If you’re faced with the decision of whether to finance or lease your next car, there’s a pretty simple rule of thumb: financing means you’re heading for ownership – ideal for a long-term commitment. Leasing is more like renting for a period of time. Perfect for those who like to drive the latest model every few years and don’t want to worry about reselling.

So your choice essentially depends on what is more important to you: building up a tangible asset or enjoying maximum flexibility with often lower monthly installments.

Financing or leasing – what suits me better?

The question of how best to finance the next big purchase – be it a car or an expensive machine – is a major concern for many people. Financing or leasing? There is no general right or wrong answer here. Rather, it’s about finding the solution that fits your life and financial situation like a glove.

Let’s look at the whole thing without complicated technical jargon. The essential difference revolves around a single question: who is the owner in the end and who bears the associated responsibility?

The fundamental difference in a nutshell

Financing is basically a classic installment purchase. You take out a loan to buy something, pay it off in installments and when the last installment is paid, the good thing is yours. From that moment on, you have complete freedom: You can convert it, sell it or simply keep driving it for as long as you want. However, you also bear the full risk of depreciation.

Leasing is a different matter. Here, you rent the vehicle for an agreed period of time and only pay for its use, so to speak. The monthly installments are therefore often significantly lower. At the end of the term, you simply return the car. Simple and uncomplicated.

The key consideration is: do you want to pay for ownership or just for use? The answer to this question is the first and most important step in your decision.

Direct comparison: financing vs. leasing

To give you a quick overview, we have directly compared the most important points of both models. This allows you to see at a glance which aspects are most important to you personally.

Direct comparison of financing vs. leasing

A comparison of the key features of financing and leasing as a quick initial decision-making aid.

| Feature | Financing | Leasing |

|---|---|---|

| Property | You become the owner with the last installment. | You are only the user, the vehicle remains the property of the lessor. |

| Monthly costs | The installments are often higher because the entire value is financed. | The installments are usually lower, as only the loss in value is paid for. |

| Flexibility | Rather low; an early sale can prove complicated. | Very high; simply switch to a new model at the end of the contract. |

| Freedom of use | Completely unlimited. No mileage limits or regulations for conversions. | Limited by contractually agreed mileage and condition. |

| Responsibility | You bear full responsibility for maintenance, repairs and depreciation. | Less responsibility; service packages can often be booked or are even included. |

| End of contract | The vehicle is yours. You can keep it, sell it or give it away. | You return the vehicle. Any additional payments for damage or extra mileage. |

This overview should serve as a kind of compass for the more detailed comparisons that we have prepared for you in the following sections. If you would like to delve even deeper into the world of credit options, you will find valuable further information in our articles on the subject of financing. You will then be well equipped to make an informed decision that is right for you.

A closer look at the key differences

So, the basics are clear. But now let’s get into the details, because this is where the wheat is separated from the chaff. The decision between financing and leasing is often determined by little things that seem inconspicuous at first glance, but can end up costing you a lot of money or throw your plans overboard.

The question “Financing or leasing, which is better?” cannot be answered in general terms. It all depends on what is important to you. To find out, we need to look not only at the monthly rate, but also at the overall package of ownership, costs and flexibility.

Who really owns the car? The question of ownership and freedom

The most fundamental difference, which affects everything else, is the question of ownership. With financing, you own the vehicle bit by bit. Each installment you pay is like another building block of your property until it is completely yours after the last payment.

And what does that mean in practice? Absolute freedom.

- No mileage restrictions: you can drive wherever and as often as you like. Nobody counts the kilometers.

- Don’t worry about the residual value: Sure, depreciation is your concern. But in the end, you don’t have to worry about whether a small dent or scratch will lead to expensive deductions.

- Your car, your rules: Fancy new rims, a different color or a technical upgrade? Go ahead! It’s your property, you can customize it however you like.

The world looks different with leasing. Here you are basically just the lessee. You pay to use the car for a certain period of time. Although this relieves you of responsibility, it also restricts your freedom considerably.

The cost structure: What is the bottom line?

A low leasing rate on an advertising poster looks great, of course. But it is often only half the truth. To make a really fair comparison, we need to look at all the items.

With financing, usually a classic installment loan, the calculation is quite simple: there is the purchase price, a possible down payment, the loan amount, interest and the monthly installment. In the case of balloon financing, there is also a large final installment at the end, which pushes down the monthly payments. If you want to delve deeper into the topic, you can find everything you need to know about installment loans in our guide everything you need to know about installment loans.

The leasing rate is a more complex structure. It is made up of various parts:

- The expected loss in value of the car

- Administrative costs of the leasing company

- An interest component and, of course, the profit margin

In addition, there are often costs lurking that only come to light when the vehicle is returned. These can be additional payments for every excess kilometer driven or deductions for signs of use that go beyond the “normal”.

At first glance, leasing often seems cheaper because you only pay for the depreciation. Financing seems more expensive because you are paying off the entire value of the vehicle – but at the end of the day you get a tangible return.

Current figures show how popular leasing is. A study from 2024 shows that lessees in Germany prefer contracts over 24 months with 10,000 kilometers per year. Although the average gross list price of the cars climbed to 47,088 euros, the installments fell to an average of 295 euros. Particularly interesting: 58 percent of the contracts were concluded by private individuals, who paid an average of just 224 euros per month. You can find more exciting insights in the leasing trends on leasingmarkt.de.

Flexibility at the end of the contract – blessing or curse?

This is where leasing shines: at the end of the term, you simply return the car and, if you wish, step straight into a brand new model. Perfect for anyone who always wants to drive the latest car and doesn’t want to deal with the hassle of reselling it.

But this convenience comes at a price. Returning the vehicle is the most critical moment of the entire contract. Every scratch is scrutinized, and high additional payments are unfortunately not uncommon.

Financing offers a different kind of flexibility. As soon as the last installment is paid, the car is yours. You have full control: continue to drive it, sell it privately or trade it in as a deposit for the next owner. The proceeds from the sale are entirely yours. You bear the sales risk, but you also determine the rules of the game.

When leasing or financing is worthwhile for you

There is no general answer to the question of whether leasing or financing is the better option. The right decision depends very much on your personal situation: Are you a private individual with individual wishes or an entrepreneur who needs to think strategically and fiscally above all else? Both methods are absolutely justified, but serve completely different needs.

For private individuals, the choice is often a very personal, sometimes even emotional matter. In business, on the other hand, it is a hard-nosed business calculation. It’s all about liquidity, balance sheet ratios and clever optimization of the tax burden. Let’s take a look at the two scenarios separately to provide some real clarity.

Financing or leasing as a private individual

When you are faced with this decision as a private customer, everything usually revolves around the central question: ownership or use? The desire to truly own a car or other item is an important factor for many.

Financing is the classic route to ownership. It is just right for you if you:

- Think long-term: You want to drive your car for many years, far beyond the typical three to four years of a leasing contract.

- Love your independence: No mileage limits, no worries about minor scratches that can quickly become expensive when you return your lease – you’re your own boss.

- Appreciate individuality: Would you like to customize your vehicle to your heart’s content? New rims, a special wrap or technical upgrades are no problem for your property.

Leasing, on the other hand, comes into its own when your priorities are flexibility and absolutely calculable costs. It is the perfect choice if you:

- regularly want to drive the latest new thing: They love the smell of a new car and always want to be technologically up to date.

- Appreciate planning security: Fixed monthly installments, often combined with service packages, give you full cost control. No nasty surprises.

- do not want to worry about reselling the car: At the end of the term, you simply return the car and choose the next one. You save yourself the stress and risk of a private sale.

So the crux of the matter is really the question of ownership. For many, the feeling that the car belongs to them is priceless. Others appreciate the freedom of leasing, precisely because they are aware of how much of a burden ownership can be. In the end, it’s a personal trade-off between the freedom of ownership and the convenience of pure use. If you decide to buy, you will find in our overview of various car loans for useful information on suitable financing models.

Financing or leasing for companies and the self-employed

For tradespeople, the self-employed and companies, the focus has shifted completely. It is not emotions that count here, but hard facts from business management. The decision between financing and leasing has a direct and tangible impact on liquidity, the balance sheet and the tax burden.

For companies, leasing is often more than just a financing alternative; it is a strategic instrument for managing liquidity and optimizing the balance sheet structure.

For most companies, leasing is simply the smarter choice. The monthly leasing installments can be immediately and fully deducted as operating expenses, which directly reduces the tax burden. Because the vehicle is not included in the company’s fixed assets, the balance sheet remains lean. This improves the equity ratio and therefore often also the creditworthiness with banks.

Financing, on the other hand, means that the vehicle must be capitalized as an asset in the balance sheet. It is then depreciated over its official useful life. This means that you can only deduct the annual depreciation (AfA) and the interest on the loan – not the entire installment. This ties up capital unnecessarily and inflates the balance sheet.

