Buying a car without a down payment – for many, this sounds almost too good to be true. Yet it is often the smartest solution to get behind the wheel immediately without having to spend your hard-saved money in one go. You simply finance the entire purchase price and keep your reserves free for other important things. This is not a lazy compromise, but a genuine instrument for greater financial flexibility.

Why it is sometimes wiser to keep your savings

Just imagine: You are standing in front of your dream car and could drive off immediately. Often this is not just a wish, but simply a necessity. The old car suddenly gives up the ghost, the family needs more space or the new job cannot be reached without a vehicle. At times like these, you simply can’t wait.

This is exactly where full financing comes into its own. Instead of putting your savings into a car that loses value from the first kilometer, you keep your money in your account. This leaves you with a reassuring cushion for unexpected repairs, your next vacation or a sensible investment.

No longer a niche product in Germany

This pragmatic approach is becoming increasingly popular. Financing without equity has long since become a popular option in Germany, especially when it comes to new cars. Although average new car prices have only risen slightly to €44,560 according to the DAT Report 2026, which analyzes market trends for 2025, more and more buyers are opting for this option. A study shows: 23 percent of new cars were leased privately – many of these offers come without any down payment at all, making it super easy to get started. You can also find more background information in our guide to car financing on autoflex24.de.

The decisive advantage is that you are able to act immediately. You don’t have to postpone your plans, but can react directly to new life circumstances.

So it’s not a question here of affording a car that you can’t actually afford. On the contrary: it is a strategic decision to make clever use of your own capital. Instead of tying it up in an asset that is constantly losing value, it remains flexibly available. The only important thing is that you are well informed beforehand and understand the conditions exactly. Then financing without a down payment turns from an emergency solution into a really smart decision that creates freedom and security.

Which financing models really work without a down payment

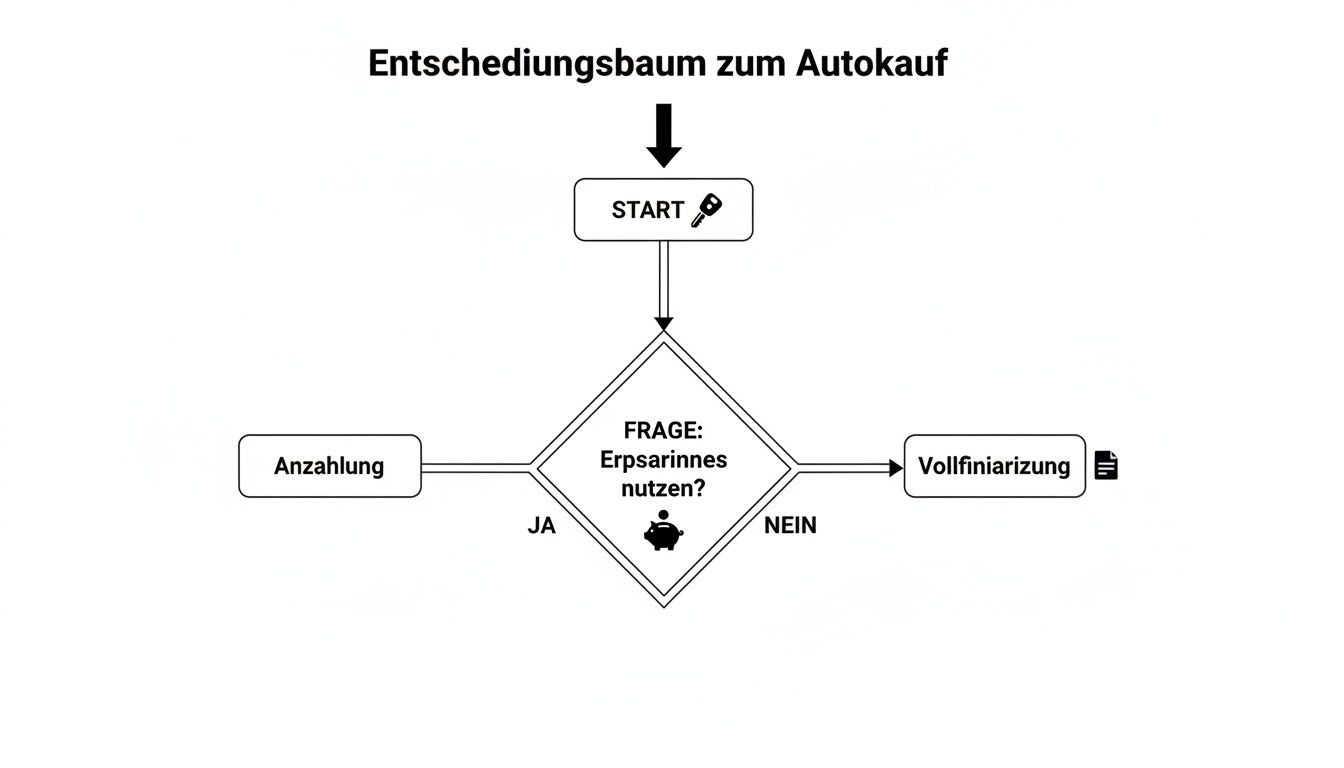

Would you like a new car but prefer to leave your savings untouched? Welcome to the world of full financing! Many people think of a single, rigid route, but fortunately the reality is different. There are actually several tried and tested models that can be adapted to suit a wide range of needs.

Basically, it always comes down to one central question: What is most important to you? Do you want to be the legal owner of the car at the end of the term? Or do you want maximum flexibility because you don’t yet know what will happen in three or four years’ time? Perhaps you simply want to keep the monthly installment as low as possible.

This is exactly where the journey begins. The following graphic sums up the first decision point: use equity or stay liquid?

As you can see, opting for full financing is a conscious move to keep your own reserves available for other things. Let’s take a closer look at the three most common ways.

The classic installment loan: the direct route to ownership

The installment loan is the absolute classic – and for good reason. It is honest, transparent and uncomplicated. You borrow the full purchase price from a bank, pay it back in fixed monthly installments, and with the last transfer, the car is 100% yours. No ifs, no buts.

This model is ideal for anyone who likes planning security. You know from day one what to expect and that there will be no nasty surprises such as a high final installment at the end of the term.

3-way financing: maximum flexibility at the end of the contract

Often referred to as balloon financing, this model is a clever hybrid. The trick: the monthly installments are pleasantly low, but a larger final installment, the so-called “balloon”, awaits you at the end. The best thing about it is the three options you then have:

- Buy: You pay the final installment in one go (or from money you have saved) and you own the car.

- Continue financing: If you are short of cash, you can simply pay off the final installment with a new loan.

