The starting signal for your own home is not given when you are looking for a property, but right here, with a single, but all-important question: What can I really afford? An honest online calculation of your mortgage is the foundation on which your entire plan is built. It transforms vague dreams into tangible figures.

Your path to home ownership begins with a solid calculation

The journey to owning your own four walls usually starts with a gut feeling – the desire for a home. But to make sure this dream doesn’t fall through, you need a clear, financially sound plan right from the start. This is where an online mortgage calculator becomes your most important ally.

With just a few clicks, it gives you a realistic estimate of your future monthly payments and shows you which financing framework is suitable for you. Instead of poking around in the fog, you immediately create transparency and see how individual adjustments affect your monthly installment.

The key data for your first calculation

Before you start the computer, you should have some basic information ready. Don’t worry, you don’t need to pore over thick folders, well thought-out estimates are enough to get you started:

- The purchase price of the property: Do you already have a specific property in mind or at least a price range for your desired area?

- Your available equity capital: How much savings, credit balances from building society savings contracts or other assets can and want to contribute?

- Your monthly net income: What is available to you (and your partner, if applicable) each month?

- The desired repayment rate: A classic starting rate is often 2%. But remember: a higher repayment rate means that you will get rid of your debt much faster.

With these few figures, you can already run through the first meaningful scenarios. This will quickly give you a feel for the dimensions in which you are operating.

A well-prepared start is more than half the battle. If you understand the basics of your financing before you talk to banks, you can negotiate on an equal footing and avoid costly mistakes.

Understanding the power of interest rates

One factor has a huge influence on your calculation: the current building interest rate. The development of building interest rates in Germany has been turbulent in recent years, to say the least. These fluctuations can make thousands of euros of difference over the term of the loan.

Interest rates have risen sharply since the ECB’s interest rate turnaround in July 2022. Currently, as of January 2026, top conditions for a 10-year fixed interest rate are around 3.6%. What does that mean in concrete terms? Even a tiny interest rate change of just 0.1% can add up to €3,000 to the cost of a €300,000 loan over 10 years. You can also find out more about current interest rate trends in the data from Statista.

This unpredictability makes it clear why it is so important to simulate different interest rate scenarios with a calculator like the one from Finanz-Fox. This allows you to develop a feel for how sensitive your rate is to market changes. It is the first, decisive step in turning uncertainty into financial clarity. This initial calculation is also the perfect basis for everything that follows. You can find out more about this in our article Tips and tricks for a successful loan application.

The figures in the mortgage calculator: what really counts

An online calculator is a fantastic tool, almost like a navigation system for your financial future. It shows you the way, but the quality of the route depends solely on how accurately you enter your data. Let’s take a look behind the scenes together and unravel the terms that determine the success or failure of your financing.

This is not about blindly typing in numbers. It’s about understanding the enormous leverage effect of each individual figure. This is the only way to turn a simple calculation into a well-founded, strategic decision for your future home.

The small but subtle difference: borrowing rate vs. effective interest rate

If you calculate a mortgage online, you will immediately come across these two terms. The borrowing rate (what used to be called the nominal rate) is, so to speak, the “pure” price that the bank charges for the money borrowed. It is the basis for everything, but it is not the whole truth.

The figure that really counts for you is the effective interest rate. In addition to the borrowing rate, it already includes most of the additional costs and fees of the loan – such as brokerage commissions or processing fees. The legislator even stipulates this so that you as a consumer can compare offers fairly.

As a simple rule of thumb, you can remember this: The effective interest rate is always a little bit higher than the borrowing rate and gives you the most honest view of the true cost of your financing.

Your strongest weapon: redemption

The initial repayment is one of the most powerful levers you can use in your overall financing. It determines what percentage of the loan amount you repay in the first year. Of course, a higher repayment means a higher monthly installment. But it also leads to a dramatically faster debt reduction and saves you a fortune in interest over the entire term.