Here is a direct comparison of the most important points for companies:

| Aspect | Leasing for companies | Financing for companies |

|---|---|---|

| Tax treatment | Installments are immediately and fully deductible as operating expenses. | Only depreciation and interest are deductible. |

| Balance sheet impact | Balance sheet neutral; the vehicle does not appear under fixed assets. | The vehicle is capitalized; the balance sheet total increases. |

| Liquidity | Protects liquidity as there is no high purchase price. | Ties up capital or requires a loan to be taken out. |

| Plannability | Fixed, easily calculable monthly costs. | Costs can also be planned, but the balance sheet burden is higher. |

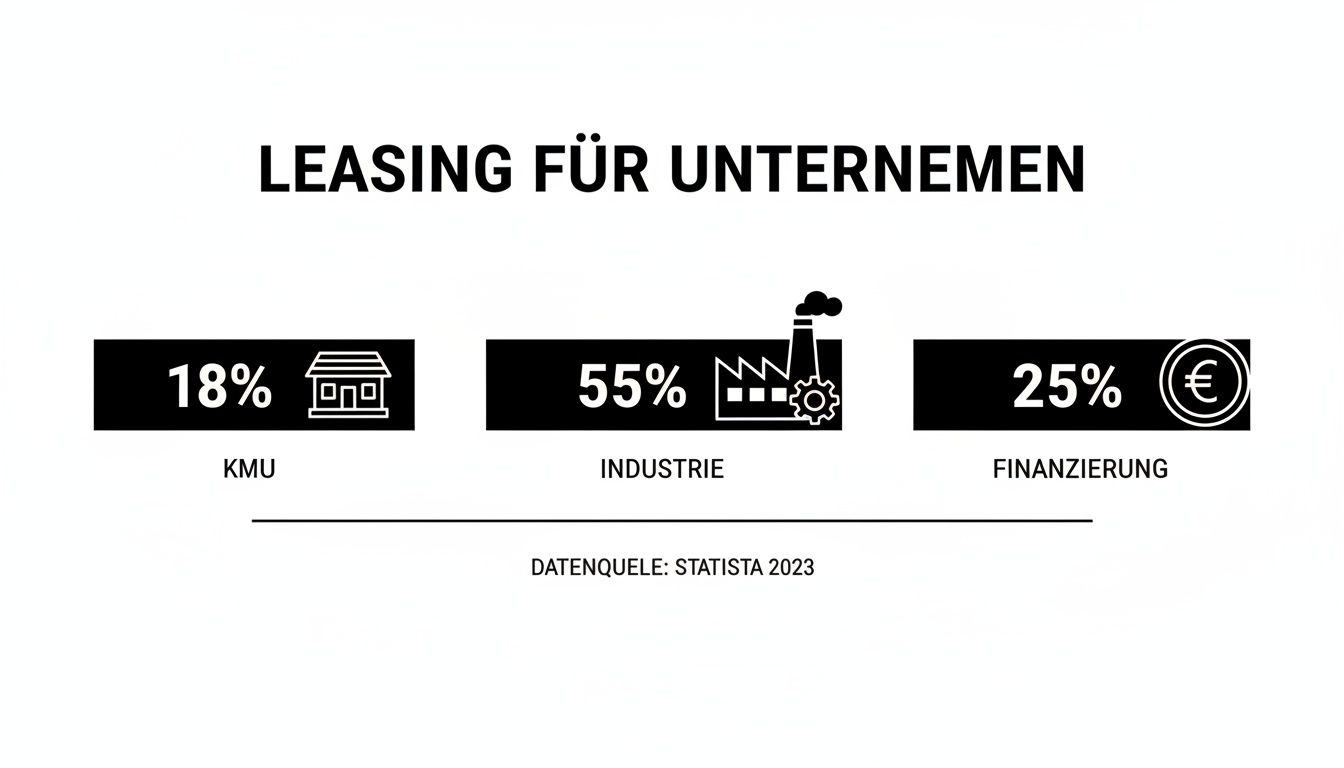

The importance of leasing for the German economy should not be underestimated. A KfW study has shown that one in four euros invested by small and medium-sized enterprises (SMEs) flows through leasing – that is an impressive 61 billion euros. While only 28 percent of SMEs use traditional bank loans, as many as 55 percent of companies with over 50 employees use leasing. It is a real stabilizer for investments because it avoids high one-off payments and protects liquidity.

A practical cost comparison with examples

Theory is a good thing, but at the end of the day, numbers speak the clearest language. To really answer the question “Financing or leasing, which is better?”, let’s leave the gray theory behind and dive right into the practice. We’ll calculate two very specific scenarios for a typical mid-range car with a purchase price of €35,000 – one as a classic financing arrangement and one as a leasing contract.

For our comparison, we assume an identical term of 36 months and an annual mileage of 15,000 kilometers. This ensures that we really are comparing apples with apples and that you get a realistic feeling for the financial burden.

Scenario 1: Traditional financing

Imagine you decide to buy a car. You make a down payment of €5,000 and finance the remaining €30,000 with a car loan. Assuming an effective annual interest rate of 5.0%, this results in a monthly installment of around €899 over a term of 36 months.

The total costs are then made up as follows:

- Down payment: € 5,000

- Sum of the installments (36 x € 899): 32.364 €

- Total payment for the vehicle: € 37,364

At the end of the three years, the car is yours. Let’s assume that the residual value of the car after this time is still 50% of the new price, i.e. a realistic €17,500. Your actual financial outlay – i.e. the loss in value plus the interest costs – therefore amounts to €19,864 (€37,364 – €17,500).

Scenario 2: The leasing contract

And now to leasing. Here, often no or only a small down payment is required. Let’s assume a one-off special payment of €2,000 to keep the monthly installments attractive. A typical leasing offer for this vehicle could be a monthly rate of €350.

The calculation over 36 months looks quite different here:

- Special leasing payment: € 2,000

- Sum of the installments (36 x € 350): 12.600 €

- Total payment for pure use: € 14,600

At the end of the contract, you simply return the car. The loss in value is already factored into the installments and is therefore no longer your problem. At first glance, of course, this seems much cheaper. But caution is advised: Additional costs for extra mileage or damage on return are not taken into account here.

The decisive difference lies in the result: with financing, you have an asset of €17,500 in the garage after three years. With leasing, you may have spent less, but you will end up empty-handed.

Cost comparison over 3 years for a mid-range car

In order to make a fair decision, we need to directly compare the total costs and the actual expenditure. The following table summarizes our calculation example and shows where the money goes.

| Cost point | Financing (example) | Leasing (example) |

|---|---|---|

| Down payment/special payment | 5.000 € | 2.000 € |

| Monthly installment | 899 € | 350 € |

| Total payment (36 months) | 37.364 € | 14.600 € |

| Remaining vehicle value | 17.500 € | 0 € |

| Real expense (loss of value + costs) | 19.864 € | 14.600 € |

In this example, leasing appears to be over €5,000 cheaper. However, this comparison is somewhat misleading as it completely ignores the freedom of ownership and potential follow-up costs of leasing. If you sell the financed car after three years, the proceeds are yours. With leasing, a careless return of the vehicle can quickly wipe out the initial savings.

Nevertheless, the popularity of leasing remains unbroken on the car market. Current data shows that almost half of all new registrations(48.4%) in Germany are leased or financed by installment plan. The total leasing volume for passenger cars amounted to an impressive 50.14 billion euros. This underlines how much many people and companies appreciate flexible rates without the burden of ownership.

This infographic shows impressively how much leasing is used by companies in particular.

The figures make it clear that leasing is a key strategic instrument, especially for larger companies, to keep their vehicle fleets modern and their balance sheets lean.

Ultimately, you need to weigh up what is more important to you personally: the potentially lower overall cost and convenience of leasing, or the freedom and long-term value of ownership through financing. If you’re considering the finance route, it’s worth taking a close look at the terms. You can also read our guide on how to find the best deal with a loan comparison.

Your personal checklist: Which path is right for you?

Now you have the facts, figures and sample calculations on the table. But the crucial question – financing or leasing – can only be answered if you take an honest look at your own needs. This checklist is designed to help you gain clarity.

Take a moment to do this. Go through the following questions point by point. Your answers will show you the way, because it’s all about making a decision that you’ll be happy with for years to come.

Question 1: What does ownership mean to you?

That is the crucial question in this decision. For many, the thought of holding something of real value in their hands at the end of the term – be it a car, a machine or an expensive IT system – is simply incredibly important.

- When ownership counts (towards financing): You nod and think: “Sure, in the end I want the car to be mine. I want to be able to keep it, sell it or maybe even pass it on.” Then financing is clearly the way to go. This is about building up assets.

- When the focus is on utility (towards leasing): They tend to think: “Ownership is just ballast that loses value. I just always want to drive the latest model without worrying about all the rest.” If this is your attitude, then leasing suits you perfectly.

Question 2: How well can you plan your future?

Realism is required here. How well can you estimate how you will use the car or machine over the next few years? Unexpected costs or even your freedom often depend on this.

In leasing, mileage is the most common reason for hefty additional payments. An honest assessment of your driving habits will save you from a nasty surprise at the end of the contract.

- Mileage: Do you cover a similar distance every year, or could a new job or a move throw everything out of kilter? Financing gives you complete freedom here. With leasing, on the other hand, a precise calculation is worth its weight in gold.

- Handling and wear and tear: Are you the meticulous type, or is a scratch no problem for you? With a financed car, you decide for yourself what constitutes normal wear and tear. In the case of a leased vehicle, this is ultimately determined by an expert when the car is returned.

Question 3: How important is flexibility to you?

Your life planning is a crucial point. Do you want to make a longer commitment or would you prefer to reshuffle the cards every few years?

- Fancy something new: Do you love technical progress and want to drive the latest model every two to three years without having to worry about reselling it? This is precisely the core promise of leasing.

- Security and longevity: Do you see your car as a loyal companion for many years and don’t want to have to make a new decision as soon as the contract expires? Then financing gives you the stability you are looking for.

Once you have thought through these points, a clear picture should slowly emerge. There is no blanket “better” or “worse” – there is only a “more suitable” or “less suitable” for your own personal situation.

