A second car is needed – whether for your partner, the commute to work or simply for more flexibility in everyday life. But the alarm bells start ringing immediately: are insurance costs going to double? Don’t worry, that doesn’t have to be the case. If you’re clever, you can insure your second car surprisingly cheaply. The key to this lies in the so-called second car regulation.

How to avoid the cost trap with a second car

Many people still believe that a new car automatically starts in the most expensive no-claims bonus class (SF class) 0, which causes premiums to skyrocket. Fortunately, this is a myth. In practice, almost every insurer has a solution to prevent this from happening and to avoid unnecessarily burdening loyal, experienced drivers.

These special regulations are basically a leap of faith. Your insurer knows that you are already accident-free on the road and rewards this with a significantly better rating for the new family member on four wheels. The result? Noticeable savings from day one.

What is really behind the second car regulation?

In simple terms, the second car regulation is a special classification for an additional vehicle that is registered to you or your partner. Instead of the SF class 0 that new drivers get, you often start directly with SF class ½.

Some insurers are even more generous and offer an even better classification – sometimes they even mirror the SF class of your first car. This, of course, maximizes your savings potential.

The hurdles are usually manageable. Typically, a few conditions must be met:

- The policyholder is the same: in most cases, both cars must be insured in your name or in the name of your partner living in the same household.

- Experience counts: Your first car must often already have a certain amount of accident-free time behind it, for example, be classified in at least SF class 3.

- No novice drivers at the wheel: Many providers set a minimum age for all drivers of the second car, often 23 or 25 years.

My practical tip: You almost always get the best deal if you insure both vehicles with the same provider. It can therefore be really worthwhile to switch with your first car in order to benefit from bundled discounts and the best possible special classification.

You should not lose sight of the financing of the car itself. Whether you buy cash, finance or lease also has an impact on your overall costs. If you are still unsure, take a look at our guide, which will show you whether leasing or a car loan is better suited to you.

The most common second car regulations at a glance

This table shows you at a glance which conditions insurers typically set for a better classification of the second car. Use it as a checklist in your search.

| Regulation | Typical condition | Possible classification |

|---|---|---|

| Standard regulation | First car insured with the same company, driver over 23 years of age. | SF ½ |

| Better classification | First car has at least SF 3, drivers over 25 years, no young drivers. | SF 2 to SF 4 |

| “Real” second car regulation | First car has a high SF class (e.g. SF 10), only you and your partner drive. | Same SF class as first car (often with upper limit) |

| Beginner driver regulation | One of your children uses the car, first car is with the same company. | SF ½ (instead of SF 0 for the child) |

As you can see, the options are many and varied. A precise comparison of the conditions is worth its weight in gold and will help you to find the right tariff for your personal situation.

The no-claims bonus: your greatest lever for a favorable premium

When it comes to saving money on car insurance, there is no way around the no-claims bonus. We call it the SF class for short. It is by far the decisive factor for the amount of your premium. The logic behind it is simple: every year that you drive accident-free, you climb up a level and your premium drops noticeably.

The good news is that you don’t have to start from scratch with your second car. Forget the expensive classification that new drivers have to swallow. There are much cleverer ways.

The most common and simplest trick is the so-called second car regulation or special classification directly with your insurer. If your first car has been registered to you accident-free for a while, insurers are often very accommodating. They reward your loyalty and your obviously safe driving behavior by immediately giving the new car a better rating – it often goes straight into SF class ½, sometimes even higher.

How to use the better classification for yourself

Sounds good, doesn’t it? But of course there are a few rules. Every provider puts the exact conditions in their small print a little differently, but there are almost always a few typical hurdles.

- Who is the policyholder? As a rule, both cars must be registered to you or your partner who lives with you in the same household.

- How long have you been driving accident-free? Many insurers require that your first car has already reached a certain SF class, for example SF 3.

- Who can drive? Caution with young drivers! Sometimes the special classification only applies if all drivers are over a certain age, such as 23 or 25.

Take a very close look at these points before you sign a contract. A small difference in the terms and conditions can end up saving you several hundred euros a year – or costing you money.

A practical tip: Ask specifically whether your insurer simply “reflects” the SF class of your first car on the second car. This is not the rule, but as a long-standing, loyal customer in particular, you sometimes have a good chance here. Persistence pays off!

Take a discount from others: This is how it works

There is another very clever strategy: you can take over someone else’s existing no-claims bonus. This is particularly valuable if someone in the family gives up driving.

Imagine the classic scenario: Your grandparents give up their driver’s license and deregister their car. What happens to the high SF classes they have accumulated over decades? They don’t just have to expire! Under certain conditions, you can simply transfer this valuable discount to your new second car.