Let’s take a look at a realistic example: A young family wants to buy a terraced house for €450,000 and has €50,000 of equity. The loan requirement is therefore €400,000. Assuming a borrowing rate of 3.5%, it looks like this:

- Scenario A (2% repayment): The monthly installment is around € 1,833. After 10 years, the remaining debt is still around € 316,000.

- Scenario B (3 % repayment): The installment rises to around €2,167. But here’s the thing: after 10 years, the remaining debt is only around €269,000.

Although the monthly burden is noticeably higher, in the second scenario the family has already repaid €47,000 more of their loan after just one decade. This takes a lot of pressure off the follow-up financing.

Security for the future: fixed interest rates

The fixed-interest period is your insurance against rising interest rates. It determines for how many years the agreed interest rate remains absolutely fixed and unchangeable. This is usually 10, 15 or even 20 years.

Of course, this security comes at a price. Longer fixed-interest periods are usually associated with a small interest premium. However, in times of low interest rates or uncertain market forecasts, it can absolutely pay off to accept this small surcharge for decades of planning security. Ultimately, this is a very personal decision that has a lot to do with your willingness to take risks. If you want to delve deeper into the development and comparison of interest rates, you will find valuable information here.

Equity and unscheduled repayments: The turbo for your debt reduction

Every extra euro of equity you contribute is pure gold. It not only reduces the loan amount, but also improves your negotiating position with the bank. The result is often noticeably better interest conditions. Just €20,000 more equity can significantly lower the monthly installment and reduce the total costs by thousands of euros over the term of the loan.

Special repayments are another powerful instrument. These are quasi unscheduled installments that you can “pay” into the loan at any time to reduce the remaining debt more quickly. Many modern contracts allow annual unscheduled repayments of up to 5% of the original loan amount, often even free of charge.

A quick calculation: With our €400,000 loan, an annual unscheduled repayment of just €5,000 would shorten the overall term by several years. The interest savings can quickly reach five figures. When choosing an offer, make sure that flexible special repayment options are included. This allows you to use unexpected windfalls such as a bonus or a small inheritance to pay off your debts directly.

The following table impressively illustrates the impact that even small adjustments to equity and repayments can have on your financing.

Sample calculation of the impact of equity and amortization

| Scenario | Equity | Credit | Repayment rate | Monthly installment | Residual debt after 10 years |

|---|---|---|---|---|---|

| Conservative | 50.000 € | 400.000 € | 2,0 % | approx. 1,833 € | approx. 316,000 € |

| Ambitious | 50.000 € | 400.000 € | 3,0 % | approx. 2,167 € | approx. 269,000 € |

| EK-Strong | 95.000 € | 355.000 € | 2,0 % | approx. 1.627 € | approx. 280,000 € |

| EK-Strong & Ambitious | 95.000 € | 355.000 € | 3,0 % | approx. 1,924 € | approx. 238,000 € |

You can see at a glance: A higher repayment reduces the residual debt massively. If you combine this with more equity, not only does the monthly installment fall, but the residual debt after 10 years virtually melts away. This is the key to carefree follow-up financing.

Read results correctly and forge a clever strategy

Okay, the online calculator has done its job. You now have two crucial figures in front of you: Your expected monthly installment and the residual debt remaining at the end of the fixed interest period. But be careful: these are not pure calculation results. See them as a starting point, as a foundation for your entire financing strategy. Now the most important part begins: putting these figures into the context of your life and your financial plans.

Many people make the mistake of only looking at the monthly installment. My practical tip: focus on the remaining debt. This figure is the real crux of your entire mortgage. It shows the amount you will have to refinance after your fixed interest rate expires – and at the market conditions applicable at that time. A high residual amount is an enormous risk.

The sword of Damocles of residual debt

Let’s imagine this: Your fixed interest rate of 10 years expires. Building interest rates, which were 3.5 % when you took out your mortgage, have now climbed to 6 %. If you now have a remaining debt of €250,000, your monthly burden will literally explode. This can cause an entire household budget to totter.