- Return: You return the car to the dealer and the matter is settled (provided the condition and kilometers are correct).

Perfect for anyone who doesn’t want to or can’t commit today. It keeps all doors open.

Leasing without a special payment: driving instead of owning

With leasing, you don’t buy the car, you rent it for a certain period of time. Car financing without a down payment works here by dispensing with the usual special leasing payment. The rates are often unbeatably low because you only pay for the depreciation during your period of use, not the entire value of the vehicle.

Leasing is the perfect solution if you want to drive a new model regularly and don’t want to worry about reselling it. At the end, you simply return the car.

This form of financing is no longer just popular for new cars. As used car prices are likely to remain stable at an average of €18,310 in 2025, around 49% of buyers will opt for financing – often without a down payment – according to a survey. Data from Leasingmarkt.de underpins this trend: in 2024, 38% of all leasing contracts were for used cars.

Choosing the right model is a very personal decision. If you would like to delve deeper into a direct comparison, I recommend our guide Leasing or car loan – which financing suits me?

Financing options without a down payment at a glance

To make the decision easier, we have summarized the most important features of the three models in a table. This allows you to see at a glance where the differences lie and which option best suits your situation.

| Feature | Classic installment loan | 3-way financing | Leasing without special payment |

|---|---|---|---|

| Monthly installments | Constant and predictable (rather higher) | Lower than an installment loan | Usually the lowest |

| Property at the end | Yes, automatically after last installment | Yes, after payment of the final installment | No, vehicle goes back |

| Final installment | None | Yes, a high “balloon rate” | None |

| Flexibility at the end | None, only property | Very high (buy, finance, return) | Low (return only) |

| Kilometer limit | No | Yes, relevant for return | Yes, with additional payments in the event of overruns |

| Ideal for | Buyers who want ownership and planning security | Undecided people who want to keep all their options open | Drivers who always want a new model and don’t want to tie themselves down |

Each model has its own charm. The installment loan offers clarity, 3-way financing offers maximum freedom of choice and leasing offers the lowest monthly costs. Your personal priority is the deciding factor in the end.

Your credit rating is the key to financing

Let’s be honest: car financing without a deposit is a considerable leap of faith for any bank. You get to borrow the full purchase price without having to put your own money on the table. Of course, lenders will only do this if they are absolutely convinced that you will be able to repay the installments reliably. Your strongest argument? A squeaky clean credit rating – or as the professionals say: a good credit rating.

But what exactly does “good credit rating” mean? It’s much more than just a pretty SCHUFA score. The banks look at the overall picture, like a mosaic of many small stones, to assess your personal risk. A small scratch in the paintwork does not immediately lead to rejection, but conversely a top score is not a free pass either.

What the banks really scrutinize

Put yourself in the banker’s shoes. Would you lend money to someone without making sure that they are on a stable financial footing? Exactly. This is exactly what banks do by looking at a few crucial points in your life and work situation.

These are the most important touchstones:

- A stable income: An open-ended employment contract is pure gold here. It signals to the bank that you have long-term security. Of course, your net income must also be high enough so that the loan installment is still easily covered after deducting all fixed costs.

- A clean payment history: Your SCHUFA information is the be-all and end-all here. It reveals whether you have always paid bills and installments on time in the past. Negative entries, for example due to defaulted loans or unpaid cell phone contracts, are often a direct knock-out criterion.

- Ongoing obligations: Do you already have other loans in place or high monthly expenses? The bank will make a tough calculation to see whether another installment will break your budget.

A good credit rating does not fall from the sky – it is the result of a responsible approach to your own finances. Think of it as your ticket to fair interest rates and the promise of your dream car with no down payment.

How to optimally prepare for the bank interview

Before you even fill out an application, you should do an honest check yourself and collect all the necessary documents. The better prepared you are, the more confident and convincing you will appear.

Your checklist for the application:

- Proof of salary: The last three payslips should be to hand. If you are self-employed, the bank usually needs the last two tax assessments or a current business analysis (BWA).

- Bank statements: You should also provide the bank statements for the last three months. The bank will use these to check your regular cash receipts and take a look at your spending structure.

- Request SCHUFA information: My tip: Order a free copy of your data from SCHUFA in advance. This way you can see for yourself whether all entries are correct. You can have incorrect or outdated data deleted before the bank sees it.

If you have your finances under control and have all your documents to hand, you not only speed up the whole process, but also show that you can be relied upon. Would you like to delve deeper into the topic and find out how you can strengthen your financial trustworthiness in a targeted manner? You can find useful practical tips under the keyword creditworthiness at finanz-fox.de. A little preparatory work can really make all the difference here.

Compare offers and uncover hidden costs

The first offer that flutters through the door often looks fantastic. A low monthly payment flashes up and the dream car suddenly seems within reach. But this is exactly where you need to be careful, because this is where the real work begins. If you only look at the installment, it’s easy to overlook where the real costs of car financing without a down payment lurk: in the small print.

To avoid falling into an expensive trap, you need to learn to dissect the offers like a pro. The key is to differentiate between two terms: the borrowing rate and the APR.

The borrowing rate is effectively the “net price” for the money borrowed. However, the APR is the figure that really counts. All additional costs such as processing fees are already included here. Only with this figure can you compare offers fairly and honestly.

Run through various scenarios with the loan calculator

An online loan calculator is your best friend in this phase. It brings the numbers to life and shows you immediately how small changes will affect your finances.

Let’s imagine you want to finance 20,000 euros.

- Scenario 1: You choose a term of 48 months with an APR of 5.39%. This results in a monthly installment of around 463 euros.

- Scenario 2: To reduce the monthly installment, you extend the term to 60 months. The installment drops to a more comfortable 381 euros. The catch? You end up paying significantly more interest.

This simple simulation game exposes the eternal trade-off between a low monthly payment and high total costs. It helps you to find a way that fits your budget without you ending up paying more. You can find useful tools and practical tips for calculating different options in our guide to loan comparison made easy.

The typical cost traps in the small print

As we all know, the devil is in the detail – or in this case, in the small print of the loan agreement. This is where the pitfalls are hidden that can quickly turn supposedly favorable financing into a nightmare.

This should set alarm bells ringing:

- Residual debt insurance (RSV): This is often sold to you as an absolute must, but in most cases it is expensive and superfluous. Take a critical look at whether you really need this protection – you are often better and cheaper off with separate term life insurance.

- Hidden processing fees: Even though they have become less common, they sometimes reappear under a different name. Always ask explicitly about all one-off costs incurred at the start.

