewarding it can be. The procedure is often surprisingly similar. If you’re interested in the topic, you can find valuable tips on how to switch gas supplier smoothly and without headaches in our guide.

Remember one thing: loyalty to the old insurer is rarely rewarded. New customers almost always get the more attractive offers, while existing customers often tacitly pay more.

The most important dates for your insurance change at a glance

Timing is everything when changing your car insurance. The following table gives you a quick overview of the key dates and deadlines that you should definitely have on your radar. This way you won’t miss any important deadlines.

| Reason for the change | Deadline or cut-off date | What you need to do |

|---|---|---|

| Regular termination | November 30 | Notice of termination must be received by the old insurer by this date (at the end of the contract on December 31). |

| Special termination (premium increase) | 1 month after receipt of the invoice | As soon as you receive notification of the increase, the period for your extraordinary termination begins. |

| Special termination (vehicle change) | Immediately upon deregistration | The contract ends automatically when the old vehicle is deregistered. |

| Special termination (case of damage) | 1 month after conclusion of the hearing | After a claim has been settled, both you and the insurer can cancel the policy. |

If you keep an eye on this data, you are always on the safe side and can react flexibly to changes.

A brief look at the market

In recent years, the mood among German drivers to change their car insurance has calmed down somewhat. A study by Sirius Campus shows that the number of policy changes has fallen from around 3.2 million to around 1.7 million. One reason for this could be more moderate premium adjustments. Nevertheless, the market remains highly competitive.

The concentration on the big players remains high: the top 5 insurers have snapped up 48% of all new contracts. These figures clearly show that although fewer people are switching, comparison is more worthwhile than ever. Portals often show potential savings of up to 30 percent. If you want to delve deeper into the figures, you can find an exciting analysis of which car insurers dominated the switching season on Versicherungsjournal.de.

This guide will give you the tools you need to take advantage of this competition and make the best decision for your car and your wallet.

Targeted use of notice periods and special termination rights

Getting rid of your old policy is the first and most important step on the way to a cheaper rate. Many drivers only have the one famous deadline in mind. But there are so many more ways to end a contract that no longer fits. If you ask yourself what you need to consider when changing car insurance, then knowing your own termination options is at the top of the list.

Of course, most contracts end on December 31 and have a notice period of one month. This explains the annual hustle and bustle around November 30. Your written notice of termination must reach the insurer by this date. Please note: The postmark is not sufficient!