If financing is the best option for you, the next step is to secure the best conditions. Find out in our guide which tips and tricks for a successful loan application really help.

Financing or leasing: what else you should know

Now that we have shed light on the major differences between financing and leasing, detailed questions often arise that can be crucial in everyday life. Finally, let’s clarify some of the most frequently asked questions that we encounter time and again in practice.

These answers from the field should take away the last uncertainties and help you to make a decision that feels right in the long term.

How do financing and leasing affect my credit rating?

Both methods – financing and leasing – leave traces at credit agencies such as SCHUFA, but the type of trace is different. A classic loan for financing is entered there as a normal liability. If you always pay your installments on time, this can even have a positive effect on your score. This proves that you are a reliable contractual partner.

Although a leasing contract is also reported, it is weighted differently. It counts more like a regular payment obligation, comparable to rent. As you are not acquiring property, a leasing contract generally places less of a burden on your credit rating than a large credit line.

What if I want to get out of the contract earlier?

Honestly? An early exit is a tricky and usually expensive affair with both models. With financing, you can of course repay the loan in full at any time. However, the bank then almost always charges a prepayment penalty to compensate for the interest it has lost.

You cannot simply terminate a leasing contract. The most common, but often laborious solution is to take over the lease. This means you have to find someone who will take over your contract under the existing conditions. However, whether this works always depends on the agreement of the lessor – there is no guarantee.

Whether you finance or lease: You are entering into a long-term commitment. There is no easy emergency exit with either option. You should bear this in mind from the outset.

What should I look out for in the “hidden” costs?

The small print can quickly turn a low rate into an expensive affair. With financing, the whole thing is still quite manageable. Here you should pay attention to possible processing fees and the exact conditions of optional residual debt insurance.

With leasing, the list of potential pitfalls is longer and requires a watchful eye:

- Extra kilometers: Every kilometer you drive more than agreed will end up costing you dearly. Calculate realistically here!

- Compensation for reduced value: scratches, dents or stains that go beyond normal signs of use can lead to hefty additional payments on return.

- Insurance requirements: Lessors often stipulate expensive fully comprehensive insurance, sometimes even with a fixed garage commitment.

So it really is worth going through the contract details point by point to avoid a rude awakening at the end.

Have you weighed up all the facts and flexible financing seems to be the right option for you? Finanz-Fox is here to help you find the right loan for your project. Our transparent loan calculator lets you run through various options so that you can discover the best offer for your situation. Start the comparison now and take a big step towards your plans.

Find your ideal loan now at https://www.finanz-fox.de.

1,365 Responses

where to buy prednisone uk: anti-inflammatory medication online – prednisone 2.5 tablet

prednisone 20mg price in india: SteriCare Pharmacy – prednisone prescription drug

vet pharmacy online: pet drugs online – Paw Trust Meds

canadian online pharmacy reviews: canadian drug stores – canadian pharmacy

Global India Pharmacy: Global India Pharmacy – Global India Pharmacy

https://northaccessrx.com/otc-meds.html# canadian pharmacy checker

canadian pharmacies that deliver to the us: is canadian pharmacy legit – canadianpharmacyworld

best canadian pharmacy online: canadian pharmacy ed medications – canadian pharmacy cheap

https://pawtrustmeds.com/# Paw Trust Meds

pet meds without vet prescription canada: NorthAccess Rx – legitimate canadian online pharmacies

indian pharmacy paypal: Global India Pharmacy – top 10 pharmacies in india

Paw Trust Meds: pet prescriptions online – pet med

https://northaccessrx.com/ed-meds-guide.html# best rated canadian pharmacy

buy prescription drugs from india: cheapest online pharmacy india – mail order pharmacy india

canadian pharmacy 24: NorthAccess Rx – safe reliable canadian pharmacy

https://globalindiapharmacy.shop/# Online medicine home delivery

indian pharmacy paypal: online pharmacy india – Global India Pharmacy

Global India Pharmacy: Online medicine home delivery – Global India Pharmacy

https://northaccessrx.com/ed-meds-guide.html# safe canadian pharmacy

canadadrugpharmacy com: canadian pharmacy tampa – canadian pharmacy uk delivery

Global India Pharmacy: Global India Pharmacy – reputable indian online pharmacy

indian pharmacy: Global India Pharmacy – Global India Pharmacy

https://northaccessrx.com/antibiotics-guide.html# canadian pharmacy online ship to usa

Global India Pharmacy: indian pharmacy paypal – reputable indian pharmacies

reputable indian pharmacies: Global India Pharmacy – Global India Pharmacy

https://northaccessrx.com/depression-treatments.html# pet meds without vet prescription canada

https://northaccessrx.com/canadian-pharmacy-rating.html# canadian online drugs

canada drugstore pharmacy rx: legitimate canadian mail order pharmacy – onlinecanadianpharmacy 24

best canadian pharmacy online: NorthAccess Rx – canadian pharmacy sarasota

safe canadian pharmacies: canadian valley pharmacy – canadian online drugstore

http://globalindiapharmacy.com/# Global India Pharmacy

Paw Trust Meds: Paw Trust Meds – Paw Trust Meds

canadian pharmacy scam: canadian pharmacy online – canadian discount pharmacy

https://globalindiapharmacy.shop/# Global India Pharmacy

canada pharmacy: best online canadian pharmacy – canadian pharmacy antibiotics

https://pawtrustmeds.com/# discount pet meds

Global India Pharmacy: best india pharmacy – cheapest online pharmacy india

Global India Pharmacy: top 10 pharmacies in india – Global India Pharmacy

mail order pharmacy india: Global India Pharmacy – Global India Pharmacy

vipps canadian pharmacy: NorthAccess Rx – canada drugs online review

Paw Trust Meds: vet pharmacy online – Paw Trust Meds

my canadian pharmacy: safe online pharmacies in canada – recommended canadian pharmacies

https://northaccessrx.com/canadian-pharmacy-rating.html# the canadian drugstore

Global India Pharmacy: indian pharmacy online – mail order pharmacy india

best mail order pharmacy canada: online canadian pharmacy reviews – cross border pharmacy canada

canada pet meds: Paw Trust Meds – Paw Trust Meds

canadianpharmacyworld com: NorthAccess Rx – buy drugs from canada

Global India Pharmacy: Global India Pharmacy – cheapest online pharmacy india

Global India Pharmacy: Global India Pharmacy – reputable indian pharmacies

Global India Pharmacy: buy medicines online in india – Global India Pharmacy

Global India Pharmacy: reputable indian pharmacies – Global India Pharmacy

http://globalindiapharmacy.com/# Global India Pharmacy

Paw Trust Meds: dog medication online – Paw Trust Meds

Paw Trust Meds: Paw Trust Meds – pet rx

https://globalindiapharmacy.shop/# Global India Pharmacy

cheap canadian pharmacy online CivicMeds italian pharmacy online

world pharmacy india: indian pharmacy paypal – prices pharmacy

viagra canada: CoreBlue Health – CoreBlue Health

CoreBlue Health Cheapest Sildenafil online buy Viagra over the counter

https://civicmeds.com/# canadian pharmacy king reviews

https://civicmeds.com/# best canadian pharmacy

prescription drugs online: CivicMeds – reputable indian online pharmacy

canadian drug pharmacy: CivicMeds – pharmacy website india

Buy Cialis online VeritasCare VeritasCare

sildenafil 50 mg price: cheap viagra – Viagra generic over the counter

online pharmacy without scripts: top mail order pharmacies – discount pharmacy online

http://veritascarepharm.com/# Cialis 20mg price

Viagra Tablet price Sildenafil 100mg price Viagra online price

https://corebluehealth.shop/# viagra without prescription

best price for viagra 100mg: CoreBlue Health – CoreBlue Health

Cheap Cialis: VeritasCare – Buy Tadalafil 10mg

Sildenafil 100mg price Generic Viagra for sale CoreBlue Health

http://veritascarepharm.com/# buy cialis pill

specialty pharmacy: CivicMeds – trustworthy canadian pharmacy

VeritasCare: Buy Cialis online – VeritasCare

VeritasCare Generic Tadalafil 20mg price VeritasCare

Cialis 20mg price in USA: VeritasCare – Cialis over the counter

reputable canadian pharmacy: CivicMeds – online pharmacy in turkey

VeritasCare Cialis without a doctor prescription Buy Tadalafil 5mg

http://veritascarepharm.com/# VeritasCare

http://corebluehealth.com/# CoreBlue Health

CoreBlue Health: cheap viagra – CoreBlue Health

online pharmacy drop shipping: pharmacies in canada that ship to the us – online pharmacy usa

VeritasCare Generic Cialis price VeritasCare

https://civicmeds.shop/# cheapest pharmacy for prescriptions without insurance

Generic Viagra online: Sildenafil Citrate Tablets 100mg – generic sildenafil

VeritasCare: VeritasCare – Cialis over the counter

Buy Tadalafil 10mg Buy Tadalafil 10mg VeritasCare

http://civicmeds.com/# online pharmacy india

п»їcialis generic: Tadalafil Tablet – VeritasCare

Cheap Cialis: VeritasCare – Generic Cialis price

canadian pharmacy king reviews best canadian pharmacy best canadian pharmacy online

https://civicmeds.shop/# canadian pharmacy online cialis

canadian family pharmacy: best canadian pharmacy for cialis – online pharmacy discount code

canadian online pharmacy: pharmacy websites – top online pharmacy india

CoreBlue Health Cheap generic Viagra online CoreBlue Health

https://veritascarepharm.shop/# VeritasCare

sure save pharmacy: cialis canadian pharmacy – international pharmacy no prescription