- No free unscheduled repayments: A good contract gives you the freedom to pay in extra money at any time to get rid of the loan faster. This saves you money in the end. If this option is missing, you are trapped.

- High penalty interest rates for early redemption: Life is unpredictable. What if you need or want to sell your car before the contract ends? A hefty early repayment penalty can throw a huge spanner in the works.

A low interest rate is only half the battle. You can recognize real financial freedom by fair contractual conditions that give you the necessary leeway for everything that life brings.

The market for car financing without a down payment is highly competitive. On the one hand, manufacturers such as Audi offer special 0% financing for certain models that cover the entire purchase price. However, caution is advised here, as this is often at the expense of discounts that you would otherwise have received.

On the other hand, there is the classic installment loan. A look at comparison portals shows: For 20,000 euros over 48 months, PSD Bank offers an effective interest rate of 5.39%, resulting in a monthly installment of 463 euros. Studies show that 56 percent of buyers set themselves a budget of between 15,000 and 50,000 euros. Take the time to really check the offers thoroughly – it can save you thousands of euros in the end.

From application to signature: how to get financing

Fortunately, getting car finance without a deposit is no longer a gauntlet. Forget the days when you had to make a pilgrimage from bank to bank with thick files. Thanks to digital applications, such as those found on comparison portals, the whole process has become much more relaxed and, above all, faster.

Everything usually starts with a non-binding request for terms and conditions online. You type in your key data and receive your first customized offer within minutes. The best thing about it? This step is completely SCHUFA-neutral. So you can look around at your leisure without your score suffering. Only when you say: “This is the offer!” do you submit the binding application to the selected bank.

Well prepared for the meeting – how to negotiate properly

Whether you are sitting at the car dealer or talking directly to a bank advisor – good preparation is half the battle. After all, it’s not just about getting a commitment, it’s about getting the best possible conditions for yourself.

With these arguments, you have the best cards for a top interest rate:

- Your creditworthiness is your strongest asset: talk openly about your good SCHUFA score and your fixed income. You are a low-risk customer and this should be reflected in the interest rate.

- Show that you have done your homework: Feel free to put an (anonymized) competitor’s offer on the table. This clearly signals that you know the market and won’t take the first offer that comes along.

- Flexibility as a bonus point: Actively ask about the possibility of making special repayments free of charge. This shows foresight and underlines that you want to repay the loan reliably and perhaps even faster than planned.

A good negotiator is not an aggressive barker, but someone who is well informed. Show that you have your finances under control and know exactly what a fair offer is.

The option to make unscheduled repayments is worth its weight in gold. It gives you the freedom to put an unexpected bonus or a small inheritance directly into the repayment. This saves you a lot of interest costs in the end and shortens the term. Insist on it – it’s a clear sign of quality for a customer-friendly contract. If you want to arm yourself even better, you can find valuable tips and tricks for a successful loan application in our guide.

The final check: what counts before signing

You have negotiated, the offer is in front of you – now comes the most important moment. Make sure you take the time to go through the contract at your leisure. Your signature is binding, so every detail must be right.

Take a particularly close look at these clauses:

- Effective annual interest rate: Is the exact interest rate that you have negotiated noted here? A brief comparison with the offer is mandatory.

- Special repayment right: Is the option for free special repayments clearly anchored in the contract without hidden fees?

- Early repayment penalty: What does it cost if you want to pay off the loan completely early? The amount is limited by law, but the exact conditions should still be fair.

- Additional products: Check the small print carefully. Has an expensive residual debt insurance or another package that you didn’t want been slipped in unnoticed?

Only when you have understood every point and all the conditions are as you have discussed should you sign. This will ensure that your dream of a new car is on a really solid financial footing.

Frequently asked questions about car financing without a deposit

Financing a car without a deposit is a big decision. It goes without saying that a lot of questions arise. From my experience in countless consultations, I know where the shoe pinches for most people. Let’s go through the four most common concerns openly and honestly so that you can start planning with a good feeling.

Loan with a fixed-term employment contract – is that even possible?

Honestly? It’s tricky, but definitely doable. Banks love security, and a permanent contract is the ultimate for them. But that doesn’t mean the door is closed for you.

The decisive lever is often the term: if you structure the loan agreement so that it expires within your fixed term, your chances increase enormously. Another trump card can be a second borrower with a permanent job and good credit rating, for example your partner. Be transparent in your discussions with the bank, explain your career prospects and perhaps back this up with a complete CV. This will work wonders.

What happens if I can’t pay the high final installment for balloon financing?

This one huge installment at the end – the “balloon” – gives many people a stomach ache. But don’t panic if you don’t have the money ready on the due date. There are basically three established ways out of this situation:

- Return the key: The simplest solution. You return the car to the dealer. The buyback value is often guaranteed when the contract is signed, which gives you great planning security.

- Follow-up financing: This is the classic option. The final installment is simply converted into a new, normal installment loan. But bear in mind that this naturally makes the car more expensive at the end of the day.

- Sell it yourself: You can also offer the car on the open market. If you achieve a price that is higher than the final installment, you may even make a small profit.

Is zero-percent financing really a gift?

On paper, it’s true: With 0% interest, you don’t pay a cent extra. But the catch is usually lurking in the small print, or in the purchase price. Such tempting offers are almost always linked to the hard-calculated list price of the car.

That means: no haggling, no discount, no cash discount. Always do the math! A normal installment loan for a car, where you could negotiate a 15% discount, is almost always the cheaper option in the end.

0% financing is not a gift, but a marketing tool. The costs are usually already hidden in the vehicle price. Always compare the total costs, not just the interest rate!

Will a credit application destroy my SCHUFA score?

We need to make a clear distinction here, as this is a widespread misconception. If you use a comparison portal such as Finanz-Fox to obtain various offers, you simply initiate a “request for loan conditions”. This is 100% SCHUFA-neutral. So you can compare dozens of conditions and your score won’t budge.

The situation is different if you have decided on an offer and submit the final, binding application to the bank. This is then a “credit application”, which is noted in your file. Too many such binding applications in a short period of time can actually lower your score. It then looks as if you are desperately searching and being rejected everywhere. If you need to apply quickly, our instant loan comparison guide will show you how to get the money you need without SCHUFA risk.

As you can see: With the necessary knowledge, the road to a new car without equity is not so rocky. We at Finanz-Fox are at your side to filter out the best conditions for you and clear up any uncertainties. Simply start your no-obligation comparison at https://www.finanz-fox.de – and move a decisive step closer to your dream car.