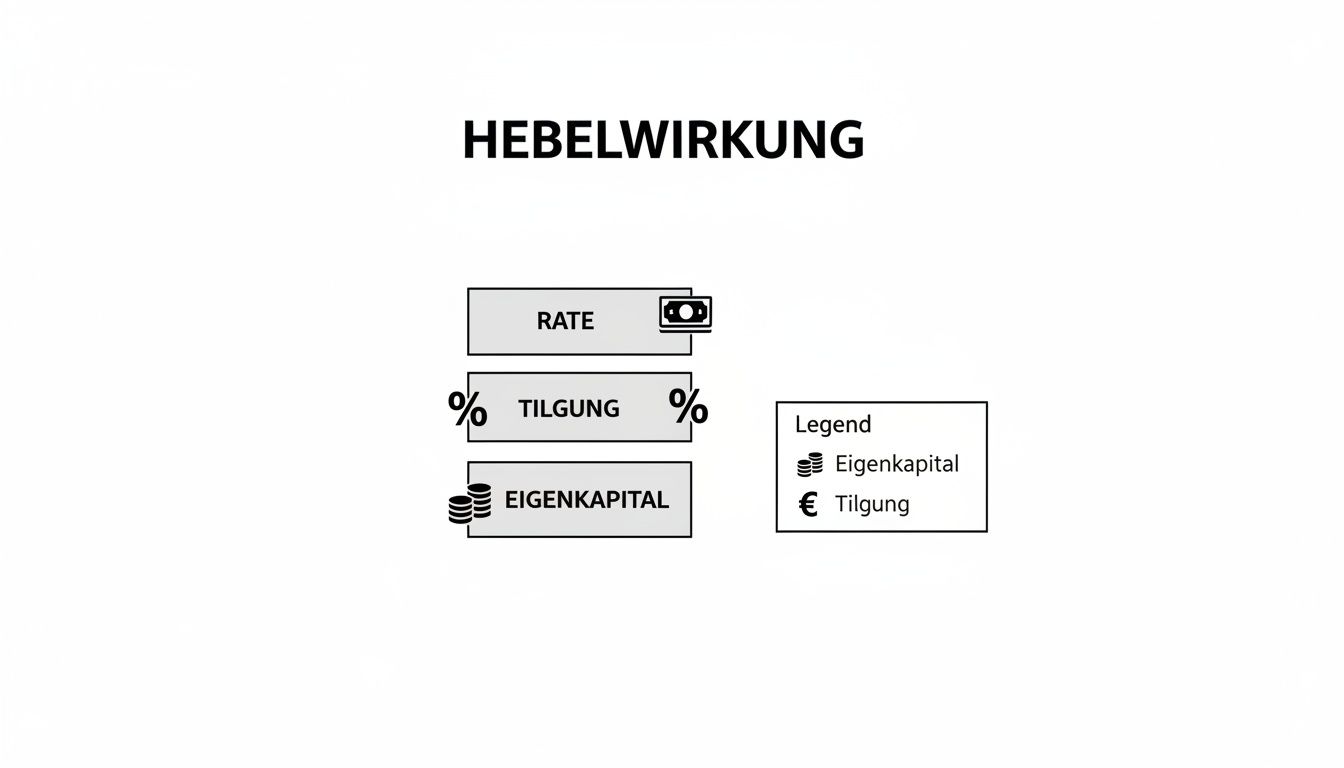

A low residual amount, on the other hand, gives you breathing space, security and flexibility. To defuse this ticking time bomb, you have three powerful tools at your disposal: a higher initial repayment, the clever use of equity and regular unscheduled repayments.

This diagram shows very nicely how these three levers – installment, repayment and equity – interact.

It’s immediately obvious: Only a well thought-out balance between these components will help you to effectively reduce your residual debt.