VeritasCare: VeritasCare – Buy Tadalafil 10mg

CoreBlue Health Cheapest Sildenafil online Order Viagra 50 mg online

https://corebluehealth.shop/# over the counter sildenafil

buy cialis pill: Cheap Cialis – VeritasCare

Cheapest Sildenafil online: Viagra online price – CoreBlue Health

no rx needed pharmacy escrow pharmacy canada legit canadian pharmacy

https://civicmeds.com/# onlinecanadianpharmacy 24

safe canadian pharmacy: canadianpharmacymeds com – modafinil online pharmacy

VeritasCare: VeritasCare – Buy Tadalafil 20mg

http://civicmeds.com/# canadian pharmacy review

CoreBlue Health: CoreBlue Health – CoreBlue Health

VeritasCare: VeritasCare – VeritasCare

https://civicmeds.shop/# legit pharmacy websites

CoreBlue Health buy viagra here Cheap Sildenafil 100mg

CoreBlue Health: CoreBlue Health – CoreBlue Health

Viagra Tablet price: CoreBlue Health – CoreBlue Health

online pharmacy no prescription CivicMeds canadian pharmacy ed medications

http://corebluehealth.com/# CoreBlue Health

https://corebluehealth.shop/# Viagra tablet online

CoreBlue Health: buy viagra here – CoreBlue Health

Cialis 20mg price: VeritasCare – VeritasCare

Viagra generic over the counter Buy Viagra online cheap CoreBlue Health

no prescription pharmacy paypal: canadian pharmacy 24 com – indian pharmacy paypal

canadian pharmacy mall: CivicMeds – drugstore com online pharmacy prescription drugs

online pharmacy reviews canadian pharmacy review low cost online pharmacy

https://corebluehealth.com/# CoreBlue Health

http://civicmeds.com/# canadian pharmacy without prescription

24 hr pharmacy: canadian prescription pharmacy – pharmacy discount coupons

buy Viagra online: Viagra without a doctor prescription Canada – Buy Viagra online cheap

script pharmacy CivicMeds canada rx pharmacy

cheapest cialis: VeritasCare – VeritasCare

Tadalafil Tablet VeritasCare VeritasCare

VeritasCare: Buy Tadalafil 10mg – VeritasCare

CoreBlue Health Buy generic 100mg Viagra online buy Viagra online

humana online pharmacy: CivicMeds – humana online pharmacy

CoreBlue Health: Viagra online price – cheapest viagra

https://veritascarepharm.com/# VeritasCare

pharmacy in canada CivicMeds canadian pharmacy com

Viagra generic over the counter: CoreBlue Health – CoreBlue Health

canadian pharmacy online ship to usa: online canadian pharmacy coupon – canadian pharmacy 1 internet online drugstore

CoreBlue Health CoreBlue Health CoreBlue Health

legitimate canadian mail order pharmacy: pharmacy coupons – non prescription medicine pharmacy

top 10 pharmacies in india: legal canadian pharmacy online – canadian online pharmacy

https://corebluehealth.com/# CoreBlue Health

Tadalafil price VeritasCare VeritasCare

CoreBlue Health: CoreBlue Health – viagra canada

Sildenafil Citrate Tablets 100mg: CoreBlue Health – Generic Viagra online

Tadalafil price VeritasCare VeritasCare

my canadian pharmacy: CivicMeds – canadian pharmacy 365

https://civicmeds.com/# online pharmacy quick delivery

VeritasCare Buy Tadalafil 5mg buy cialis pill

CoreBlue Health Cheapest Sildenafil online CoreBlue Health

https://corebluehealth.com/# CoreBlue Health

http://civicmeds.com/# best australian online pharmacy

buy Viagra online Viagra tablet online generic sildenafil

CoreBlue Health generic sildenafil Cheapest Sildenafil online

https://veritascarepharm.shop/# VeritasCare

VeritasCare VeritasCare Tadalafil Tablet

http://civicmeds.com/# drugstore com online pharmacy prescription drugs

CoreBlue Health CoreBlue Health Order Viagra 50 mg online

http://veritascarepharm.com/# Buy Tadalafil 10mg

VeritasCare VeritasCare Generic Cialis price

CoreBlue Health Viagra without a doctor prescription Canada CoreBlue Health

http://veritascarepharm.com/# Buy Tadalafil 20mg

over the counter sildenafil cheapest viagra sildenafil online

Cialis over the counter: п»їcialis generic – VeritasCare

http://veritascarepharm.com/# VeritasCare

https://civicmeds.com/# canadian 24 hour pharmacy

bitcoin pharmacy online canadian pharmacy cheap canadian online pharmacy reviews

buy Viagra online: sildenafil online – CoreBlue Health

Tadalafil Tablet VeritasCare VeritasCare

reliable rx pharmacy: pharmacy store – tadalafil canadian pharmacy

https://veritascarepharm.shop/# VeritasCare

Cialis without a doctor prescription Generic Cialis price VeritasCare

generic sildenafil: buy Viagra online – CoreBlue Health

https://corebluehealth.com/# Cheap Sildenafil 100mg

CoreBlue Health CoreBlue Health CoreBlue Health

http://civicmeds.com/# escrow pharmacy online

VeritasCare: VeritasCare – VeritasCare

CoreBlue Health CoreBlue Health CoreBlue Health

canadian drugs pharmacy: pharmacy no prescription required – canadian pharmacy store

https://veritascarepharm.shop/# VeritasCare

generic sildenafil CoreBlue Health Buy Viagra online cheap

CoreBlue Health: CoreBlue Health – CoreBlue Health

canadian pharmacy meds best canadian online pharmacy reviews my canadian pharmacy reviews

https://civicmeds.shop/# canadapharmacyonline

buy cialis pill: VeritasCare – VeritasCare

https://corebluehealth.com/# CoreBlue Health

https://pinupazz.top/ pin-up online casino

пин ап пин ап казахстан

pin up pin-up oyunu

pin up pin up

https://pin-up-kz.space/ пин ап казино kz

https://pinupaz.online/ pin up

https://pinupazz.top/ pin-up online casino

pin-up pin-up online casino

https://pin-up-kz.space/ пин ап казино kz

pin up pin-up online casino

пин ап пин ап кз

https://pinupazz.top/ pin up az

pin-up pin up casino

https://pin-up-kz.space/ пин ап казахстан

https://pinupazz.top/ pin up

https://pinupaz.online/ pin up

пин ап пин ап кз

pin up pin up casino

пин ап пин ап кз

https://pinupazz.top/ pin up az

https://pinupaz.online/ pin up casino

https://pin-up-kz.space/ пин ап казино

https://pinupazz.top/ pin-up oyunu

https://pinupaz.online/ pin up az

https://pinupaz.online/ pin up casino

canadian pharmacy near me: SteadyMeds pharmacy – online canadian pharmacy reviews

http://formulinepharmacy.com/# no prescription needed pharmacy

AccessBridge: medications can i buy mexico – AccessBridge Pharmacy

AccessBridge: mexico prescriptions – AccessBridge

https://accessbridgepharmacy.shop/# purple pharmacy

best rx pharmacy online: pharmacy website india – shop medicine online

online pharmacy in mexico: pharmacy mexico – AccessBridge

https://steadymedspharmacy.com/# canadian drugstore online

worldwide pharmacy online Online medicine order best online pharmacy no prescription

SteadyMeds pharmacy: SteadyMeds – SteadyMeds

https://formulinepharmacy.shop/# new pharmacy online

best mail order pharmacy: india pharmacy mail order – online pharmacy without scripts

reputable online pharmacy no prescription: indian pharmacy online – medstore online pharmacy

https://accessbridgepharmacy.com/# AccessBridge

canadian pharmacy no scripts: SteadyMeds pharmacy – canadian pharmacies online

AccessBridge Pharmacy prescriptions from mexico AccessBridge

SteadyMeds pharmacy: SteadyMeds pharmacy – www canadianonlinepharmacy

http://formulinepharmacy.com/# overseas pharmacy no prescription

no rx needed pharmacy: FormuLine Pharmacy – top-rated online pharmacies

SteadyMeds pharmacy: SteadyMeds – SteadyMeds pharmacy

https://accessbridgepharmacy.com/# AccessBridge Pharmacy

secure medical online pharmacy: reputable indian online pharmacy – buy online medicine

https://accessbridgepharmacy.com/# farmacia mexicana online

https://formulinepharmacy.com/# online pharmacy no rx

best online pharmacy: best online pharmacy india – safe online pharmacies

buy drugs online: top 10 pharmacies in india – no prescription needed pharmacy

https://accessbridgepharmacy.shop/# mexican rx pharm

online pharmacy discount code: FormuLine Pharmacy – no prescription needed pharmacy

AccessBridge: order medicine from mexico – mexican pharmacy online

https://accessbridgepharmacy.shop/# AccessBridge

reputable overseas online pharmacies FormuLine Pharmacy top-rated online pharmacies

