Comparing homeowners’ and landowners’ liability insurance is more than just a chore – it is worth hard cash for every property owner and can secure their livelihood in an emergency. Just imagine: An ungritted sidewalk in winter, a roof tile that comes loose in a storm, or an old tree that crashes into the neighbor’s car. In all these cases, you as the owner are liable for the damage caused to others on your property. The right tariff is not a mass-produced product, but must be tailored precisely to your personal situation and your property.

Why the right protection for your property is crucial

As a property owner, you have a responsibility that many people tend to forget in everyday life. The legislator calls this the duty to ensure public safety. It sounds cumbersome, but it simply means that you must ensure that your property does not pose a danger to others. If you breach this duty, it can be really expensive.

A classic, but unfortunately recurring example: a pedestrian slips on your icy sidewalk and breaks their leg. The resulting claims are often enormous – treatment costs, compensation for pain and suffering, loss of earnings, perhaps even a lifelong pension. Such sums can quickly run into the millions. Without good home and landowner’s liability insurance, you are liable with everything you own.

Remember: this insurance is not just a paymaster in the event of an accident. It is also your personal shield against unjustified claims and thus functions like passive legal protection. The insurer checks the claims and defends you against unfounded or exaggerated claims – even in court if necessary.

Risks for different owners

The potential sources of risk are as varied as the properties themselves. A rented apartment building harbors completely different risks than an unused plot of land.

- For landlords: The dangers often lurk in the details. A loose banister, a broken step or poor maintenance of the heating system can quickly lead to liability cases.

- For condominium owners’ associations (WEG): The association as a whole is liable if damage is caused to the common property – for example by a leaking roof or crumbling plaster on the façade.

- For property owners: Even an undeveloped property is not a risk-free zone. Old, rotten trees can fall onto the neighboring property during a storm and cause immense damage.

With older buildings in particular, there is sometimes a particularly tricky issue: the safe disposal of asbestos, which can lead to enormous liability risks if not handled properly.

With our guide, we take you by the hand so that you can compare the rates in a targeted manner and find exactly the protection that fits your property perfectly. If you want to understand how these comparison tools work in detail, take a look at our article on the advantages of a comparison platform.