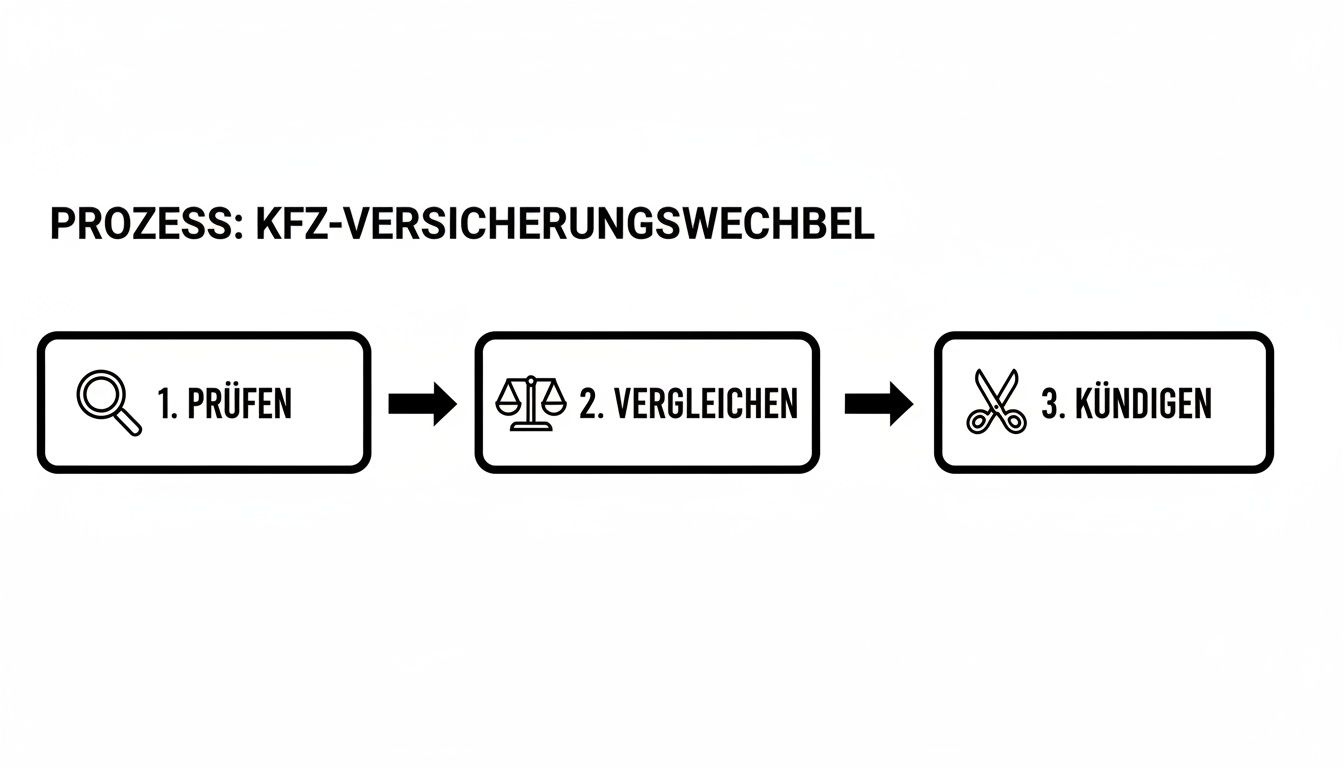

This process is actually quite simple to structure if you know how.

As you can see here, a successful switch always starts with an honest review of the old contract. Then comes the careful comparison – and only at the very end the termination.

The special right of termination: the joker up your sleeve

Much more exciting than the normal termination at the end of the year are the situations that give you a special right of termination. This allows you to simply override the rigid deadlines and gain unexpected freedom. In practice, there are three classic cases in particular:

- Premium increase: Your insurer is cutting prices without improving benefits? That’s your keyword! Even a small adjustment to the type or regional class can trigger this right. As soon as you receive the new invoice, you usually have one month to give extraordinary notice of termination.

- Claims: After a claim has been settled – regardless of whether it is positive or negative for you – both parties can terminate the contract. Here too, there is usually a period of one month after the claim has been settled. This is particularly worth considering if you were anything but satisfied with the settlement.

- Vehicle change: The simplest case. You sell your old car and deregister it, which automatically terminates the contract. When you buy a new car, you then have complete freedom in your choice of insurer.

Imagine this: You receive your new premium invoice in October and can’t believe your eyes – the price has gone up, even though you’ve made it through the year without an accident. Instead of waiting until November 30, you can exercise your special right of termination immediately.

This right is a real asset for us consumers. We have summarized further important details for you in our overview of current notice periods so that you don’t miss out.

Termination – but the right way

Whether you give notice of termination in due time at the end of the year or for cause, one thing remains the same: it must be in writing. A simple letter is sufficient, but it should contain the following points to ensure that nothing goes wrong:

- Your full name and address

- The number of your insurance policy

- The registration number of the vehicle

- The reason (e.g. “Termination with notice to expiry of contract” or “Special termination due to premium increase”)

- The current date and your handwritten signature

To be on the safe side, especially in the case of extraordinary termination, it is worth taking a look at tried and tested templates such as this sample for extraordinary termination. My tip from experience: Always send the notice of termination by registered letter with acknowledgement of receipt. It may cost a few euros more, but you will have solid proof that everything arrived on time. This way, nothing stands in the way of a smooth transition.

Compare tariffs and services correctly

Hand on heart: If you only look for the cheapest price, you often fall into the performance trap. The small print is tricky and can be really expensive in the event of a claim.

The figures speak for themselves: according to the Federal Statistical Office, premiums have recently risen by 10.9 percent, and for fully comprehensive insurance the increase was a hefty 17 percent. Let’s take a model family with a VW Golf – here the annual premiums for top rates vary between 400 and 1,136 euros. This shows the huge savings potential of the right comparison.