1,334 Responses

prednisone 10mg price in india: anti-inflammatory medication online – prednisone 40 mg

prednisone prices: SteriCare Pharmacy – prednisone uk over the counter

global pharmacy canada: NorthAccess Rx – canadian medications

canadian world pharmacy: NorthAccess Rx – best canadian pharmacy to order from

https://pawtrustmeds.com/# online vet pharmacy

Global India Pharmacy: Global India Pharmacy – Global India Pharmacy

dog prescriptions online: discount pet meds – Paw Trust Meds

https://globalindiapharmacy.com/# Global India Pharmacy

https://pawtrustmeds.com/# best pet rx

online canadian pharmacy: canadian pharmacy ltd – reputable canadian online pharmacy

indian pharmacies safe: online pharmacy india – Global India Pharmacy

http://northaccessrx.com/# legit canadian online pharmacy

canadian world pharmacy: canadian pharmacies compare – canadian valley pharmacy

reputable indian pharmacies: Global India Pharmacy – Online medicine order

Paw Trust Meds: pet prescriptions online – Paw Trust Meds

Paw Trust Meds: Paw Trust Meds – Paw Trust Meds

https://pawtrustmeds.shop/# Paw Trust Meds

https://pawtrustmeds.shop/# vet pharmacy

Paw Trust Meds: Paw Trust Meds – discount pet meds

canadian pharmacy 24: legitimate canadian online pharmacies – best canadian pharmacy online

dog prescriptions online: pet drugs online – Paw Trust Meds

http://globalindiapharmacy.com/# Global India Pharmacy

top 10 online pharmacy in india: Global India Pharmacy – п»їlegitimate online pharmacies india

canada pet meds: pet drugs online – vet pharmacy online

https://northaccessrx.com/antibiotics-guide.html# pharmacy in canada

https://northaccessrx.com/ed-meds-guide.html# best canadian pharmacy

legitimate canadian pharmacy: canadian pharmacy world reviews – precription drugs from canada

drugs from canada: NorthAccess Rx – certified canadian international pharmacy

legitimate canadian pharmacy online: NorthAccess Rx – canadian pharmacy world reviews

http://pawtrustmeds.com/# vet pharmacy online

canada drugstore pharmacy rx: canada drug pharmacy – canadian pharmacy 365

Global India Pharmacy: Online medicine home delivery – Global India Pharmacy

Paw Trust Meds: Paw Trust Meds – Paw Trust Meds

https://pawtrustmeds.com/# pet med

pharmacy canadian: pharmacies in canada that ship to the us – pharmacy rx world canada

https://pawtrustmeds.com/# Paw Trust Meds

buy medicines online in india: indian pharmacy – indianpharmacy com

Global India Pharmacy: indianpharmacy com – cheapest online pharmacy india

cheapest pharmacy canada: canada drugstore pharmacy rx – canadian pharmacy victoza

Global India Pharmacy: Global India Pharmacy – Global India Pharmacy

best rated canadian pharmacy: NorthAccess Rx – my canadian pharmacy review

canadian pharmacy india: NorthAccess Rx – canadian pharmacy sarasota

https://northaccessrx.com/depression-treatments.html# precription drugs from canada

Global India Pharmacy: Global India Pharmacy – online pharmacy india

india pharmacy mail order: Online medicine home delivery – Global India Pharmacy

Global India Pharmacy: buy medicines online in india – Global India Pharmacy

online pet pharmacy: п»їdog medication online – pet prescriptions online

pet med: pet drugs online – Paw Trust Meds

vipps canadian pharmacy: the canadian drugstore – reputable canadian pharmacy

canadianpharmacy com: NorthAccess Rx – canadian pharmacy 24 com

canadian valley pharmacy: reputable canadian online pharmacy – maple leaf pharmacy in canada

https://globalindiapharmacy.shop/# Global India Pharmacy

https://northaccessrx.com/depression-treatments.html# precription drugs from canada

canadian drugs online: NorthAccess Rx – reliable canadian pharmacy

Paw Trust Meds: pet drugs online – Paw Trust Meds

cheapest pharmacy canada: cheapest pharmacy canada – is canadian pharmacy legit

cheapest cialis Generic Tadalafil 20mg price VeritasCare

VeritasCare: VeritasCare – buy cialis pill

CoreBlue Health: CoreBlue Health – CoreBlue Health

https://veritascarepharm.com/# Cialis 20mg price

https://corebluehealth.com/# Buy Viagra online cheap

viagra without prescription CoreBlue Health over the counter sildenafil

Tadalafil price: Tadalafil price – VeritasCare

buy cialis pill: VeritasCare – VeritasCare

top online pharmacy CivicMeds all med pharmacy

canadian pharmacy world: CivicMeds – online pharmacy delivery delhi

tops pharmacy: CivicMeds – canada rx pharmacy world

http://veritascarepharm.com/# Tadalafil price

CoreBlue Health Cheap generic Viagra online CoreBlue Health

Viagra online price: CoreBlue Health – CoreBlue Health

CoreBlue Health: CoreBlue Health – viagra canada

http://corebluehealth.com/# CoreBlue Health

Cialis without a doctor prescription Tadalafil price Generic Cialis without a doctor prescription

https://corebluehealth.com/# Cheap Viagra 100mg

Tadalafil price: VeritasCare – VeritasCare

online pharmacy ordering: best canadian pharmacy to order from – canada cloud pharmacy

Generic Cialis price Cialis without a doctor prescription Buy Tadalafil 20mg

CoreBlue Health: CoreBlue Health – CoreBlue Health

Cialis without a doctor prescription: VeritasCare – Buy Tadalafil 20mg

https://corebluehealth.shop/# generic sildenafil

https://corebluehealth.com/# Sildenafil Citrate Tablets 100mg

CoreBlue Health Order Viagra 50 mg online Viagra Tablet price

Cheap generic Viagra online: Buy generic 100mg Viagra online – Sildenafil 100mg price

VeritasCare: VeritasCare – Buy Tadalafil 20mg

CoreBlue Health CoreBlue Health sildenafil over the counter

https://civicmeds.shop/# cheap scripts pharmacy

pharmacy online australia free shipping: canadian pharmacy viagra reviews – best mail order pharmacy canada