However, the hurdles here are somewhat higher than with the pure second car regulation:

- Family ties: The transfer usually only works between first-degree relatives (i.e. parents to children and vice versa), between spouses or partners who live together.

- Proof of driving experience: You must provide credible evidence that you have already driven the car of the person handing it over on a regular basis. A corresponding entry as a driver in the old insurance contract is the best proof here.

- The driving license rule: This is the most important point! You can only take on as many years of discount as you have a driver’s license. So a 25-year-old who has been allowed to drive for seven years can only take over SF class 7 at most – even if their grandfather had a flawless SF 30.

Incidentally, this trick is not just limited to cars. It is often possible to transfer the discount from a deregistered motorcycle or motorhome to a new car. So before you sign a new contract, ask around in the family. Perhaps there is still untapped savings potential lying dormant.

Of course, the SF class is only one component. It’s just as important to know the basics, as our article on finding the best personal liability tariff shows.

Choose the right comprehensive cover at no extra cost

When it comes to insuring a second car cheaply, the choice of comprehensive cover is often the biggest lever. Motor third party liability is a legal requirement – there is no room for maneuver. With comprehensive insurance, on the other hand, you have the reins in your hands and can really save money if you choose the cover that really suits your car and your situation.

The all-important question is: What is the car still worth? Is it a ten-year-old small car that is really only used to get to the supermarket? Then expensive comprehensive insurance is usually a waste of money. The high annual premium is no longer in any reasonable proportion to the low residual value of the car.

Partially comprehensive insurance as a happy medium

Partially comprehensive insurance is absolutely the right choice for the vast majority of second cars. It is the perfect compromise between solid protection and an affordable premium. It covers precisely the damage for which you cannot do anything yourself – risks that we all encounter in everyday life:

- Theft: protection you shouldn’t do without, especially in the city.

- Glass breakage: A small stone chip on the highway and the windshield is broken.

- Wildlife accidents: Anyone who often drives overland knows the danger.

- Natural hazards: Storm, hail or flooding can affect anyone.

Comprehensive insurance only really comes into play for newer, valuable or perhaps even financed cars. It also covers damage caused by self-inflicted accidents and vandalism. A luxury that is simply too expensive for an older car with a low current value. If your car is financed, you can also find useful information on this in our articles on suitable car loans.

This comparison will help you to decide whether partially comprehensive cover is sufficient for your second car or whether fully comprehensive cover is worthwhile for you.

Comparison of comprehensive insurance rates: Which cover is worthwhile and when

| Feature | Partial casco | Fully comprehensive insurance |

|---|---|---|

| Theft & robbery | ✔️ | ✔️ |

| Fire & Explosion | ✔️ | ✔️ |

| Damage caused by storm, hail, lightning, flooding | ✔️ | ✔️ |

| Glass breakage (e.g. stone chips) | ✔️ | ✔️ |

| Collision with furred game (e.g. deer, wild boar) | ✔️ | ✔️ |

| Marten bite (consequential damage often only partial) | ✔️ | ✔️ |

| Self-inflicted accident damage | ❌ | ✔️ |

| Vandalism (willful damage) | ❌ | ✔️ |

| Damage caused by the hit-and-run driver | ❌ | ✔️ |

As you can see, the key differences are self-inflicted damage and vandalism. If the value of your second car does not justify these additional costs, partial casco is the smarter option.

An often underestimated practical tip: play with the excess! Many leave it at €150 as standard. Check the comparison calculator to see how much the premium drops if you increase it to €300. The annual savings are often so high that the higher risk in the event of a claim is absolutely worth it.