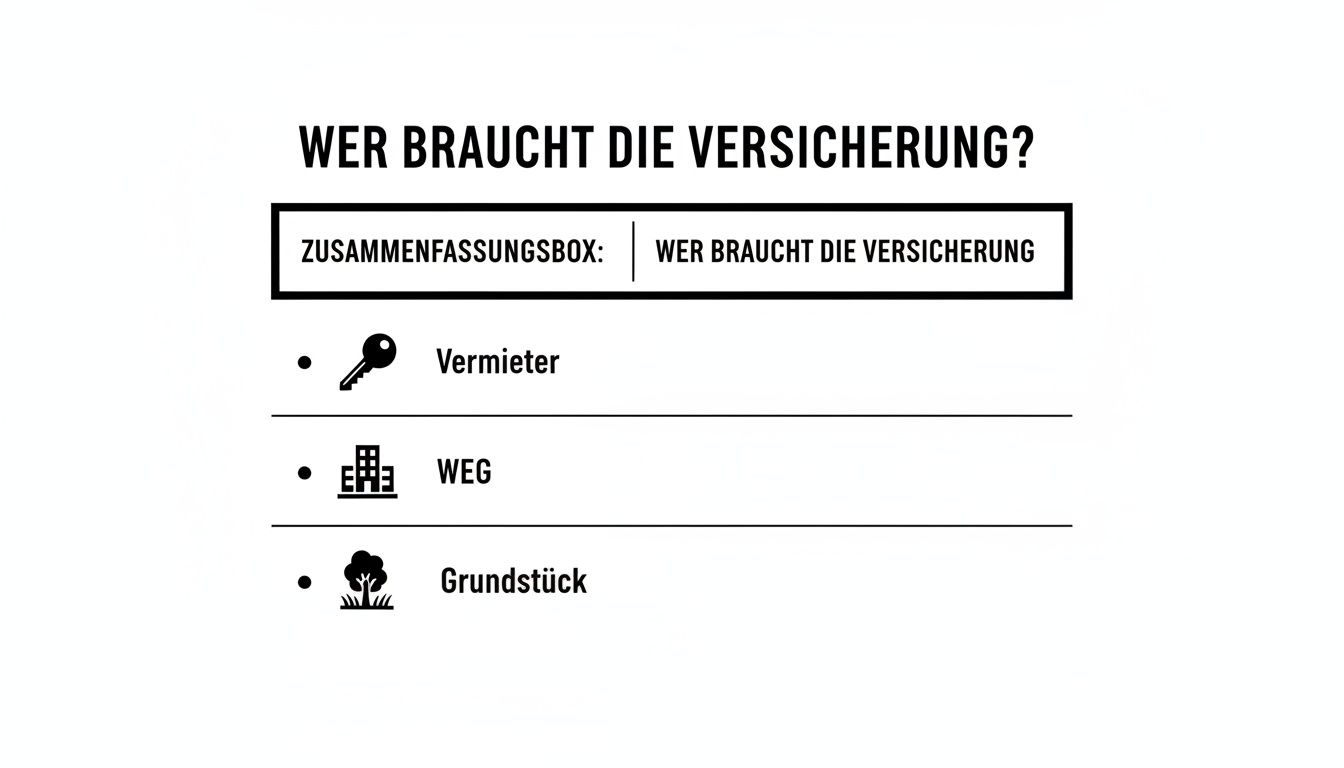

Who really needs home and landowner’s liability insurance

As a property owner, your responsibility does not end at the front door, it starts at the property boundary. This is where the so-called duty to maintain public safety comes into play – a legal term that is quite complex. It means nothing other than that you are liable for damage caused to others on your property. Homeowners’ and landowners’ liability insurance is the direct answer to this often underestimated risk. But who really needs it?

Many people are lulled into a false sense of security and think that their personal liability insurance already covers everything. This is a fallacy, as this cover only applies in one very specific case: if you live in a detached house alone with your family. As soon as something changes in this constellation, there is a gap in the insurance cover that can threaten your existence in an emergency.

Landlords and condominium owners’ associations

For landlords, this insurance is not an optional extra, but an absolute must. It doesn’t matter whether you rent out an entire apartment building, a single condominium or just a small granny apartment – your private liability is out of the question here. Any damage caused to a tenant or their visitors on the property is your responsibility.

Just imagine a tenant tripping in a dimly lit stairwell or a visitor slipping on damp leaves in the courtyard. Without homeowners’ and landowners’ liability insurance, you are liable for treatment costs, compensation for pain and suffering or even a lifelong pension – with your entire personal assets.

One sticking point that you should definitely keep in mind when comparing homeowners’ and landowners’ liability insurance: cover against damage caused by the tenant but for which you as the owner are responsible. The classic example is an improperly installed flower box that falls from a balcony and injures a passer-by.

Insurance is also essential for homeowners’ associations (WEGs). Here, it is not the individual owner but the community as a whole that is liable for damage caused to the common property.

- Falling roof tiles: A loose tile comes loose during a storm and crashes onto a parked car.

- Leaking roof: Rainwater seeps through the communal roof and ruins the new furnishings in a co-owner’s attic apartment.

- Poor winter service: The clearing service commissioned by the condominium owners’ association overlooked an icy spot – the letter carrier falls and breaks his arm.

The costs of such damage are otherwise passed on to all owners. The insurance therefore protects the assets of each individual member of the community.

Property owners and special cases

Insurance cover is not only an issue for developed land. Even if you “only” own an undeveloped plot of land, you still have an obligation. You must ensure that your land does not pose a risk to others. This could be a rotten tree that threatens to fall onto the road during the next storm, or an unsecured, old foundation on which children playing could injure themselves.