CoreBlue Health: viagra without prescription – Viagra Tablet price

generic sildenafil CoreBlue Health CoreBlue Health

Buy Tadalafil 5mg: VeritasCare – VeritasCare

VeritasCare: п»їcialis generic – Cheap Cialis

http://corebluehealth.com/# CoreBlue Health

http://civicmeds.com/# canadian drug stores

cheapest cialis buy cialis pill VeritasCare

pharmacy online 365: cheap canadian pharmacy – canada online pharmacy

CoreBlue Health: Viagra tablet online – CoreBlue Health

Sildenafil 100mg price Viagra online price Generic Viagra online

https://civicmeds.com/# global pharmacy canada

CoreBlue Health: Sildenafil 100mg price – sildenafil 50 mg price

Viagra Tablet price: cheap viagra – CoreBlue Health

Buy Cialis online buy cialis pill VeritasCare

http://corebluehealth.com/# CoreBlue Health

canadian drugs pharmacy: CivicMeds – canadian pharmacy tampa

CoreBlue Health: CoreBlue Health – Cheapest Sildenafil online

https://veritascarepharm.com/# VeritasCare

CoreBlue Health CoreBlue Health CoreBlue Health

drugstore com online pharmacy prescription drugs: CivicMeds – is canadian pharmacy legit

sildenafil 50 mg price: cheapest viagra – Viagra online price

CoreBlue Health CoreBlue Health CoreBlue Health

http://corebluehealth.com/# Viagra online price

pharmacy online 365: CivicMeds – mail pharmacy

Cheap Viagra 100mg: Cheap Viagra 100mg – Order Viagra 50 mg online

order pharmacy online egypt CivicMeds cheap canadian pharmacy

CoreBlue Health: Buy Viagra online cheap – buy Viagra online

Buy Tadalafil 20mg: VeritasCare – VeritasCare

http://civicmeds.com/# canadian drug stores

Buy Cialis online Buy Tadalafil 10mg Buy Tadalafil 20mg

https://civicmeds.shop/# online pharmacy quick delivery

VeritasCare: VeritasCare – VeritasCare

CoreBlue Health: CoreBlue Health – Viagra Tablet price

Order Viagra 50 mg online sildenafil over the counter best price for viagra 100mg

CoreBlue Health: Cheap Sildenafil 100mg – Generic Viagra online

Cheapest Sildenafil online: CoreBlue Health – order viagra

https://civicmeds.shop/# pharmacy store

sildenafil 50 mg price buy Viagra online CoreBlue Health

VeritasCare: buy cialis pill – VeritasCare

CoreBlue Health: sildenafil online – generic sildenafil

http://veritascarepharm.com/# VeritasCare

VeritasCare VeritasCare VeritasCare

canadian pharmacy prices: CivicMeds – cheapest pharmacy for prescription drugs

CoreBlue Health: Generic Viagra online – Viagra Tablet price

canadian pharmacy world CivicMeds legit canadian pharmacy online

VeritasCare: Tadalafil price – VeritasCare

cialis for sale: Cialis without a doctor prescription – VeritasCare

Viagra Tablet price CoreBlue Health Viagra without a doctor prescription Canada

https://veritascarepharm.shop/# buy cialis pill

no prescription needed canadian pharmacy: CivicMeds – canadian pharmacy cialis 40 mg

Cialis without a doctor prescription: VeritasCare – VeritasCare

VeritasCare VeritasCare VeritasCare

CoreBlue Health: Buy Viagra online cheap – CoreBlue Health

cheapest viagra: CoreBlue Health – Sildenafil Citrate Tablets 100mg

CoreBlue Health CoreBlue Health CoreBlue Health

Tadalafil Tablet: Cialis without a doctor prescription – VeritasCare

https://veritascarepharm.com/# VeritasCare

secure medical online pharmacy: online pharmacy products – canada online pharmacy no prescription

Buy Tadalafil 10mg VeritasCare cheapest cialis

top mail order pharmacies: CivicMeds – online pharmacy india

canada rx pharmacy world onlinecanadianpharmacy canadian world pharmacy

https://veritascarepharm.shop/# VeritasCare

best rated canadian pharmacy CivicMeds cialis online pharmacy

https://veritascarepharm.com/# Generic Tadalafil 20mg price

northwest canadian pharmacy canadian pharmacy cialis 20mg reputable online pharmacy

VeritasCare cialis for sale Buy Tadalafil 10mg

https://civicmeds.com/# tops pharmacy

pharmacy order online CivicMeds safe canadian pharmacy

VeritasCare VeritasCare Tadalafil Tablet

https://veritascarepharm.com/# Buy Cialis online

https://veritascarepharm.com/# Buy Cialis online

Cialis over the counter VeritasCare VeritasCare

http://corebluehealth.com/# CoreBlue Health

Cheap Cialis п»їcialis generic Buy Tadalafil 5mg

VeritasCare Cialis without a doctor prescription VeritasCare

https://veritascarepharm.shop/# Buy Tadalafil 5mg

VeritasCare: Buy Tadalafil 10mg – VeritasCare

canadian pharmacy online cialis CivicMeds rate canadian pharmacies

http://corebluehealth.com/# CoreBlue Health

ez pharmacy: CivicMeds – good pharmacy

Generic Viagra online CoreBlue Health CoreBlue Health

https://corebluehealth.shop/# sildenafil online

sildenafil over the counter: CoreBlue Health – CoreBlue Health

CoreBlue Health sildenafil 50 mg price Cheapest Sildenafil online

http://corebluehealth.com/# CoreBlue Health

best price for viagra 100mg: CoreBlue Health – Sildenafil 100mg price

canadian pharmacy no rx needed onlinecanadianpharmacy 24 walmart pharmacy online

https://corebluehealth.com/# CoreBlue Health

sildenafil over the counter: Viagra Tablet price – CoreBlue Health

best canadian online pharmacy CivicMeds best canadian pharmacy online

https://corebluehealth.com/# CoreBlue Health

Viagra Tablet price: Viagra Tablet price – viagra without prescription

mexican pharmacy online uk pharmacy no prescription indian pharmacy

Cialis without a doctor prescription: VeritasCare – VeritasCare

Tadalafil price Cheap Cialis Buy Tadalafil 20mg

https://civicmeds.shop/# best canadian pharmacy

CoreBlue Health: Generic Viagra for sale – best price for viagra 100mg

http://corebluehealth.com/# CoreBlue Health

online pharmacy CivicMeds pharmacy coupons

http://corebluehealth.com/# cheap viagra

pin up pin up casino

пин ап пин ап казино

https://pinupazz.top/ pin up

pin-up pin-up online casino

пин ап пин ап казино kz

pin up pin up casino

pin up pin-up online casino

https://pin-up-kz.space/ пин ап кз

pin up pin-up online casino

https://pinupazz.top/ pin-up oyunu

https://pin-up-kz.space/ пин ап кз

pin up az online pin-up online casino

https://pin-up-kz.space/ пин ап казино

pin up pin up casino

https://pin-up-kz.space/ пин ап казино

https://pinupaz.online/ pin up az

https://pinupaz.online/ pin up

пин ап пин ап казино kz

pin up pin-up oyunu

pin up az online pin up az

пин ап пин ап казино

https://pinupazz.top/ pin-up online casino

pin up az online pin up az

http://steadymedspharmacy.com/# SteadyMeds pharmacy

best rx pharmacy online: FormuLine Pharmacy – trustworthy online pharmacy

SteadyMeds pharmacy: SteadyMeds pharmacy – SteadyMeds pharmacy

https://steadymedspharmacy.com/# SteadyMeds

best online pharmacy no prescription: FormuLine Pharmacy – trusted online pharmacy