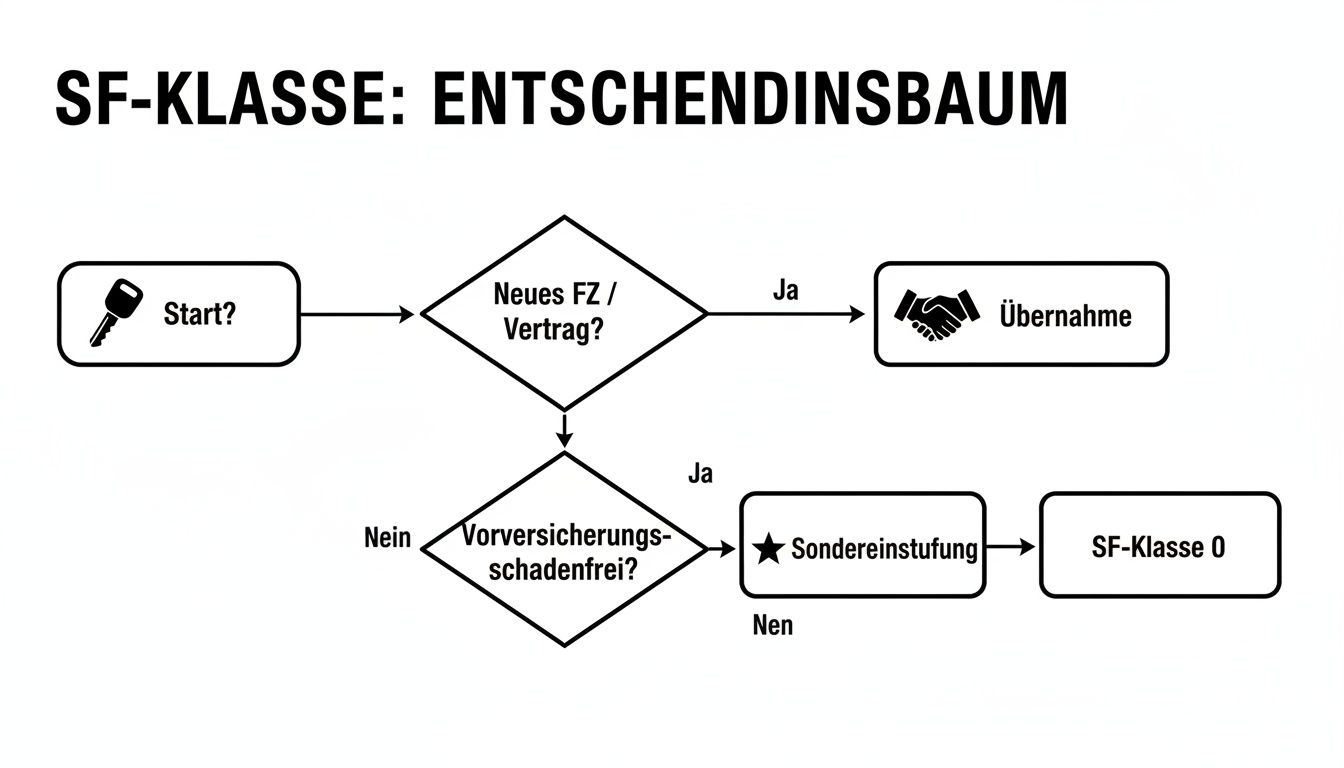

The correct classification of the no-claims bonus class (SF class) is of course the basis for any favorable tariff. This graphic shows you which options are available for your second car.

You can see immediately: either you use a special classification of the insurer or you transfer an existing no-claims bonus. Both are the key to a really low premium for the second car.

Uncover hidden discounts and clever tariff features

The right no-claims bonus class is a great foundation, no question about it. But to insure your second car really cheaply, we need to dig a little deeper. The real savings treasures often lie in the small print of the tariff details and in your own personal driving profile.

With honest information and a few smart decisions, you can often get more than you initially think.

A simple but really effective trick: insure both cars with the same provider. Many companies reward this loyalty with a significant bundled discount, which often applies to both policies. It’s worth actively asking about this, because you won’t always be offered this bonus on your own.

The driving profile as your personal savings booster

The biggest lever you have in your hand, apart from the SF class, is your individual driving profile. Absolute honesty is required here, because incorrect information can be really expensive in the event of a claim. So be realistic, but make full use of the savings potential available to you.

- The kilometers per year: the absolute classic. Think very carefully about how often the second car is really driven. Is it only used for weekly shopping and short trips around town? If so, you may easily stay below the magic limit of 10,000 kilometers per year, which will noticeably reduce the premium.

- The number of drivers: Every person who is allowed to drive increases the risk from an insurance perspective. So limit the number of drivers to the bare minimum, for example only yourself and your partner. Excluding drivers under the age of 23 or 25 often results in the biggest discount.

- The parking lot at night: where does the car sleep? A lockable single garage is the jackpot for insurers and is rewarded with the highest discount. But a carport or a fixed parking space are still much better than parking on the street.

A practical tip: Many people underestimate the impact of such small changes. The change from “lantern parking” to “garage parking” alone can make a price difference of up to 15%, depending on the region and vehicle.

Telematics tariffs: The smart solution for young drivers

Especially when a young driver has to use the second car, the costs often shoot through the roof. A modern and above all fair solution here can be a telematics tariff. Driving behavior is simply measured via an app or a small plug in the car.

The system looks at things like acceleration, braking maneuvers and compliance with speed limits. Those who drive safely and with foresight are rewarded directly – often with discounts of up to 30% on the annual premium. This is not only a brilliant opportunity to save a lot of money, but it also promotes a safe driving style. A real win-win situation.

To help you get a better grip on your finances in general, you can also find other useful financial tips for everyday life here.