AccessBridge: AccessBridge – AccessBridge Pharmacy

http://accessbridgepharmacy.com/# AccessBridge

top online pharmacy: Online medicine home delivery – buy online medicine

http://accessbridgepharmacy.com/# pharmacy mexico city

mexican pharmacys: AccessBridge Pharmacy – AccessBridge

https://steadymedspharmacy.shop/# SteadyMeds

legitimate canadian pharmacy SteadyMeds SteadyMeds pharmacy

AccessBridge Pharmacy: mexican medicine – AccessBridge

no prescription pharmacy paypal: FormuLine Pharmacy – reliable online pharmacy

http://accessbridgepharmacy.com/# pharmacy in mexico online

http://steadymedspharmacy.com/# SteadyMeds pharmacy

reputable online pharmacy no prescription: top online pharmacy india – legitimate online pharmacy

http://accessbridgepharmacy.com/# AccessBridge

pharmacy in canada: SteadyMeds pharmacy – canadian pharmacy online ship to usa

https://steadymedspharmacy.shop/# adderall canadian pharmacy

top-rated online pharmacies: best india pharmacy – no script pharmacy

http://formulinepharmacy.com/# no prescription needed pharmacy

AccessBridge Pharmacy AccessBridge Pharmacy order meds from mexico

reliable online pharmacy: FormuLine Pharmacy – no prescription pharmacy paypal

https://formulinepharmacy.shop/# online drugs order

legitimate online pharmacy: п»їlegitimate online pharmacies india – legal online pharmacies in the us

https://accessbridgepharmacy.com/# AccessBridge

SteadyMeds: canadianpharmacy com – SteadyMeds pharmacy

https://formulinepharmacy.com/# best online pharmacy no prescription

AccessBridge: AccessBridge Pharmacy – AccessBridge

best mail order pharmacy FormuLine Pharmacy buy drugs online

https://formulinepharmacy.shop/# worldwide pharmacy

no prescription pharmacy paypal: FormuLine Pharmacy – best mail order pharmacy

http://accessbridgepharmacy.com/# mexico pet pharmacy

https://steadymedspharmacy.com/# SteadyMeds

mexican pharmacys: AccessBridge – mexican drug stores

https://steadymedspharmacy.shop/# legitimate canadian pharmacy

reliable online pharmacy: Online medicine order – new pharmacy online

online pharmacy without scripts: FormuLine Pharmacy – trusted online pharmacy

online pharmacy FormuLine Pharmacy overseas pharmacy no prescription

https://steadymedspharmacy.com/# SteadyMeds pharmacy

legitimate online pharmacy: FormuLine Pharmacy – new pharmacy online

https://steadymedspharmacy.com/# canadian neighbor pharmacy

best canadian pharmacy: real canadian pharmacy – SteadyMeds pharmacy

SteadyMeds pharmacy: SteadyMeds – SteadyMeds

AccessBridge Pharmacy AccessBridge buy drugs online

https://accessbridgepharmacy.com/# AccessBridge

AccessBridge Pharmacy: AccessBridge Pharmacy – AccessBridge

international pharmacy: FormuLine Pharmacy – new pharmacy online

http://steadymedspharmacy.com/# my canadian pharmacy rx

AccessBridge: buying prescription drugs in mexico – AccessBridge Pharmacy

AccessBridge Pharmacy: AccessBridge Pharmacy – AccessBridge

https://steadymedspharmacy.shop/# SteadyMeds

AccessBridge Pharmacy: medicine mexico – AccessBridge Pharmacy

order from mexico: AccessBridge Pharmacy – pharmacy in mexico city

progreso, mexico pharmacy online: AccessBridge Pharmacy – pharmacies in mexico that ship to the us

https://edmedscoupon.shop/# ed medications cost

new pharmacy online: Pharm Rate – best mail order pharmacy

http://petcanadadirect.com/# pet meds official website

online pharmacy without scripts http://pharmrate.com/# Pharm Rate

Pet Canada Direct: Pet Canada Direct – online vet pharmacy

Pet Canada Direct online vet pharmacy Pet Canada Direct

legit online pharmacy: Pharm Rate – online pharmacy

http://pharmrate.com/# Pharm Rate

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

no rx needed pharmacy https://petcanadadirect.com/# pet meds for dogs

safe online pharmacies: best mail order pharmacy – Pharm Rate

https://pharmrate.shop/# Pharm Rate

п»їdog medication online: vet pharmacy online – Pet Canada Direct

buy ed meds Ed Meds Coupon trustworthy online pharmacy

https://edmedscoupon.shop/# top rated ed pills

cost of ed meds: Ed Meds Coupon – legit online pharmacy

online vet pharmacy: Pet Canada Direct – п»їdog medication online

online pharmacies https://edmedscoupon.shop/# low cost ed pills

http://petcanadadirect.com/# Pet Canada Direct

Pet Canada Direct: pet med – pet meds online

express scripts mail order pharmacy: secure medical online pharmacy – pharmacy order online

order ed meds online buying erectile dysfunction pills online pharmacy online

online pharmacy no prescription needed http://pharmrate.com/# no prescription needed pharmacy

https://petcanadadirect.com/# Pet Canada Direct

Pet Canada Direct: pet rx – Pet Canada Direct

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

https://petcanadadirect.shop/# dog prescriptions online

reliable online pharmacy: pharmacy online – Pharm Rate

where to buy ed pills: what is the cheapest ed medication – overseas pharmacy no prescription

worldwide pharmacy https://edmedscoupon.shop/# top rated ed pills

Pharm Rate pharmacy online Pharm Rate

http://edmedscoupon.com/# pills for erectile dysfunction online

pet pharmacy online: Pet Canada Direct – Pet Canada Direct

Pharm Rate: Pharm Rate – Pharm Rate

https://petcanadadirect.com/# dog prescriptions online

pharmacy no prescription required http://petcanadadirect.com/# canada pet meds

online pharmacies: medicine online – Pharm Rate

order ed pills online: where can i get ed pills – online pharmacy no prescription

Pharm Rate legal online pharmacy medstore online pharmacy

dog prescriptions online: Pet Canada Direct – vet pharmacy

ed drugs online: Ed Meds Coupon – online drugs order

top-rated online pharmacies http://pharmrate.com/# online pharmacy without scripts

https://pharmrate.shop/# express scripts mail order pharmacy

cheapest ed online: Ed Meds Coupon – secure medical online pharmacy

shop medicine online: Pharm Rate – worldwide pharmacy

over the counter antibiotics over the counter antibiotics over the counter antibiotics

https://stromectol.reviews/# ivermectin 12

pcos semaglutide: semaglutide life – online pharmacy no rx

https://stromectol.reviews/# stromectol reviews

best compounding pharmacy for semaglutide: semaglutide max dose – reputable overseas online pharmacies

https://antibiotics.cheap/# antibiotics cheap

stromectol reviews: ivermectin gel – stromectol reviews

To save money on prescriptions: canadian online pharmacy hiv meds – report any suspicious activity

https://stromectol.reviews/# stromectol tab 3mg

how to qualify for semaglutide rybelsus дёж–‡ 1mg semaglutide

antibiotics for uti over the counter: otc medicine – cheap antibiotics

https://semaglutide.life/# rybelsus online pharmacy

over the counter antibiotics: buy doxycycline antibiotics – over the counter antibiotics

stromectol usa: stromectol coronavirus – ivermectin gel

https://stromectol.reviews/# stromectol reviews

https://stromectol.reviews/# stromectol reviews

semaglutide drugs: semaglutide life – trustworthy online pharmacy

rybelsus malaysia price semaglutide life semaglutide online no insurance

semaglutide doses for weight loss: generic rybelsus cost – buy online medicine

https://stromectol.reviews/# stromectol reviews

reviews on rybelsus: semaglutide life – legitimate online pharmacy

https://stromectol.reviews/# ivermectin price usa

https://antibiotics.cheap/# over the counter antibiotics

stromectol reviews: where to buy stromectol online – ivermectin gel

pros and cons of semaglutide: what is better semaglutide or tirzepatide – shop medicine online

stromectol cost stromectol reviews buy stromectol

https://semaglutide.life/# semaglutide and hair loss

https://antibiotics.cheap/# antibiotics

over the counter antibiotics: uti antibiotics online – cheap antibiotics

https://antibiotics.cheap/# over the counter antibiotics

stromectol coronavirus: ivermectin oral solution – ivermectin 50ml

stromectol order online: ivermectin 1mg – ivermectin buy australia

https://semaglutide.life/# can semaglutide cause anxiety

https://semaglutide.life/# ozempic vs compounded semaglutide

over the counter antibiotics: antibiotics cheap – antibiotics cheap

ivermectin coronavirus stromectol 0.5 mg stromectol reviews

stromectol reviews: stromectol reviews – purchase ivermectin

https://antibiotics.cheap/# get antibiotics without seeing a doctor

stromectol reviews: ivermectin oral solution – stromectol tab 3mg

https://antibiotics.cheap/# over the counter antibiotics

ivermectin new zealand: ivermectin 8000 – ivermectin 1 cream

https://semaglutide.life/# does rybelsus cause nausea

can you take semaglutide a day early: semaglutide life – foreign online pharmacy

buy amoxicillin antibiotic antibiotics cheap cheap antibiotics

antibiotics cheap: over the counter antibiotics – get antibiotics without seeing a doctor

https://semaglutide.life/# buy semaglutide online

https://semaglutide.life/# switching from tirzepatide to semaglutide

antibiotics cheap: over the counter antibiotics – generic antibiotics online cheap

antibiotics online prescription: over the counter antibiotics – over the counter antibiotics

https://antibiotics.cheap/# over the counter antibiotics

over the counter antibiotics: antibiotics cheap – antibiotics for uti over the counter

rybelsus 3 mg para bajar de peso what does rybelsus cost can you buy rybelsus over the counter