Use the repayment plan as a compass

A good mortgage calculator will not only provide you with the key data, but also a detailed repayment plan. Think of this document as your personal roadmap to freedom from debt. It shows you month by month how your installment is divided into an interest and a repayment portion.

Sure, at the beginning it’s often frustrating to see how the lion’s share of your installment goes straight to the bank as interest. But keep at it! With each individual payment, the ratio shifts a little in your favor. Because the interest is always calculated on a slightly lower residual debt, your repayment share grows steadily. Understanding this effect is incredibly motivating.

The results of your online calculation are not set in stone. See them as a kind of strategic playground. Play through different scenarios and find the perfect balance between monthly affordability and the quickest way to a debt-free property.

Keeping an eye on the current market situation

When interpreting your figures, you should of course not ignore the current market situation. Following the turnaround in interest rates, the volume of mortgage lending in Germany has plummeted. According to the Association of German Pfandbrief Banks, only 110 billion euros in loans were approved in 2023 – a decline of a whopping 31% compared to the previous year.

For you as a borrower, this means that banks are taking a closer look, demanding more equity and rejecting applications more frequently. This only underlines the importance of a realistic and early online calculation, for example here on Finanz-Fox. This is the only way you can realistically assess your chances.

These stricter conditions make proper preparation all the more important. Your results calculated online are the ideal basis for confidently entering into discussions with financing experts. You will then already know what rate is right for you, what residual debt you are aiming for and what repayment amount you are aiming for.

With this knowledge, you can transform yourself from a supplicant into an informed negotiating partner at eye level. You can compare offers in a targeted manner and ask the right questions. You can use the calculator not only as a calculator, but also as a strategic tool for a secure and sustainable future within your own four walls.

Typical errors when calculating online? How to play it safe

The ability to calculate a mortgage online is fantastic. A few clicks and you have an initial idea of the monthly installment. But precisely this simplicity harbors a danger: it lulls you into a false sense of security.

From my experience, I can say that many prospective homeowners fall into the same pitfalls time and time again. These mistakes can quickly turn the big dream of owning your own home into a financial nightmare. But don’t worry, you can avoid them if you know them. It’s important not just to focus on the purchase price and interest rates, but to keep an eye on the big picture.

Let’s take a closer look at the most common stumbling blocks so that your path to home ownership is built on a solid foundation right from the start.

The classic: the ancillary purchase costs are simply forgotten

To be honest, this is the most common and most expensive mistake. People focus entirely on the purchase price of the property and forget that there is a good chunk of costs on top of that. As a rule, the bank does not finance these additional costs – the money has to come from the equity.

Depending on the federal state, this can quickly amount to 10 % to 15 % of the purchase price. Plan for this sum from the very first second!

- Land transfer tax: The largest item. Depending on the federal state, you can expect between 3.5% and 6.5% of the purchase price.

- Notary and land registry fees: You can apply a flat rate of around 2% for these. These fees are set by law and are non-negotiable.

- Broker commission: If a broker is involved, there is often an additional 3 % to 7 %, depending on the region and agreement.

For a 400,000 euro property, we are quickly talking about 40,000 euros or more. If this money is missing from the budget, the financing will fall through before it has even really started.

An honest cash check is the be-all and end-all. Calculate the total costs from the outset, not just the purchase price. Only then will the online calculation protect you from a rude awakening when the first bills arrive.

The story of the Meier family – a practical example

The Meier family had found their dream home: a charming detached house built in 1985. They sat down at the online calculator, entered the purchase price of €450,000 and their equity of €60,000. The monthly installment seemed feasible, the plan was set.

But what they completely ignored was the need for modernization. The roof was getting on in years, the windows were draughty and the heating was a relic from the old days. When the first cost estimates from the tradesmen arrived – around €50,000 – their entire calculation collapsed.

This amount was not included in their original financing. The family had to rethink their plans, painstakingly refinance them and were suddenly under enormous financial pressure. A buffer for modernization would have saved them all this stress.