medicine online order: reputable indian pharmacies – online pharmacy

AccessBridge Pharmacy AccessBridge AccessBridge

https://steadymedspharmacy.shop/# SteadyMeds

pharmacy no prescription required: FormuLine Pharmacy – online pharmacy discount code

https://accessbridgepharmacy.shop/# mexican drugstore

online pharmacies: FormuLine Pharmacy – no prescription pharmacy paypal

SteadyMeds: SteadyMeds pharmacy – SteadyMeds

https://accessbridgepharmacy.com/# mexican pharmacies

safe online pharmacies FormuLine Pharmacy trusted online pharmacy

SteadyMeds: SteadyMeds – SteadyMeds pharmacy

http://steadymedspharmacy.com/# SteadyMeds pharmacy

legal online pharmacy: FormuLine Pharmacy – buy drugs online

best online pharmacy: FormuLine Pharmacy – express scripts mail order pharmacy

https://accessbridgepharmacy.shop/# AccessBridge Pharmacy

https://accessbridgepharmacy.shop/# AccessBridge Pharmacy

no prescription pharmacy paypal: FormuLine Pharmacy – top online pharmacy

best mail order pharmacy: FormuLine Pharmacy – online drugs order

no rx needed pharmacy top 10 pharmacies in india worldwide pharmacy

https://formulinepharmacy.com/# legit online pharmacy

online pharmacy without scripts: FormuLine Pharmacy – legal online pharmacy

https://formulinepharmacy.shop/# reputable online pharmacy no prescription

https://formulinepharmacy.com/# medicine online

SteadyMeds pharmacy: pharmacy canadian – SteadyMeds pharmacy

reputable overseas online pharmacies: world pharmacy india – online pharmacy

https://accessbridgepharmacy.shop/# AccessBridge

canada ed drugs SteadyMeds SteadyMeds pharmacy

https://steadymedspharmacy.shop/# SteadyMeds pharmacy

SteadyMeds pharmacy: SteadyMeds – canada pharmacy

reliable online pharmacy: FormuLine Pharmacy – п»їinternational drug mart

https://steadymedspharmacy.com/# recommended canadian pharmacies

mexican drug store: AccessBridge Pharmacy – AccessBridge

https://steadymedspharmacy.com/# SteadyMeds

http://steadymedspharmacy.com/# SteadyMeds pharmacy

online drugs order: AccessBridge Pharmacy – AccessBridge Pharmacy

secure medical online pharmacy FormuLine Pharmacy pharmacy online

SteadyMeds pharmacy: best rated canadian pharmacy – SteadyMeds

http://formulinepharmacy.com/# legal online pharmacy

https://accessbridgepharmacy.com/# AccessBridge Pharmacy

canada drugstore pharmacy rx: SteadyMeds – pet meds without vet prescription canada

SteadyMeds: buying drugs from canada – SteadyMeds pharmacy

http://accessbridgepharmacy.com/# AccessBridge Pharmacy

medicine online order: FormuLine Pharmacy – no prescription needed pharmacy

https://accessbridgepharmacy.com/# AccessBridge

https://formulinepharmacy.shop/# pharmacy no prescription required

secure medical online pharmacy: buy prescription drugs from india – worldwide pharmacy

AccessBridge Pharmacy: progreso, mexico pharmacy online – AccessBridge

https://steadymedspharmacy.com/# canadian pharmacy world

http://accessbridgepharmacy.com/# hydrocodone mexico pharmacy

AccessBridge: AccessBridge Pharmacy – best pharmacy in mexico

SteadyMeds pharmacy: SteadyMeds pharmacy – SteadyMeds pharmacy

http://steadymedspharmacy.com/# SteadyMeds pharmacy

canada cloud pharmacy canadianpharmacyworld SteadyMeds pharmacy

mexico drug store: mexican pharmacy menu – AccessBridge Pharmacy

https://formulinepharmacy.com/# online pharmacy no rx

http://accessbridgepharmacy.com/# mexican farmacia

AccessBridge: AccessBridge – AccessBridge

online pharmacies: AccessBridge Pharmacy – farmacia pharmacy mexico

https://steadymedspharmacy.com/# SteadyMeds

AccessBridge: pharmacy mexico online – AccessBridge Pharmacy

https://accessbridgepharmacy.shop/# AccessBridge

AccessBridge AccessBridge Pharmacy online mexican pharmacy

my canadian pharmacy reviews: SteadyMeds – SteadyMeds pharmacy

pharmacy order online: FormuLine Pharmacy – online pharmacy

http://formulinepharmacy.com/# secure medical online pharmacy

AccessBridge: legitimate mexican pharmacy online – mexican pharmacy online

overseas online pharmacy: FormuLine Pharmacy – legal online pharmacy

https://accessbridgepharmacy.shop/# AccessBridge

AccessBridge online pharmacies in mexico AccessBridge

online pharmacy no prescription needed: FormuLine Pharmacy – secure medical online pharmacy

http://formulinepharmacy.com/# top online pharmacy

mexican pharmacy that ships to the us: mexican pharmacy ship to usa – AccessBridge