So let’s summarize for whom the policy is a must:

| Who are you? | Do you need the insurance? | Why is that? |

|---|---|---|

| Landlord (no matter what and how much) | Absolutely essential | Private liability insurance generally excludes rented accommodation. |

| Condominium owners’ association (WEG) | Absolutely essential | The community is jointly and severally liable for damage to the common property. |

| Owners of undeveloped land | Absolutely essential | The traffic safety obligation also applies to fallow land and the dangers emanating from it. |

| Owners of owner-occupied single-family homes | Generally not necessary | This is where private liability insurance normally steps in. But it never hurts to take a look at your policy! |

The last point in particular is crucial. Check the conditions of your private liability insurance very carefully. As soon as you sublet even one room, set up a granny apartment or share the house with a second family, the cover in most tariffs expires. It is precisely in these situations that a targeted home and landowner’s liability insurance comparison is essential in order to close a dangerous gap in cover.

What really matters when it comes to homeowners’ and landowners’ liability insurance

A low price is tempting, no question about it. But if something actually happens, the supposed bargain can quickly turn out to be an expensive disappointment. That’s why looking at the specific features is the be-all and end-all when comparing home and landowner liability insurance. It is precisely here, in the small print, that the wheat is separated from the chaff – and solid protection from a sketchy tariff.

This infographic shows at a glance for whom this protection is essential.

You can see immediately that whether you are a landlord, part of a homeowners’ association or the owner of an undeveloped property, you all have a duty to ensure public safety and therefore need this protection.

The sum insured: your most important protective shield

The sum insured is the absolute maximum amount that your insurance will pay in the event of a claim. With skyrocketing costs for medical treatment, expensive repairs or lengthy court cases, a high sum is more important today than ever before. A few years ago, 10 million euros might have been considered sufficient, but those days are definitely over.

The reality is that claims can quickly run into the millions. The market is also responding to this: independent rating agencies such as Franke-Bornberg recommend a minimum cover of 50 million euros for personal injury and property damage for new tariffs from 2025. Some top insurers, such as GEV, already offer cover at this level in their premium tariffs, while others, such as Die Bayerische, have raised their sums to a respectable 25 million euros. If you would like to delve deeper into the background to these new valuation standards, you will find interesting insights here.

If the sum insured is too low, this is a financial game of roulette. If the damage exceeds the sum insured, you are liable for the remaining amount with your entire personal assets. Saving a few euros on the annual premium can therefore cost you hundreds of thousands or even millions in the event of an emergency.

The deductible: Saving with a sense of proportion

The excess is the amount you pay out of your own pocket in the event of a claim. Of course, a higher deductible lowers the annual premium, but this decision needs to be carefully considered.

- The advantage: you immediately save money on ongoing insurance costs.

- The disadvantage: you have to pay for minor damage yourself, and for major damage you have to pay the agreed amount.

Ask yourself honestly: What amount can I easily afford to pay if the worst comes to the worst without running into financial difficulties? In most cases, an excess of between 150 and 250 euros is a sensible compromise between premium savings and a financial buffer. If you want to know more about how premiums and benefits interact, our article on optimizing your personal liability insurance provides useful tips.

The key clauses that make the difference

In addition to the big figures such as the sum insured and deductible, it is often the special clauses that determine the quality of a tariff. Be sure to look out for these points when making your comparison:

- Co-insurance for building projects: Are you planning minor renovations or modernization? A good policy includes builder’s liability insurance for projects up to a certain amount (e.g. 100,000 euros) free of charge. This saves you having to take out a separate and often expensive insurance policy.

- Damage caused by photovoltaic and solar systems: A system on the roof is a potential source of danger. If a module comes loose during a storm and damages something, it can be really expensive. Check whether such systems are explicitly and sufficiently insured.

- Securing oil tanks: A leak in a heating oil tank is every homeowner’s nightmare. The contaminated soil has to be extensively cleaned up – costs in the millions are not uncommon. Protection against such water damage is absolutely vital for anyone with an oil heating system.