https://stromectol.reviews/# stromectol reviews

side effects of rybelsus 7 mg: do semaglutide tablets work – international pharmacy

https://semaglutide.life/# cost of rybelsus vs ozempic

stromectol reviews: ivermectin 2mg – stromectol reviews

stromectol covid 19: stromectol reviews – stromectol reviews

https://antibiotics.cheap/# antibiotics cheap

semaglutide buy: weight loss pill rybelsus – online pharmacy without scripts

https://stromectol.reviews/# stromectol reviews

stromectol reviews ivermectin lotion stromectol reviews

stromectol reviews: stromectol reviews – stromectol reviews

https://stromectol.reviews/# stromectol coronavirus

rybelsus without diabetes: semaglutide life – online pharmacy no prescription needed

https://semaglutide.life/# best alcohol on semaglutide

order semaglutide online: semaglutide life – shop medicine online

https://antibiotics.cheap/# over the counter antibiotics

stromectol reviews: stromectol reviews – stromectol reviews

how to open rybelsus bottle cap semaglutide life symptoms of semaglutide

stromectol tablets buy online: ivermectin 10 mg – stromectol reviews

https://semaglutide.life/# levity semaglutide

stromectol reviews: stromectol reviews – ivermectin 3 mg tablet dosage

https://antibiotics.cheap/# over the counter antibiotics

stromectol reviews: generic ivermectin for humans – ivermectin 6mg

https://semaglutide.life/# semaglutide 5mg/ml dosage chart

over the counter antibiotics: buy antibiotics online – antibiotics for uti

https://stromectol.reviews/# stromectol reviews

ivermectin tablets: ivermectin 1mg – stromectol reviews

https://semaglutide.life/# compounded semaglutide expiration

generic ivermectin cream: ivermectin 3 mg tablet dosage – stromectol reviews

over the counter antibiotics: Over the counter antibiotics pills – antibiotics cheap

https://stromectol.reviews/# ivermectin uk coronavirus

over the counter antibiotics: antibiotics cheap – antibiotics cheap

https://semaglutide.life/# rybelsus generic

antibiotics cheap antibiotics cheap over the counter antibiotics

over the counter antibiotics: antibiotics cheap – antibiotics

https://antibiotics.cheap/# otc antibiotics

buy ivermectin for humans uk: ivermectin 500ml – stromectol ivermectin

stromectol reviews: cost of ivermectin medicine – ivermectin uk

https://antibiotics.cheap/# antibiotics online pharmacy

https://semaglutide.life/# what not to eat on semaglutide

Canadian Tabs: canadian pharmacies online – Canadian Tabs

online pharmacy india: Indian Meds Delivery – online pharmacy no rx

online shopping pharmacy india reputable indian pharmacies online pharmacy no prescription needed

https://indianmedsdelivery.xyz/# best online pharmacy india

Canadian Tabs: canadian pharmacy 1 internet online drugstore – pet meds without vet prescription canada

https://mexicanpharm.xyz/# Mexican Pharm

my canadian pharmacy: buying drugs from canada – Canadian Tabs

https://canadiantabs.xyz/# canadian pharmacy review

canadian pharmacy no rx needed: Canadian Tabs – Canadian Tabs

Canadian Tabs: best canadian pharmacy – canadian pharmacy no scripts

world pharmacy india Indian Meds Delivery top-rated online pharmacies

https://mexicanpharm.com/# mexican drugstore

https://indianmedsdelivery.xyz/# indian pharmacies safe

canadadrugpharmacy com: cheapest pharmacy canada – onlinecanadianpharmacy 24

indian pharmacies safe: Indian Meds Delivery – express scripts mail order pharmacy

https://indianmedsdelivery.com/# cheapest online pharmacy india

online pharmacy india: Indian Meds Delivery – legit online pharmacy

https://indianmedsdelivery.xyz/# best india pharmacy

Canadian Tabs: canada drugs online review – pet meds without vet prescription canada

buy prescription drugs from india Indian Meds Delivery reputable overseas online pharmacies

https://mexicanpharm.xyz/# Mexican Pharm

Mexican Pharm: mexico pharmacy order online – Mexican Pharm

india online pharmacy: best online pharmacy india – pharmacy websites

https://canadiantabs.com/# canadian pharmacy scam

india online pharmacy: indian pharmacy online – no prescription pharmacy paypal

indian pharmacy online: Indian Meds Delivery – legitimate online pharmacy

https://canadiantabs.xyz/# Canadian Tabs

Canadian Tabs Canadian Tabs pharmacy com canada

reliable canadian online pharmacy: Canadian Tabs – Canadian Tabs

Canadian Tabs: ordering drugs from canada – trusted canadian pharmacy

http://mexicanpharm.com/# Mexican Pharm

https://canadiantabs.com/# canadianpharmacy com

legit canadian online pharmacy: Canadian Tabs – canadian pharmacy com

top online pharmacy india: cheapest online pharmacy india – best rx pharmacy online

https://canadiantabs.com/# buy canadian drugs

medicine from mexico Mexican Pharm mexican meds

https://mexicanpharm.com/# Mexican Pharm

purple pharmacy online: best online mexican pharmacy – Mexican Pharm

Canadian Tabs: Canadian Tabs – canadian pharmacy online

https://indianmedsdelivery.xyz/# indian pharmacy

buy medicines online in india: Indian Meds Delivery – online pharmacy without prescription

canadian pharmacy mall: Canadian Tabs – certified canadian international pharmacy

https://canadiantabs.xyz/# canada pharmacy 24h

https://canadiantabs.xyz/# my canadian pharmacy reviews

reputable indian online pharmacy Indian Meds Delivery best mail order pharmacy

Canadian Tabs: Canadian Tabs – buy prescription drugs from canada cheap

indian pharmacy online: Indian Meds Delivery – no prescription pharmacy paypal

I have tried several, but: why choose canadian online pharmacy over local – never share unnecessary personal info

http://ivermectinfirst.com/# where to buy ivermectin pills

online drugs order: Online Pharm First – legit online pharmacy

https://ivermectinfirst.shop/# Ivermectin First

ivermectin pill cost: stromectol 3 mg dosage – ivermectin syrup

https://ivermectinfirst.com/# stromectol covid

reputable overseas online pharmacies Online Pharm First no prescription pharmacy paypal

pet meds for dogs: Vet Pharm First – Vet Pharm First

Vet Pharm First: best pet rx – Vet Pharm First

https://vetpharmfirst.shop/# Vet Pharm First

http://ivermectinfirst.com/# ivermectin 3mg pill

Ivermectin First: Ivermectin First – Ivermectin First

Ivermectin First: Ivermectin First – Ivermectin First

http://ivermectinfirst.com/# buy stromectol canada

ivermectin 50 mg cost of ivermectin ivermectin online

reputable overseas online pharmacies: international pharmacy – buy online medicine

https://onlinepharmfirst.com/# us pharmacy no prescription

Ivermectin First: stromectol medication – ivermectin cost

http://vetpharmfirst.com/# Vet Pharm First

reputable online pharmacy no prescription: Online Pharm First – online pharmacy

Ivermectin First: ivermectin gel – Ivermectin First

https://ivermectinfirst.shop/# ivermectin 6mg dosage

Vet Pharm First dog prescriptions online Vet Pharm First

Vet Pharm First: pet prescriptions online – Vet Pharm First

http://vetpharmfirst.com/# dog prescriptions online

best pet rx: Vet Pharm First – Vet Pharm First

worldwide pharmacy online: top-rated online pharmacies – pharmacy no prescription required

https://vetpharmfirst.shop/# Vet Pharm First

express scripts mail order pharmacy: Online Pharm First – pharmacy order online

http://onlinepharmfirst.com/# express scripts mail order pharmacy

legal online pharmacy no rx needed pharmacy shop medicine online

top-rated online pharmacies: Online Pharm First – best online pharmacy no prescription

https://vetpharmfirst.shop/# Vet Pharm First

pet med: canada pet meds – vet pharmacy

pharmacy no prescription required: Online Pharm First – online pharmacy no rx

https://onlinepharmfirst.com/# new pharmacy online

Vet Pharm First: best pet rx – Vet Pharm First

https://onlinepharmfirst.com/# pharmacy order online

Ivermectin First ivermectin 5 Ivermectin First

ivermectin 5 mg: buy ivermectin pills – Ivermectin First

https://vetpharmfirst.com/# Vet Pharm First

vet pharmacy online pet med canada pet meds

ivermectin usa price: Ivermectin First – Ivermectin First

https://onlinepharmfirst.shop/# best rx pharmacy online

Ivermectin First: Ivermectin First – ivermectin brand name

pet pharmacy online online pet pharmacy pet meds for dogs

stromectol cost Ivermectin First ivermectin 1 cream generic

http://ivermectinfirst.com/# Ivermectin First

shop medicine online: overseas pharmacy no prescription – overseas online pharmacy

https://vetpharmfirst.com/# vet pharmacy

pet rx Vet Pharm First pet drugs online

dog prescriptions online: Vet Pharm First – Vet Pharm First

http://vetpharmfirst.com/# dog prescriptions online

stromectol online canada stromectol where to buy Ivermectin First

canada pet meds: Vet Pharm First – pet drugs online

http://ivermectinfirst.com/# Ivermectin First

pet rx dog prescriptions online best pet rx

Ivermectin First: ivermectin pills – Ivermectin First

https://ivermectinfirst.shop/# Ivermectin First

online pharmacy no prescription needed: Online Pharm First – no prescription needed pharmacy

pet prescriptions online pet pharmacy pet pharmacy online

https://onlinepharmfirst.com/# reliable online pharmacy

medstore online pharmacy Online Pharm First online drugs order

https://ivermectinfirst.shop/# ivermectin 6

rybelsus heartburn semaglutide injections for weight loss legit online pharmacy

https://rybelsus.pro/# novo nordisk rybelsus coupon

Cheap Cialis Tadalafil Tablet Buy Tadalafil 10mg

https://cialis.sbs/# Tadalafil price

https://rybelsus.pro/# rybelsus tablets for weight loss

Generic Viagra for sale over the counter sildenafil Viagra without a doctor prescription Canada

semaglutide shelf life (rybelsus) how rybelsus works

https://viagra.onl/# best price for viagra 100mg

cheapest viagra cheap viagra over the counter sildenafil

Tadalafil price Buy Tadalafil 5mg Tadalafil price

https://cialis.sbs/# п»їcialis generic

https://viagra.onl/# Viagra without a doctor prescription Canada

Generic Viagra online Sildenafil 100mg price over the counter sildenafil

Buy generic 100mg Viagra online order viagra Viagra without a doctor prescription Canada