The professional approach is always the same: first understand the services, then compare the prices. Not the other way around! If you follow this sequence, you protect yourself from unpleasant surprises when it really matters.

In practice: Only around 27.5% of all tariffs received the top rating of FFF+ in the test. This means that most offers do not provide the best value for money.

This figure proves that expensive is not automatically good. With a keen eye and a good comparison, you can find the tariff that really suits you and save money at the same time. It’s also always worth taking a look at customer ratings and independent test reports.

What really matters when it comes to benefits

Before you plunge into the jungle of offers, you should clarify what is important to you. In my experience, these points are crucial:

- Waiver of the defense of gross negligence: a must! This protects you financially if you were careless for a moment – for example when running a red light.

- Amount of cover: The rule here is: get big, don’t get small. It should be at least 100 million euros, more is always better.

- Workshop commitment: Can give you a nice discount, but limits your flexibility. More on this in a moment.

- Marten protection incl. consequential damage: A marten bite is annoying, and the resulting engine damage is ruinous. Make sure that consequential damage is sufficiently covered.

- Mallorca policy: Indispensable for anyone traveling abroad in a rental car. It raises the often paltry foreign liability cover to German standards.

Once you have defined these building blocks for yourself, you can finally compare offers fairly and transparently.

Workshop binding in detail

You can often reduce your premium by 10 to 15 percent with a garage commitment. Sounds tempting, doesn’t it?

The catch: In the event of a claim, the insurer will tell you which partner garage you have to go to. This may mean that you have to travel further or go without your trusted garage around the corner.

- The advantage: You get a noticeable discount, as a kind of loyalty bonus.

- The disadvantage: If you do take your car to another garage, you will be stuck with some of the costs.

- My tip: Check in advance how dense the network of partner workshops is in your area. If the nearest garage is 50 kilometers away, the discount may not be worth the hassle.

An eye-opening comparison

Let’s compare two fictitious tariffs. It quickly becomes clear what is important:

| Feature | Decoy tariff | Price-performance winner |

|---|---|---|

| Annual fee | 399 € | 650 € |

| Workshop binding | Yes | No |

| Waiver gross negligence | No | Yes |

| Sum insured | 50 million € | 100 million € |

| Marten consequential damage | Up to € 1,000 | Up to € 3,000 |

| Mallorca policy | Not included | Included |

At first glance, you save over 250 euros. But a single accident caused by gross negligence or major marten damage can cost you thousands of euros out of your own pocket.

Tip from the expert: True saving does not mean looking at the last euro, but rather not being left out in the cold in an emergency. A close look at the small print is the best investment.

If you want to delve deeper into the world of tariffs, comparison calculators are a powerful tool. We have put together even more useful tips for you in our guide to comparing tariffs at Finanz-Fox.

A practical example with the VW Golf

Let’s take our family with the Golf again. With provider A they pay €1,136 a year, with provider B only €400. A no-brainer, you’d think.

However, provider B does not cover gross negligence and marten damage is limited to €1,000. One night, a marten bites important cables, resulting in engine damage. The repair costs €2,800. The family has to pay €1,800 themselves.

With provider A, the entire claim would have been covered. In this case, the higher premium would have more than paid for itself and saved the family from a financial disaster.

This example shows that far more than just the price plays a role when it comes to changing car insurance. It’s the details that make the difference in the end.

Conclusion: How to make smart savings without skimping on protection

Those who compare regularly are one step ahead. Insurers are constantly enticing customers with promotions and new customer discounts – especially in spring. I recommend doing a thorough check at least every two years.

Write the important deadlines in bold in your calendar so that you don’t miss any deadlines or offers. This way you get the most out of your trip without compromising on safety.

- Keep an eye on promotions: Short-term offers often offer the greatest savings potential.

- Take advantage of family discounts: If you have several cars, ask specifically for bundled discounts.

- Make online calculators part of your routine: Use it every spring to sound out the market and stay up to date.

With this knowledge, you are well prepared for your next insurance change.