What makes your insurance more expensive – and how you can still save

Have you been driving accident-free for years and yet a higher insurance bill flutters through the door? That’s annoying, of course. However, this is usually due to things that you personally have no influence over. If you understand these mechanisms, you can assess offers much better and ultimately make the right decision to insure your second car cheaply.

Basically, there are two major external factors that influence prices here: the general cost trend and, hard to believe, your zip code.

When the workshop invoice becomes a price driver

We are all feeling the effects of inflation, and the automotive industry is no exception. On the contrary: spare parts have become extremely expensive in recent years, and the hourly rates charged by garages have also risen sharply. Just think of a modern headlight – what used to be a simple bulb is now a complex component with LED or laser technology that can quickly cost a small fortune.

This trend naturally has a direct impact on insurance companies. If the average cost per claim increases, providers have to raise their premiums to avoid slipping into the red. Unfortunately, this means that premiums are rising for everyone, even the most careful driver. Such general price increases are not just a car issue, as you can also see from the development of energy costs in Germany.

The latest figures speak for themselves: motor vehicle liability insurance has become 8 percent more expensive on average, fully comprehensive insurance even 12 percent more expensive. The main reason? The insurers’ combined ratio has gotten out of hand. You can read more about the background to these premium adjustments here.

The regional class: your zip code is a deciding factor

An often underestimated factor is your place of residence. Insurers are masters of statistics and assess the risk of damage for every zip code in Germany. The result of this calculation is the so-called regional class.

Very different data is used here:

- Accident density: Statistically, there are simply more accidents in big cities than in the countryside.

- Theft rate: Depending on the region, a particular make of car is stolen more or less frequently.

- Natural hazards: In some areas it hails more often, in others there is more storm damage.

So if you move to an area that is statistically classified as “riskier”, your premium may increase – even if your car and no-claims class remain the same. Moving to the countryside, on the other hand, can have a positive effect. It is precisely because of such external influences that it is so important not to simply let your insurance run for years, but to compare it regularly.

Your questions about second car insurance – answered briefly and concisely

Finally, we will address the questions that I am asked time and again in my day-to-day advisory work. Here you will get clear answers to the typical stumbling blocks and can clear up any last doubts before you insure your second car at a reasonable price.

It’s often the small details that ultimately make the difference between a good deal and an expensive contract. Let’s tackle the most common ambiguities head on.

Do I have to register my second car with the same insurance company?

No, you don’t have to. You are completely free to choose the provider and are not obliged to insure both cars with the same company. Sometimes a different insurer is even cheaper on paper for the second car, for example because it classifies the specific model in a better type class.

But beware, there’s a catch here. If you choose two different providers, you often miss out on two decisive advantages:

- The combined or bundled discount: Many insurers reward your loyalty if you take out several policies with them.

- The uncomplicated special classification: The particularly attractive second car regulation, which secures you a better SF class, is usually linked to the fact that the first car is also insured there.

So do your sums very carefully. A supposedly cheaper individual offer can end up costing you more if you lose discounts on your first car contract.

My practical tip: Always calculate two scenarios. First: both cars with the previous provider. Secondly: the second car with a new, cheaper insurer. Only a direct comparison will show what will really end up in your wallet.

Does the second car regulation also work for novice drivers?

Absolutely, and this is one of the best money-saving tips for families! A novice driver who registers their first car usually ends up in the extremely expensive SF class 0, which really hurts.

The clever way out: the son’s or daughter’s car is registered as a second car to the parents. As a result, the young driver benefits from the special classification and often starts directly in SF class ½ or even better. This saves hundreds of euros from day one.

Later, when the next generation has been driving accident-free for a few years, the contract and no-claims bonus can simply be transferred to them. This is an elegant and effective way of avoiding an expensive entry-level policy.

What happens to my SF class if I have an accident with the second car?

Here you can rest assured: an accident with the second car has absolutely no effect on the no-claims class of your first car. Each insurance contract runs separately.

If you cause damage with the second car, only its SF class will be downgraded in the following year. The hard-earned discount on your main vehicle remains completely unaffected. This gives you enormous security, as a minor mishap does not immediately ruin the entire discount system.

Can I transfer the no-claims bonus from my motorcycle to my car?

Yes, with most insurers this is surprisingly straightforward. For example, if you deregister your beloved motorcycle and buy a practical second car instead, you can simply take the no-claims bonus you have built up over the years with you.

The prerequisite is usually that the owner remains the same and the vehicles follow each other seamlessly, i.e. there are no large gaps between deregistration and registration. This ensures that your valuable discount does not expire and that you insure your second car at a favorable price right from the start.

A favorable rate for your second car is a great start. With Finanz-Fox, you can quickly and easily find the best offers for all your financial and insurance needs – from car loans to the right policy for your home. Compare now at https://www.finanz-fox.de and get the best out of your finances.