Cialis without a doctor prescription Cheap Cialis Buy Tadalafil 10mg

https://cialis.sbs/# Buy Cialis online

https://cialis.sbs/# Buy Cialis online

Buy Tadalafil 10mg п»їcialis generic Buy Cialis online

Шановні учасники! В інформаційну добу надзвичайно важливо мати доступ до перевірених джерел, а не тонути у фейках та поверхневих новинах. Я знайшов сайт, який вирішує цю проблему — він є каталогом перевірених українських ЗМІ. Там зібрані ресурси з різних регіонів та тематик: від аналітики Львова до наукових відкриттів та журналістських розслідувань. Додайте собі в закладки, щоб завжди бути в курсі подій з перевірених джерел на newandlostdpuie.space

https://viagra.onl/# Viagra Tablet price

https://cialis.sbs/# Cialis 20mg price in USA

Generic Tadalafil 20mg price Cialis 20mg price Tadalafil Tablet

buy Viagra over the counter Cheap Sildenafil 100mg Order Viagra 50 mg online

Buy Cialis online Cialis over the counter Generic Cialis without a doctor prescription

https://rybelsus.pro/# what if i miss a dose of rybelsus

Generic Cialis without a doctor prescription cheapest cialis п»їcialis generic

https://viagra.onl/# Cheap Viagra 100mg

Sildenafil Citrate Tablets 100mg Viagra Tablet price Buy Viagra online cheap

https://cialis.sbs/# cialis for sale

Viagra without a doctor prescription Canada Cheap Viagra 100mg cheap viagra

https://cialis.sbs/# п»їcialis generic

https://rybelsus.pro/# otc semaglutide

Buy Tadalafil 20mg cialis for sale Buy Tadalafil 5mg

Buy generic 100mg Viagra online Cheap generic Viagra online cheapest viagra

empower pharmacy lawsuit semaglutide foods to avoid on semaglutide international pharmacy

https://rybelsus.pro/# rybelsus 3 mg para bajar de peso

https://viagra.onl/# Viagra tablet online

Cheap generic Viagra online Viagra without a doctor prescription Canada Cheap Sildenafil 100mg

https://cialis.sbs/# Tadalafil Tablet

cialis generic Cialis over the counter Tadalafil Tablet

rybelsus 7 mg precio walmart rybelsus 7 mg precio walmart over the counter semaglutide

what is the highest dose of rybelsus rybelsus patent expiration legit online pharmacy

https://viagra.onl/# Cheap Viagra 100mg

https://cialis.sbs/# cheapest cialis

Viagra online price sildenafil 50 mg price Viagra without a doctor prescription Canada

what is semaglutide used for get semaglutide online medicine online order

https://cialis.sbs/# п»їcialis generic

https://rybelsus.pro/# can semaglutide cause diarrhea

how to get on semaglutide rybelsus 7mg price legit online pharmacy

semaglutide pros and cons rybelsus gastroparesis rybelsus effectiveness

https://viagra.onl/# buy Viagra over the counter

https://rybelsus.pro/# how to take rybelsus 3 mg

Generic Cialis price Tadalafil Tablet cialis generic

levity semaglutide rybelsus dosis п»їinternational drug mart

https://cialis.sbs/# cialis for sale

https://cialis.sbs/# cialis for sale

Cialis 20mg price in USA Cialis 20mg price in USA Tadalafil Tablet

generic sildenafil cheap viagra Viagra generic over the counter

Cialis over the counter Cialis without a doctor prescription Generic Cialis price

https://cialis.sbs/# buy cialis pill

best semaglutide for weight loss rybelsus 7mg price legal online pharmacy

https://viagra.onl/# Sildenafil 100mg price

https://rybelsus.pro/# rybelsus (semaglutide tablets)

how much weight can i lose on semaglutide best time of day to take semaglutide injection top online pharmacy

Buy Tadalafil 20mg Buy Tadalafil 5mg Buy Cialis online

https://rybelsus.pro/# semaglutide for weight loss near me

Cialis without a doctor prescription Cialis without a doctor prescription Tadalafil price

pusulabet resmi pusulabet güncel adres

https://casivipgiris.site# bahiscasino casino

bahiscasino resmi giriş: bahiscasino güncel

Generic Cialis without a doctor prescription Buy Cialis online Cheap Cialis

https://bestbetgiris.online# pusulabet resmi

https://bestbetgiris.online# pusulabet giriş

https://casivipgiris.site# bahiscasino güncel adres

legitimate canadian online pharmacies: Easy Canada Meds – Easy Canada Meds

canadian family pharmacy: Easy Canada Meds – trustworthy canadian pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

top 10 pharmacies in india mail order pharmacy india safe online pharmacies

online pharmacy india: online pharmacy india – legitimate online pharmacy

http://easymexmeds.com/# Easy Mex Meds

top 10 pharmacies in india: buy prescription drugs from india – legitimate online pharmacy

Easy Mex Meds order from mexico Easy Mex Meds

Easy Mex Meds: Easy Mex Meds – best mexican online pharmacy

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

Easy Mex Meds: Easy Mex Meds – pharmacy in mexico that ships to us

buy medicines online in india mail order pharmacy india no prescription needed pharmacy

mexican pharmacy near me: Easy Mex Meds – farmacia pharmacy mexico

best mexican online pharmacy: mexican drug store – Easy Mex Meds

https://easyindiameds.com/# п»їlegitimate online pharmacies india

mexican online pharmacy medication from mexico buying prescription drugs in mexico

reputable canadian pharmacy: Easy Canada Meds – Easy Canada Meds

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

Easy Canada Meds best canadian pharmacy online Easy Canada Meds

medications canada: Easy Canada Meds – Easy Canada Meds

mexican pharmacy what to buy: best mexican pharmacy online – pharmacy mexico city

online shopping pharmacy india: Easy India Meds – online pharmacies

affordable pharmacy mexican drug stores Easy Mex Meds

http://easymexmeds.com/# order meds from mexico

mail order pharmacy india: Easy India Meds – buy online medicine

top 10 pharmacies in india: indian pharmacy – reliable online pharmacy

Easy Canada Meds canadian drugs pharmacy Easy Canada Meds

Easy Canada Meds: Easy Canada Meds – pharmacy canadian

Easy Canada Meds: drugs from canada – Easy Canada Meds

indian pharmacies safe: reputable indian online pharmacy – trustworthy online pharmacy

canadian compounding pharmacy Easy Canada Meds canadian pharmacy 24 com

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

https://easyindiameds.shop/# pharmacy website india

canadian pharmacy oxycodone: Easy Canada Meds – Easy Canada Meds

cheapest online pharmacy india Easy India Meds trustworthy online pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

Easy Canada Meds: Easy Canada Meds – canadian compounding pharmacy

Easy Canada Meds canadian compounding pharmacy precription drugs from canada

mexico meds: reliable rx pharmacy – online pharmacy in mexico

my canadian pharmacy reviews: canadian pharmacy checker – pharmacy wholesalers canada

Easy Mex Meds: mexican online pharmacies – Easy Mex Meds

Easy Mex Meds Easy Mex Meds mexican rx

https://easycanadameds.com/# best online canadian pharmacy

Easy Mex Meds: tijuana pharmacy online – pharmacies in mexico

Online medicine order: india pharmacy – buy drugs online

mexican meds pharmacy delivery Easy Mex Meds

canadian pharmacy meds reviews: Easy Canada Meds – buying drugs from canada

pharmacy in mexico: Easy Mex Meds – Easy Mex Meds

Easy Mex Meds legitimate mexican pharmacy online Easy Mex Meds

best canadian online pharmacy: Easy Canada Meds – buy canadian drugs

Easy Canada Meds: Easy Canada Meds – cheap canadian pharmacy

indian pharmacy paypal Easy India Meds pharmacy order online

https://easyindiameds.com/# world pharmacy india

buy prescription drugs from india: buy prescription drugs from india – shop medicine online

top online pharmacy india: buy prescription drugs from india – medstore online pharmacy

Easy Mex Meds Easy Mex Meds best mexican pharmacy online

mail order pharmacy india: indian pharmacy paypal – legal online pharmacy

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

precription drugs from canada canadian mail order pharmacy the canadian drugstore