The no-claims bonus – your cash – in the right place

Your no-claims bonus class, often simply called SF class, is worth its weight in gold. It is the decisive lever for the amount of your insurance premium and rewards you with hefty discounts for every accident-free year. If you make a mistake when transferring to a new provider, it can quickly cost you hundreds of euros a year.

In principle, the change is very straightforward: Your new insurer requests the SF class electronically from your old company. The most important thing is that the information you provide in the application is 100% correct. This is the only way to avoid annoying queries and unnecessary delays.

But as we all know, the devil is in the detail. Especially if you pass on the discount within the family or return to driving after a long break, there are a few pitfalls lurking. So if you are thinking about what you need to consider when changing your car insurance, you should take a very close look here.

Transfer SF class in the family? How to do it right

A classic: parents or grandparents pass on their no-claims bonus to their children or grandchildren. This is of course a fantastic starting aid for new drivers who would otherwise have to struggle with extremely high premiums.

But it’s not quite that simple. The insurers have clear rules here, which they also check carefully:

- Regular use: The person who is to receive the discount must have actually driven the car of the person handing it in on a regular basis. A joyride at the weekend is not enough.

- Close relatives: The transfer usually only works between spouses, children or people living in the same household. Unfortunately, you cannot bequeath your discount to a nice neighbor.

- Driving license rule: This is the most important point! The recipient can only take over as many accident-free years as he himself has a driver’s license. If the son has had his driver’s license for five years, he can only take over five of his father’s 30 accident-free years.

A practical example: Grandma gives up driving and wants to transfer her SF class 25 to her 20-year-old grandson. However, as he has only had his driver’s license for two years, he can only claim SF class 2 for himself. In this case, the huge remainder of the discount is unfortunately forfeited.

Special cases where you need to be careful

In addition to passing it on within the family, there are a few other situations in which you need to be careful not to lose the valuable discount.

Discount from your second car

Would you like to use the SF class of your second car for your new main vehicle? No problem, this is generally possible. But beware: the classifications for second cars are often worse than those for first cars. Check carefully whether it is really worth swapping.

Insurance pause

If you take your car out of service for a while and pause the contract, your SF class will not be lost. Most insurers suspend the discount for up to seven years. A few are even more generous and extend this period to ten years. It is worth asking specifically here!

Every insurer calculates differently

This is a point that many people don’t have on their radar: Every provider cooks its own soup and has its own SF table. An SF class of 10 can mean a discount of 35% with insurance company A, but perhaps only 32% with insurance company B. The new rate may therefore be a little more expensive despite the identical SF class. So don’t just compare the class, but always the final price.

Well thought-out vehicle financing also helps to keep the overall costs under control. If you are unsure about the best way to finance your car, our guide to leasing or car loans could be an interesting read for you.

Avoid the most common mistakes when switching

Drivers fall into the same traps every year. Changing car insurance becomes unnecessarily expensive or, in the worst case, even ineffective. But don’t worry, if you know where the typical stumbling blocks lurk, a smooth transition really isn’t rocket science.

The absolute classic is and remains, of course, missing the notice period. Anyone who misses the deadline of November 30 is often annoyed by an old, usually more expensive contract for another year. But there are also more subtle mistakes that can be at least as annoying.

False statements and their bitter consequences

One risk that many people massively underestimate is inaccurate or embellished information in the new insurance application. The idea is tempting: simply lower the annual mileage and the premium will drop. But this little trick can come back to bite you later.

If the insurance company discovers in the event of a claim that the actual mileage is significantly higher, there is a risk of hefty contractual penalties. Sometimes the insurer even refuses to pay the claim altogether. The same applies to the group of drivers: if the 18-year-old son regularly drives the car, he must also be included in the contract. If he is not, the entire insurance cover is at stake.

A practical tip: Always be absolutely honest with your details. Report any changes, such as a higher mileage or a new driver, immediately. The small premium adjustment that may become due is nothing compared to the financial disaster that threatens in the event of uninsured damage.