Budget planning sewn to the edge

Another critical point: many people calculate their monthly installment so precisely that there is hardly anything left at the end of the month. That is extremely dangerous.

What happens when the washing machine breaks down, the car needs an expensive repair or expenses increase due to a new addition to the family? Financing without a buffer for unforeseen events quickly becomes an unbearable burden. It’s better to plan your installment so that you can continue to live a relaxed life and put something aside each month.

Also think about the running costs that a property entails:

- Property tax

- Building insurance

- Garbage collection

- Reserves for maintenance

These expenses can add up to several hundred euros per month and must be paid in addition to the loan installment.

Only looking at the interest rate and ignoring flexibility

Sure, everyone wants the lowest interest rate. But that’s often short-sighted. A really good financing contract gives you room to breathe and adapts to your life. So when choosing one, make sure you look for options such as special repayments or the option to change the repayment rate.

Special repayments allow you to pay off a larger amount out of turn once a year. A bonus from your boss, a small inheritance or money you have saved can be used directly to reduce the remaining debt. This shortens the term and saves you thousands of euros in interest.

A repayment rate change is worth its weight in gold. Are you getting a pay rise? Then simply increase the repayment. Things get a little tighter financially? Then you can temporarily lower the installment. A careful loan comparison should therefore always consider more than just the interest figure after the decimal point.

From the calculation to the best financing offer

Your online calculation is complete. You now have a compass in your hand to point you in the right direction. You have run through various scenarios, got a feel for rates and terms and developed a really realistic idea of what is possible for you. But how do you turn this theoretical calculation into a solid, binding financing offer? Now the really exciting part begins: turning your figures into reality.

The online calculator has shown you the “what”. Your calculated key data is now the solid basis for the next step, the actual loan application. And this is where platforms like Finanz-Fox come into play. Don’t think of it as just another calculator – it’s much more. It’s your personal marketplace that opens the door to offers from hundreds of banks, savings banks and insurers across Germany. Once you have entered your data, it becomes the basis for a genuine, broad market comparison.

The power of comparison – this is where the money is

Let’s be honest: Imagine having to knock on the door of every single bank personally to get a quote. An insane amount of work. A good comparison platform does exactly this work for you and serves you the right options on a silver platter based on your calculation.

The decisive advantage often lies in the details. Even tiny differences in interest rates, which at first glance hardly seem worth mentioning, have a huge financial leverage effect over the long term of a mortgage.

An interest rate difference of just 0.2 percentage points doesn’t sound like much, does it? But with a loan of 350,000 euros and a fixed interest rate of 15 years, this small difference quickly adds up to savings of over 10,000 euros. That’s money you can use for unscheduled repayments, a new kitchen or simply for your financial security.

Interest rate trends as a strategic factor

Especially in a constantly changing market environment, the right time is worth its weight in gold. Current forecasts on interest rate trends show how important it is to make a precise online calculation and a quick comparison afterwards. Experts expect moderate stability in building interest rates in the near future, which are likely to settle between 3.0 and 3.7 percent – always influenced by the ECB’s decisions and the yields on German government bonds. Slight fluctuations are possible at any time, which is why a quick reaction to good conditions can be worth hard cash. Further analysis shows the complexity of the market.

A platform like Finanz-Fox helps you to make the most of this window of opportunity. You can apply the daily updated conditions directly to your personal situation and immediately see which bank has the best offer on the table for you.

The person behind the numbers

As valuable as digital tools are, mortgage financing is and remains one of the biggest financial decisions of your life. That’s why the last step from calculation to offer is often the most important: personal advice based on your digital results.

An experienced financial advisor at Finanz-Fox takes your online calculated data as a starting point. They will categorize it for you, ask the right questions and shed light on aspects that no calculator in the world can capture:

- Your individual creditworthiness: How does a bank realistically assess your creditworthiness and where can it be optimized?