- Gradual damage: This is damage that does not occur suddenly, but develops over a long period of time. The classic example: an unnoticed dripping pipe softens the neighbor’s wall over a period of months.

- Waiver of the objection of gross negligence: This clause is worth its weight in gold. It ensures that the insurance pays out even if you are accused of a clear breach of duty – for example, if you forget to close a basement window during heavy rain and the neighbor’s basement is flooded as a result.

A thorough home and landowner liability comparison is therefore much more than just a price check. It’s about finding the exact benefit modules that match the individual risks of your property and really have your back in an emergency.

How your insurance premium is determined

The premium for homeowners’ and landowners’ liability insurance is anything but a lump sum. You can think of it more like a jigsaw puzzle, where each piece influences the final cost. A careful comparison of homeowners’ and landowners’ liability insurance will quickly show you where insurers are tightening the screws – and where you can make targeted savings without jeopardizing important protection.

By far the biggest factor in the calculation is the type of property you own. What matters most to the insurer is the risk, and this is of course completely different for a quiet, undeveloped property than for a fully rented apartment building with hustle and bustle in the stairwell.

The property itself as the linchpin

An undeveloped property is generally the cheapest to insure. This mainly concerns risks such as falling trees or an unsecured excavation pit. However, as soon as there is a building on it, the risk increases and so does the premium.

Insurers take an even closer look at rented properties. The decisive factor is not only the number of apartments, but often also the gross annual rent. It serves as a kind of yardstick for the size and value of the house and thus for the potential amount of damage.

- Rented single-family home: The risk here is still quite manageable, which is reflected in moderate premiums.

- Apartment building: Statistically speaking, every additional tenant increases the likelihood of something happening. More people, more movement, more potential liability risks.

- Commercial units: If there is a store or doctor’s surgery on the first floor, this means constant public traffic. Insurers usually charge a premium for this increased risk.

Clever design of deductible and contract term

An effective lever for directly influencing the costs is the excess. This is the amount you pay out of your own pocket in the event of a claim. Although a higher excess noticeably reduces your annual premium, it is not always the wisest decision.

Think about it: an excess of €500 sounds tempting, but if you have two minor claims in quick succession, you’re quickly out €1,000. A lower excess of €150, for example, may be a better compromise in the long run.

The choice of deductible is a very personal risk assessment. Only opt for a sum that you can really handle easily in an emergency without breaking a sweat.

The contract term can also pay off. Many providers give a small discount if you commit for three years. Also see if there are any bundled discounts if you have other policies with the same insurer. Incidentally, this is a detail that is often overlooked when analyzing real estate financing and the associated costs.

Why market comparison is more important today than ever

The insurance market never sleeps. Inflation, exploding construction costs and a generally higher claims frequency are forcing insurers to constantly recalculate their premiums. This shows how crucial it is to regularly compare homeowners’ and landowners’ liability insurance. Otherwise you may soon be paying too much for a policy from yesterday.

A current example underlines this dynamic: Haftpflichtkasse, a large German insurer, will adjust its premiums from July 2025 – after seven stable years. The reasons? In 2023 alone, the claims burden in general liability rose by a whopping 14.56% compared to the previous year. The result is a premium adjustment of 10%.

These developments make one thing clear: if you simply let your contract run its course, you are giving away money. Only if you actively compare can you be sure that your cover is not only suitable, but also fairly priced.

What really counts in an emergency: Stories from real life

Insurance clauses often sound terribly theoretical. But you only realize what they are really worth when the theory suddenly turns into a real emergency. A good home and landowner’s liability insurance comparison will prepare you for precisely this moment. The following stories are taken directly from real life and show how quickly a little negligence can turn into a huge financial problem – and how the right protection can secure your own existence.

Case 1: The icy landing

Imagine Mr. Meier. He rents out a small apartment building and is responsible for winter maintenance. On a freezing cold January morning, he is in a hurry and forgets to grit the steps to the entrance. A treacherous layer of ice had formed overnight. His tenant, Mr. Kurz, doesn’t notice the slippery patch on his way to work, has an unfortunate fall and breaks his wrist.