Insurance gaps and the small print

Another critical point is the seamless transition. The new contract must be seamlessly linked to the old one. An insurance gap of even a single day means that your vehicle is no longer allowed on the road. The golden rule is therefore: only cancel the old contract when you have the new provider’s firm commitment and electronic insurance confirmation (eVB number) in black and white.

The current willingness to switch in Germany is high – many people want to save money. At 18%, this is particularly pronounced among men, high earners and FDP voters. However, focusing purely on price is a fallacy. The price differences between a low-cost tariff and a solid mid-range offer can quickly amount to 52%. Those who panic at price increases of up to 20 percent and accept the first offer that comes along often overlook important details such as a garage commitment or the limited scope of validity in other EU countries. If you would like to delve deeper into the motives of the switchers, you can find further insights on dasinvestment.com.

Keep these points in mind and you will be on the safe side:

- Missing the notice period: The most common and most expensive mistake. A red entry in the calendar for 30.11. is mandatory.

- Cheating on mileage: This will come to light in the event of a claim and lead to additional payments or loss of benefits.

- Just look at the price: cheap is not always good. Take your time and compare the services in detail.

- Risking an insurance gap: First the new commitment, then the old termination. Never the other way around.

Incidentally, good insurance cover doesn’t stop at the car. In our guide, we show you how you are also optimally covered in the private sphere, for example with personal liability insurance.

The most frequently asked questions about changing insurance

Changing insurance is basically straightforward, but the devil is often in the detail. Over the years, a few questions have emerged as real classics that come up again and again. I have summarized the most important answers for you here so that you don’t get tripped up.

What if I missed the notice period on November 30?

Take a deep breath – this is no reason to panic. If the deadline for normal termination has passed, the race is not yet lost. Your next, decisive look should now be at your last premium invoice.

Very often, a special right of termination is hidden here. This arises whenever your insurer increases the premium without improving the benefits to the same extent. Sometimes even small adjustments to the type or regional class are enough to open this door for you. As soon as you receive this notification, you usually have one month to give extraordinary notice of termination. If there is no such clause, your contract will unfortunately usually be extended for another year.

First take out the new insurance and then cancel the old one?

Yes, definitely! This is not only the safest way, but the only sensible way. Please never do it the other way around. An insurance gap of just one day can mean real trouble, because then your car may not be driven another meter on public roads.

So proceed strategically: Take your time to find a new tariff that really suits you. Submit the application and wait for a binding confirmation from the new provider. As soon as you have the new policy or at least the electronic insurance confirmation (eVB number) in your hand, cancel your old contract. This way, the transition is seamless and you are protected throughout.

My golden rule is: always confirm first, then cancel. This saves you any risk and unnecessary stress with the registration office.

Can the new insurer simply reject my application?

This question often causes a certain amount of nervousness, but the answer is quite clear. In the case of motor third party liability insurance, i.e. the legally required part, a refusal is extremely rare. Insurers are subject to a so-called obligation to accept (or obligation to contract), which is intended to ensure that every vehicle owner receives the necessary basic cover.

The picture is different for voluntary comprehensive insurance (partial and comprehensive cover). Here, the insurer is free to decide and even reject an application. Typical reasons for this in my experience are

- Too much previous damage in the recent past

- A vehicle model that is considered particularly risky (e.g. high-powered sports cars)

- A negative credit report or unpaid invoices with other insurers

And this is precisely why it is so important to wait for written confirmation from the new provider before terminating the old contract.

What happens to my no-claims bonus when I change?

Don’t worry, your hard-earned no-claims bonus (your SF class) is your most valuable asset and will of course not be lost if you change insurers. The new insurer simply requests this data electronically from your old insurer. This is a standardized process.

All you have to do is provide correct information about your previous insurance and the length of time you have been driving accident-free. However, there is one small detail to bear in mind: The tables that convert an SF class into a specific discount rate in percent are not identical for every provider. Your SF class therefore remains the same, but the resulting discount may be slightly different.

A well-planned change of insurance can save you several hundred euros every year. If you want to get the best deal not only on car insurance but also on other financial matters, Finanz-Fox is the right place for you. Compare top offers for loans, insurance and more quickly and easily at https://www.finanz-fox.de.