- Your future plans: Are you planning to start a family? Are you planning to change jobs? How does the financing fit in with your long-term life goals without restricting you?

- State subsidies: Are you entitled to KfW subsidies or other grants that make your financing noticeably cheaper? Thousands of euros often remain unused here.

This advice bridges the gap between what the calculator shows and what is the best solution for you as a person with individual wishes and needs. The aim is not only to find the conditions you want, but also to secure them securely and sustainably. If you would like to find out more about why a comprehensive comparison is so worthwhile, you will find valuable insights here.

Use your calculation as a springboard – take the next step now and make your dream of owning your own home a reality.

What often remains unclear after the first calculation

Even after the most careful online calculation, a few question marks often remain. This is completely normal, after all, we are talking about one of the biggest financial decisions of your life. To take away the last uncertainties, I have compiled the answers to the questions that I encounter most frequently in practice.

Think of it as a final knowledge check before you take the next step. These answers should help you to classify the figures from the calculator correctly and move on with a good feeling.

How accurate is such an online calculator really?

A good online calculator is your best first compass. If you enter your figures honestly and as accurately as possible, you will get a surprisingly precise simulation of your future financial burden. The technology behind it is based on current average interest rates and standard parameters.

However, it is also clear that the final, binding offer from your bank will almost certainly differ slightly. Why? Because very personal factors come into play that an anonymous calculator cannot know:

- Your creditworthiness: How does the bank assess your individual financial reliability?

- The mortgage lending value: What value does the bank appraiser set for your dream property? This does not always have to be the purchase price.

- Your life situation: Your career prospects, family planning and other personal circumstances also play a role.

So consider the online calculator for what it is: a powerful planning tool. It helps you to run through realistic scenarios and be perfectly prepared for discussions with the banks.

What documents do I need for the first calculation?

The good news first: you don’t need any official documents for the very first round of the online calculator. This is purely about getting a feel for the numbers.

All you need are well thought-out estimates. Simply have the most important key data ready in your head: the approximate purchase price, how much equity you have on the high edge and what you have available in net monthly terms. The closer these estimates are to reality, the more valuable the result will be.

Only when things get serious and you obtain concrete offers via a platform such as Finanz-Fox will the banks ask for proof. Then they will ask for payslips, bank statements as proof of equity and, of course, documents relating to the property itself.

A tip from years of experience: never plan to the last cent. Solid financing always has room for life’s surprises.

And what if interest rates rise after I’ve done all the math?

This is a classic case and exactly the reason why you should not hesitate forever once you have found a suitable scenario. The results from the online calculator are always a snapshot of the current interest rate environment. Building interest rates can change on a daily basis – a decision by the ECB or slight unrest on the capital market is enough.

So if you have a calculation that feels good to you, the next logical step is to get a concrete offer via a platform like Finanz-Fox. Once a bank makes you a binding offer, the interest rate in it is reserved for you for a certain period of time – often one to two weeks. This allows you to freeze the conditions, even if market interest rates rise again during this time.

Should I include a buffer in the calculation?

Absolutely! This is perhaps the most important piece of advice I can give prospective property owners. Financing that is sewn to the edge is the best recipe for sleepless nights.

There must always be a financial buffer – for a broken heating system, unforeseen car repairs or other private emergencies. A good rule of thumb is that your monthly installment should not exceed 35-40% of your joint net household income.

My practical tip: Be deliberately a little more conservative when entering the amount in the calculator. Enter a slightly lower income or test a slightly higher rate than you are comfortable with. This way, you build a safety buffer into your calculation right from the start and remain flexible if something unexpected happens.

Do you have your key data ready and feel ready to take the next step? At Finanz-Fox you can compare offers from hundreds of banks free of charge and without obligation. You’ll find the financing that really suits you and your dream home. Start your comparison now at https://www.finanz-fox.de and secure the best conditions.