What follows is a chain of consequences. Mr. Kurz is absent from work for weeks. His health insurance company knocks on Mr. Meier’s door and wants the treatment costs reimbursed. Mr. Kurz himself demands compensation for pain and suffering and claims his loss of earnings. Suddenly there is a claim for over 15,000 euros.

Fortunately, Mr. Meier had homeowners’ and landowners’ liability insurance. He reported the case, the insurance company checked the facts, recognized the breach of the duty to maintain public safety and paid the full amount. Without this cover, Mr. Meier would have had to pay everything out of his own pocket. An expensive omission.

Case 2: The rotten tree in the storm

The Schmidt family has a beautiful large plot of land on which stands an old maple tree – the family’s pride and joy. What they don’t realize: Inside, the tree is already rotten. When a violent autumn storm hits, a massive branch breaks off and crashes directly onto the neighbor’s brand new car. The damage is immense: around 25,000 euros.

The neighbor naturally demands compensation. The Schmidt family contacts their insurance company, but this is where things get complicated. Because the question of fault is anything but clear. Should the family have recognized the dilapidated condition of the tree? Should they have carried out a regular inspection?

This is precisely where one of the most important, often overlooked benefits of homeowners’ and landowners’ liability insurance comes into play: passive legal protection. The insurance not only pays out if a claim is justified. It also defends you against unjustified or excessive claims – in court if necessary.

In the Schmidts’ case, the insurance company called in an expert. His verdict: the internal damage to the tree was not visible from the outside. The insurance company successfully defended the neighbor’s claim and paid the entire legal and expert costs of several thousand euros.

Case 3: The leaking roof of the community of owners

In a residential complex with 20 parties, a few roof tiles came loose unnoticed over the winter. Nobody noticed. Then comes the heavy rain. Water seeps in, seeps through the ceiling of the attic apartment and ruins the Lehmann family’s high-quality furnishings. The damage to the furniture and electronics, together with the need to dry out the building, adds up to almost 40,000 euros.

The property management immediately reports the damage to the insurance company of the homeowners’ association (WEG). As the damage originated from the common property, the condominium association is liable as a whole.

The insurance company steps in and pays twice:

- Settlement of the property damage: It pays for all the damage to the Lehmann family’s property.

- Assumption of follow-up costs: It pays for professional drying to prevent expensive consequential damage such as mold.

If the condominium had not been insured, the amount of damage would have had to be apportioned among all 20 owners. This would have meant an unexpected special contribution of 2,000 euros for each party. These examples make it clear that a careful comparison of homeowners’ and landowners’ liability insurance is not a chore, but an absolutely sensible investment in the financial security of your property.

How to find the best tariff for you

At first glance, the insurance market for homeowners’ and landowners’ liability insurance can seem quite confusing. Every provider advertises different strengths, and the rates often differ only in tiny but important details. But don’t worry: with the right strategy, you can systematically find the cover that really suits you and your property. A thorough home and landowner’s liability insurance comparison is much more than just a price check – it’s about the entire package and the quality behind it.

The best way to do this is to rely on the experience of professionals. For property owners, this insurance is an absolute must, and experienced brokers know exactly which providers are really reliable in the event of a claim and don’t just look good on paper. According to a broker survey conducted in 2025, Haftpflichtkasse is ahead in this respect: with an impressive 24.23% of mentions, it consolidates its position as the clear number one. Its strength lies above all in the speedy processing of applications and policies, where it received a top score of 1.54. GEV Grundbesitzer has established itself closely behind with a strong rise to third place.

It’s more than just the price that counts

A low premium is of course attractive, but in an emergency, completely different things are decisive. Imagine you have to report a claim urgently – how easy is it to contact the insurer? How quickly and easily will your problem be solved? This is exactly where the wheat is separated from the chaff.