Easy Mex Meds: mexican pharmacy prices – reliable rx pharmacy

reputable indian online pharmacy: indianpharmacy com – overseas pharmacy no prescription

https://easymexmeds.com/# Easy Mex Meds

canadian pharmacy no rx needed canadian pharmacy sarasota adderall canadian pharmacy

india online pharmacy: cheapest online pharmacy india – express scripts mail order pharmacy

northern pharmacy canada: Easy Canada Meds – onlinecanadianpharmacy

www canadianonlinepharmacy canadian pharmacy world pharmacy in canada

Easy Canada Meds: cheapest pharmacy canada – Easy Canada Meds

Easy Canada Meds canada drug pharmacy is canadian pharmacy legit

indianpharmacy com: Easy India Meds – medicine online

mexican pharmacies near me: buying prescription drugs in mexico – Easy Mex Meds

Online medicine home delivery Easy India Meds no prescription needed pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

online pharmacies: mexico pharmacies – Easy Mex Meds

india pharmacy mail order Easy India Meds pharmacy no prescription required

mexican pharmacy menu: Easy Mex Meds – online drugs order

mexican mail order pharmacy: mexico medicine – Easy Mex Meds

mail order pharmacy india Easy India Meds pharmacy online

Easy Canada Meds: precription drugs from canada – Easy Canada Meds

https://easyindiameds.com/# best online pharmacy india

Easy Canada Meds: certified canadian pharmacy – Easy Canada Meds

Easy Mex Meds Easy Mex Meds Easy Mex Meds

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

best canadian pharmacy to order from: Easy Canada Meds – best online canadian pharmacy

canadianpharmacymeds canadian medications Easy Canada Meds

mexican online mail order pharmacy Easy Mex Meds Easy Mex Meds

Easy Canada Meds: Easy Canada Meds – pharmacy com canada

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

https://easymexmeds.com/# Easy Mex Meds

top 10 pharmacies in india Easy India Meds trusted online pharmacy

can i order online from a mexican pharmacy: online pharmacies – Easy Mex Meds

Easy Mex Meds: mexican online pharmacy wegovy – Easy Mex Meds

Easy Canada Meds canadian drugstore online canadapharmacyonline legit

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

Online medicine order: indian pharmacy online – top online pharmacy

https://easyindiameds.shop/# mail order pharmacy india

Easy Canada Meds canada pharmacy online website shopping Easy Canada Meds

top 10 pharmacies in india: Easy India Meds – best online pharmacy no prescription

mexico drug store online: mexico medicine – Easy Mex Meds

mail order pharmacy india Easy India Meds medicine online

indian pharmacy paypal: Easy India Meds – legal online pharmacies in the us

Easy Mex Meds: medications can i buy mexico – mexican medicine

Easy Mex Meds Easy Mex Meds Easy Mex Meds

Easy Canada Meds: Easy Canada Meds – the canadian drugstore

https://easycanadameds.shop/# Easy Canada Meds

Easy Mex Meds: legitimate mexican pharmacy online – Easy Mex Meds

Easy Canada Meds onlinecanadianpharmacy canadian pharmacy online

hydrocodone mexico pharmacy: Easy Mex Meds – mexican farmacia

pharmacy buy online medicine

Fresh Pharm 24 secure medical online pharmacy

https://freshpharm24.com/product/lipitor online pharmacy no rx

lipitor fresh pharm buy drugs online

Fresh Pharm online pharmacy without scripts

https://freshpharm24.com/product/stendra reliable online pharmacy

https://freshpharm24.com/product/viagra online pharmacy

generic levothroid medstore online pharmacy

pharmacy fresh pharm online pharmacy

pharmacy fresh pharm worldwide pharmacy

https://freshpharm24.com/ medicine online

viagra online pharmacy no rx

online pharmacy trustworthy online pharmacy

Fresh Pharm 24 secure medical online pharmacy

https://freshpharm24.com/product/priligy online drugs order

https://freshpharm24.com/product/norvasc medicine online

priligy online pharmacy without scripts

online pharmacy no rx needed pharmacy

https://freshpharm24.com/ buy drugs online

Fresh Pharm legit online pharmacy

Fresh Pharm online pharmacies

Fresh Pharm medicine online order

https://freshpharm24.com/ no prescription pharmacy paypal

https://freshpharm24.com/ trusted online pharmacy

pharmacy medicine online order

pharmacy medstore online pharmacy

https://freshpharm24.com/product/levothroid best rx pharmacy online

Fresh Pharm buy online medicine

https://freshpharm24.com/product/lipitor online pharmacy no prescription needed

https://freshpharm24.com/ reputable overseas online pharmacies

pharmacy overseas pharmacy no prescription

Fresh Pharm us pharmacy no prescription

https://freshpharm24.com/product/viagra online pharmacy discount code

Fresh Pharm top online pharmacy

Fresh Pharm 24 trustworthy online pharmacy

https://freshpharm24.com/product/stendra secure medical online pharmacy

Buy Tadalafil 20mg п»їcialis generic buy cialis pill

http://sildenafilvip.com/# Sildenafil Vip

https://cialisvip.com/# cialis for sale

stromectol cream ivermectin tablets ivermectin where to buy for humans

https://cialisvip.online/# Cialis 20mg price

https://sildenafilvip.shop/# over the counter sildenafil

Cheapest Sildenafil online Sildenafil Vip sildenafil 50 mg price

https://cialisvip.online/# Cialis Vip

https://cialisvip.com/# Cialis Vip

stromectol ireland stromectol Vip stromectol 3 mg

viagra canada Cheapest Sildenafil online sildenafil over the counter

https://stromectolvip.com/# stromectol xr

https://sildenafilvip.shop/# Sildenafil Vip

https://stromectolvip.com/# ivermectin tablets order

sildenafil 50 mg price Sildenafil Vip Viagra online price

http://sildenafilvip.com/# Sildenafil Vip

ivermectin 3mg tablets price stromectol Vip stromectol ivermectin

http://stromectolvip.com/# purchase stromectol online

Viagra tablet online Sildenafil Citrate Tablets 100mg viagra without prescription

https://cialisvip.com/# Tadalafil Tablet

https://stromectolvip.com/# buy ivermectin cream

buy stromectol online uk buy stromectol canada ivermectin generic name

https://stromectolvip.com/# stromectol 6 mg dosage

Buy Cialis online Cialis Vip Generic Cialis price

https://sildenafilvip.com/# over the counter sildenafil

ivermectin tablets order buy ivermectin cream cost of ivermectin 1% cream

http://cialisvip.com/# Generic Cialis without a doctor prescription

http://stromectolvip.com/# ivermectin topical

buy Viagra over the counter buy Viagra online Cheap generic Viagra

https://sildenafilvip.shop/# Sildenafil Vip

https://stromectolvip.com/# ivermectin 4 tablets price

ivermectin cost uk stromectol Vip stromectol buy

cialis for sale Cialis Vip Cialis without a doctor prescription

http://stromectolvip.com/# ivermectin 18mg

https://sildenafilvip.com/# Viagra online price

Viagra online price Buy generic 100mg Viagra online Cheap generic Viagra online

http://sildenafilvip.com/# viagra canada

stromectol stromectol Vip ivermectin 4

http://sildenafilvip.com/# Sildenafil Vip

stromectol pills ivermectin 250ml stromectol buy uk

Generic Tadalafil 20mg price Cialis Vip Tadalafil Tablet

http://sildenafilvip.com/# Sildenafil Vip

ivermectin oral stromectol Vip ivermectin 5

http://cialisvip.com/# Buy Cialis online

buy cialis pill Cialis Vip cheapest cialis

https://stromectolvip.com/# oral ivermectin cost

ivermectin lotion for lice stromectol uk cost of ivermectin 1% cream

Tadalafil price Cialis Vip Buy Tadalafil 5mg

https://stromectolvip.online/# stromectol pills

Tadalafil Tablet Cialis Vip Generic Cialis price

https://cialisvip.online/# Cialis Vip

ivermectin 6 mg tablets stromectol Vip ivermectin over the counter canada

http://stromectolvip.com/# ivermectin 80 mg

Generic Cialis price buy cialis pill buy cialis pill

Viagra tablet online sildenafil 50 mg price Buy generic 100mg Viagra online

https://sildenafilvip.shop/# viagra without prescription

Viagra online price Sildenafil Vip Cheap Sildenafil 100mg

http://stromectolvip.com/# stromectol ivermectin 3 mg

ivermectin generic cream ivermectin otc ivermectin iv

https://sildenafilvip.com/# Sildenafil Vip

cheap viagra Viagra online price best price for viagra 100mg

ivermectin cream canada cost stromectol uk buy ivermectin cost canada

https://sildenafilvip.com/# Sildenafil Vip

rybelsus副作用 glp-1 drugs for weight loss rybelsus not working

victoza delivery liraglutide online buy victoza online

https://victopharm.com/# new pharmacy online

cheap liraglutide LiraglutideGlp1 liraglutide pharmacy

https://liraglutideglp1.shop/# generic liraglutide

liraglutide price LiraglutideGlp1 buy victoza online

overseas pharmacy no prescription Victo Pharm online pharmacy discount code

why am i so tired on semaglutide glp 1 pills is there a generic for rybelsus

http://liraglutideglp1.com/# glp-1

cheap liraglutide victoza weight loss п»їbuy liraglutide

https://liraglutideglp1.shop/# victoza generic

rybelsus and surgery glp-1 drugs como tomar rybelsus

https://semaglutideglp1.com/# semaglutide and pancreatitis

us pharmacy no prescription top online pharmacy online pharmacy