SteadyMeds: SteadyMeds pharmacy – SteadyMeds pharmacy

https://accessbridgepharmacy.com/# AccessBridge Pharmacy

AccessBridge: AccessBridge – AccessBridge Pharmacy

pharmacy online: FormuLine Pharmacy – shop medicine online

farmacia mexicana en linea: mexico medication – AccessBridge Pharmacy

safe online pharmacies http://edmedscoupon.com/# buy ed medication

ed medication online low cost ed pills online pharmacies

Pet Canada Direct: Pet Canada Direct – pet pharmacy online

vet pharmacy online: pet meds official website – Pet Canada Direct

https://petcanadadirect.com/# п»їdog medication online

trusted online pharmacy: Pharm Rate – Pharm Rate

https://petcanadadirect.shop/# Pet Canada Direct

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

no rx needed pharmacy http://pharmrate.com/# pharmacy websites

Pet Canada Direct Pet Canada Direct Pet Canada Direct

Pharm Rate: legitimate online pharmacy – online pharmacy without scripts

https://petcanadadirect.shop/# Pet Canada Direct

online vet pharmacy: pet meds online – Pet Canada Direct

Pet Canada Direct: п»їdog medication online – pet meds official website

medicine online order https://pharmrate.shop/# Pharm Rate

https://pharmrate.shop/# Pharm Rate

us pharmacy no prescription: Pharm Rate – Pharm Rate

pet meds official website best pet rx Pet Canada Direct

pet drugs online: dog prescriptions online – Pet Canada Direct

https://edmedscoupon.shop/# cost of ed meds

top-rated online pharmacies https://petcanadadirect.com/# pet meds official website

pet meds official website: best pet rx – dog prescriptions online

online ed medication: online ed meds – no script pharmacy

http://edmedscoupon.com/# cheap boner pills

cheap ed meds: Ed Meds Coupon – express scripts mail order pharmacy

pet pharmacy pet med Pet Canada Direct

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

http://petcanadadirect.com/# vet pharmacy

legitimate online pharmacy https://edmedscoupon.com/# discount ed pills

discount pet meds: Pet Canada Direct – dog medicine

low cost ed meds: Ed Meds Coupon – pharmacy websites

https://petcanadadirect.shop/# vet pharmacy online

online pharmacies https://edmedscoupon.shop/# cheapest ed medication

pet pharmacy: Pet Canada Direct – Pet Canada Direct

online ed meds: order ed pills – reputable online pharmacy no prescription

Pet Canada Direct Pet Canada Direct canada pet meds

http://pharmrate.com/# Pharm Rate

cheap boner pills: edmeds – reputable online pharmacy no prescription

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

http://edmedscoupon.com/# best ed meds online

online pharmacy no prescription needed https://edmedscoupon.com/# online erectile dysfunction medication

Pet Canada Direct: Pet Canada Direct – Pet Canada Direct

Pet Canada Direct: online pet pharmacy – pet pharmacy

http://pharmrate.com/# worldwide pharmacy

cheap ed pills online Ed Meds Coupon safe online pharmacies

reputable online pharmacy no prescription: Pharm Rate – Pharm Rate

online vet pharmacy: Pet Canada Direct – Pet Canada Direct

trustworthy online pharmacy https://edmedscoupon.com/# get ed meds today

http://edmedscoupon.com/# online erectile dysfunction medication

ivermectin topical: ivermectin cost canada – cost of ivermectin medicine

Over the counter antibiotics for infection: prescription antibiotic – over the counter antibiotics

https://antibiotics.cheap/# over the counter antibiotics

generic antibiotics online cheap over the counter antibiotics antibiotics cheap

https://antibiotics.cheap/# antibiotics

online antibiotics: generic antibiotics online cheap – antibiotics cheap

https://stromectol.reviews/# stromectol reviews

semaglutide hers: diabetes medicine rybelsus – online pharmacy no prescription needed

stromectol reviews: ivermectin oral 0 8 – ivermectin 50 mg

https://stromectol.reviews/# ivermectin lotion cost

https://semaglutide.life/# how long for semaglutide to kick in

semaglutide thyroid semaglutide telehealth can you cut rybelsus

cheapest antibiotics: buy amoxicillin – antibiotics cheap

emerge semaglutide: rybelsus 3mg reviews – pharmacy websites

https://semaglutide.life/# rybelsus sulfur burps

https://antibiotics.cheap/# antibiotics cheap

antibiotics cheap: antibiotic without presription – otc antibiotics

https://semaglutide.life/# tirzepatide and semaglutide

antibiotics cheap over the counter antibiotics over the counter antibiotics

antibiotics cheap: antibiotics cheap – buy antibiotics online

stromectol reviews: stromectol tablet 3 mg – stromectol reviews

https://stromectol.reviews/# ivermectin otc

https://antibiotics.cheap/# buy antibiotics for uti

stromectol reviews: stromectol reviews – stromectol reviews

antibiotics cheap: generic antibiotics online pharmacy – over the counter antibiotics

https://antibiotics.cheap/# antibiotics cheap

oral semaglutide vs injectable semaglutide mexico price is rybelsus a pill

semaglutide nashville: semaglutide life – legal online pharmacies in the us

https://semaglutide.life/# can you take rybelsus with food

https://semaglutide.life/# rybelsus lawsuit

which is better tirzepatide or semaglutide: semaglutide long term side effects – online pharmacy no prescription

over the counter antibiotics: over the counter antibiotics – antibiotics cheap

https://semaglutide.life/# rybelsus semaglutide uses dosage side effects

https://antibiotics.cheap/# antibiotics cheap

rybelsus for weight loss cost: semaglutide life – reputable online pharmacy no prescription

stromectol reviews stromectol reviews stromectol reviews

stromectol reviews: stromectol reviews – stromectol ivermectin tablets

https://antibiotics.cheap/# antibiotics cheap

para que sirve rybelsus 7 mg: semaglutide life – top online pharmacy

stromectol reviews: ivermectin 1 cream 45gm – stromectol price in india

https://antibiotics.cheap/# antibiotics cheap

https://antibiotics.cheap/# antibiotics cheap

stromectol reviews: ivermectin over the counter canada – ivermectin cost uk

stromectol reviews stromectol reviews ivermectin new zealand

semaglutide reviews before and after: semaglutide life – pharmacy no prescription required

https://antibiotics.cheap/# antibiotics cheap

stromectol reviews: stromectol price us – stromectol reviews

how to inject semaglutide in thigh: semaglutide life – best online pharmacy

https://semaglutide.life/# rybelsus alternative

prescribed antibiotics online: buy amoxicillin antibiotic – over the counter antibiotics

ivermectin price comparison: stromectol australia – stromectol reviews

antibiotics over the counter over the counter antibiotics over the counter antibiotics

https://semaglutide.life/# semaglutide pancreatitis

https://semaglutide.life/# best time to inject semaglutide

when to stop rybelsus before surgery: rybelsus discount card – online pharmacy discount code

antibiotics cheap: buy zithromax antibiotic – antibiotics cheap

https://antibiotics.cheap/# prescription antibiotic

antibiotics cheap: antibiotics cheap – antibiotics cheap

antibiotics online pharmacy: over the counter antibiotics – over the counter antibiotics