The quality of service in the event of a claim is not a minor matter, but the heart of every insurance company. A provider that is almost impossible to reach by phone or unnecessarily drags out the processing only causes additional stress when your nerves are already frayed.

When making your comparison, you should therefore consciously keep an eye on these service aspects. Independent assessments and broker surveys, such as the one just mentioned, provide valuable information on how an insurer really performs on a day-to-day basis. To obtain specific quotes, you can submit a non-binding inquiry directly to various providers.

Your personal checklist for the tariff comparison

A clear structure helps you to maintain an overview and compare offers fairly. Use the following checklist as your personal guide to systematically go through the points that are most important to you:

- Sum insured: Is the sum insured for personal injury and property damage high enough? Today, it should be at least 50 million euros to be on the safe side.

- Deductible: Is the deductible suitable for your financial situation? Too high an amount can quickly become a burden in the event of a claim.

- Specific risks: Are special sources of danger to your property – such as an oil tank, a photovoltaic system or planned construction projects – really covered?

- Service & availability: Is there reliable information on service quality and how quickly claims are settled?

- Important clauses: Does the insurer waive the defense of gross negligence? Is gradual damage also covered?

- Value for money: Is the annual premium in the end in a fair relationship to the benefits and service you receive?

Armed with this checklist, you can filter the insurers’ offers in a targeted manner. Our comparison calculator at Finanz-Fox helps you to compare the tariffs transparently. Our experts will also help you understand the small print and complete the application quickly and digitally. And if you are generally interested in the topic of financing, you will find valuable tips for a successful loan application in our guide.

Practical questions: What property owners really want to know

Finally, I have collected a few more questions that I come across time and again in consultations. They come directly from practical experience and will hopefully help you to clear up the last little question marks before you make a decision.

How do I get out of my old contract?

With homeowners’ and landowners’ liability insurance, there is usually a notice period of three months to the end of the contract term. This is the classic rule. If you miss this deadline, the contract often runs tacitly for another year – annoying, but common practice.

But there are also ways out. You have a special right of termination in two cases:

- After a claim: Regardless of whether the insurance company has paid out or not, you have one month after the decision to cancel the contract.

- If it gets more expensive: If the insurer increases the price without improving the benefits, you can also pull the ripcord within one month of being notified.

Does my vacation apartment actually count?

You need to take a very close look here. The answer depends heavily on the details in your contract and the type of use. A vacation home in Germany that you use exclusively for yourself could possibly even be included in your personal liability insurance.

But beware: as soon as you rent out the apartment, even if only for a few weeks a year to vacation guests, you definitely need separate home and landowner’s liability insurance. Only this covers the risks arising from constantly changing tenants. So take a very close look at the small print, as the rules are often quite different, especially for properties abroad.

What do I do if something has actually happened?

If the worst comes to the worst, a cool head and the right action are worth their weight in gold. To avoid jeopardizing your claims, it is best to follow this sequence:

- First secure the situation: If someone is injured, provide first aid, of course. Otherwise, make sure that nothing else happens.

- Record everything: Take photos of the damage site, save the names and addresses of possible witnesses and write down briefly how everything happened.

- Report the damage immediately: Call your insurance company or report the incident online – and as quickly as possible. Very important: Do not admit guilt on the spot!

- Let the professionals do it: Forward all letters or claims directly to your insurance company. The experts there will check the claims and take care of everything else.

If you pay attention to these points, you will have the full backing of your insurer. If you want to find out more, you can find further information in our articles on comparing tariffs.

A well-intentioned “I’m sorry, that was my fault” at the scene of the accident can cost you dearly and cost you your insurance cover. After all, the insurance company is there to defend you against unjustified claims. So always leave the legal assessment to people who are familiar with it.

A thorough home and landowner’s liability insurance comparison is and remains the smartest way to optimally insure your property. At Finanz-Fox, we help you sort through the jungle of rates and find the contract that really suits you. Protect your property and your financial future – easily online at https://www.finanz-fox.de.