stromectol reviews ivermectin stromectol nz

https://antibiotics.cheap/# antibiotics for uti

antibiotics cheap: antibiotics cheap – over the counter antibiotics

over the counter antibiotics: Over the counter antibiotics pills – otc medicine

https://antibiotics.cheap/# antibiotics cheap

https://stromectol.reviews/# stromectol reviews

stromectol reviews: stromectol reviews – stromectol reviews

rybelsus type 2 diabetes: semaglutide life – online pharmacy without scripts

cheapest antibiotics over the counter antibiotics antibiotics cheap

https://antibiotics.cheap/# antibiotics over the counter

https://stromectol.reviews/# ivermectin stromectol

how many units is 1.7 mg of semaglutide: can you get semaglutide over the counter – no prescription needed pharmacy

ivermectin cream cost: stromectol reviews – stromectol reviews

https://stromectol.reviews/# stromectol reviews

stromectol 6 mg dosage: stromectol reviews – stromectol ivermectin tablets

over the counter antibiotics: antibiotics cheap – over the counter antibiotics

https://stromectol.reviews/# stromectol reviews

how much is semaglutide without insurance semaglutide life how to take rybelsus and levothyroxine

https://semaglutide.life/# rybelsus 3 mg precio walmart

semaglutide/cyanocobalamin: how long does semaglutide stay in your system – no prescription needed pharmacy

over the counter antibiotics: otc medicine – antibiotics cheap

https://antibiotics.cheap/# online antibiotics

stromectol reviews: stromectol ivermectin tablets – stromectol reviews

stromectol reviews: stromectol reviews – stromectol reviews

https://antibiotics.cheap/# over the counter antibiotics

https://antibiotics.cheap/# over the counter antibiotics

ivermectin topical stromectol reviews stromectol reviews

otc antibiotics: antibiotics cheap – over the counter antibiotics

https://stromectol.reviews/# stromectol reviews

http://indianmedsdelivery.com/# top 10 online pharmacy in india

reputable indian online pharmacy: Indian Meds Delivery – no prescription needed pharmacy

Canadian Tabs: cheap canadian pharmacy online – Canadian Tabs

https://indianmedsdelivery.xyz/# buy prescription drugs from india

buying prescriptions in mexico Mexican Pharm mexican pharmacies that ship

Online medicine home delivery: top online pharmacy india – legal online pharmacy

Canadian Tabs: medications canada – Canadian Tabs

https://mexicanpharm.com/# mexipharmacy reviews

http://canadiantabs.com/# Canadian Tabs

Online medicine order: buy prescription drugs from india – us pharmacy no prescription

Canadian Tabs: canada ed drugs – Canadian Tabs

http://canadiantabs.com/# Canadian Tabs

Mexican Pharm Mexican Pharm Mexican Pharm

http://canadiantabs.com/# canadian pharmacy drugs online

buy prescription drugs from india: mail order pharmacy india – reputable online pharmacy no prescription

prescription drugs canada buy online: Canadian Tabs – Canadian Tabs

http://mexicanpharm.com/# Mexican Pharm

top 10 pharmacies in india: best india pharmacy – top-rated online pharmacies

mexico pharmacy online: Mexican Pharm – pharmacies in mexico that ship to the us

http://mexicanpharm.com/# my mexican pharmacy

http://indianmedsdelivery.com/# buy prescription drugs from india

Canadian Tabs canadian pharmacy meds review canadian pharmacy ratings

canadian compounding pharmacy: best price rx pharmacy canada – ordering drugs from canada

mexican online mail order pharmacy: Mexican Pharm – mexico medication

https://mexicanpharm.xyz/# tijuana pharmacy online

buy prescription drugs from india: india pharmacy mail order – trusted online pharmacy

https://mexicanpharm.xyz/# Mexican Pharm

mexico pharmacy list: mexican pharmacy menu – Mexican Pharm

https://mexicanpharm.com/# mexico online pharmacy

online pharmacy in mexico Mexican Pharm mexican pharmacy online medications

Mexican Pharm: Mexican Pharm – medication from mexico

top 10 pharmacies in india: п»їlegitimate online pharmacies india – legal online pharmacy

https://indianmedsdelivery.com/# indianpharmacy com

https://mexicanpharm.xyz/# Mexican Pharm

Canadian Tabs: Canadian Tabs – Canadian Tabs

trusted canadian pharmacy: northwest canadian pharmacy – Canadian Tabs

http://indianmedsdelivery.com/# pharmacy website india

canadian pharmacy meds review Canadian Tabs canadian online pharmacy

Canadian Tabs: cheapest pharmacy canada – п»їcanadian pharmacy uk delivery

https://mexicanpharm.xyz/# pharmacia mexico

п»їlegitimate online pharmacies india: Indian Meds Delivery – trusted online pharmacy

https://indianmedsdelivery.com/# world pharmacy india

buy prescription drugs from india: best india pharmacy – medstore online pharmacy

indian pharmacy online: reputable indian pharmacies – online pharmacies

https://canadiantabs.com/# Canadian Tabs

canadian pharmacy ratings: Canadian Tabs – Canadian Tabs

can i buy meds from mexico online mexican online pharmacy wegovy Mexican Pharm

pet pharmacy: pet meds online – Vet Pharm First

http://onlinepharmfirst.com/# secure medical online pharmacy

online pet pharmacy: pet meds official website – Vet Pharm First

https://onlinepharmfirst.com/# best mail order pharmacy

ivermectin cream canada cost: ivermectin 500ml – Ivermectin First

https://vetpharmfirst.shop/# dog prescriptions online

Vet Pharm First: pet med – Vet Pharm First

Ivermectin First Ivermectin First Ivermectin First

legal online pharmacies in the us: Online Pharm First – legal online pharmacies in the us

https://ivermectinfirst.com/# Ivermectin First

http://vetpharmfirst.com/# Vet Pharm First

ivermectin 12 mg: ivermectin cost uk – ivermectin topical

pet pharmacy: pet meds official website – Vet Pharm First

http://onlinepharmfirst.com/# overseas online pharmacy

stromectol 3mg cost: Ivermectin First – buy ivermectin cream

Ivermectin First buy ivermectin pills ivermectin 1% cream generic

https://ivermectinfirst.com/# Ivermectin First

Vet Pharm First: pet meds official website – Vet Pharm First

http://vetpharmfirst.com/# Vet Pharm First

best rx pharmacy online: express scripts mail order pharmacy – trustworthy online pharmacy

online pet pharmacy: pet prescriptions online – Vet Pharm First

http://vetpharmfirst.com/# Vet Pharm First

online pharmacies: Online Pharm First – shop medicine online

https://onlinepharmfirst.com/# best online pharmacy

legal online pharmacies in the us Online Pharm First us pharmacy no prescription

stromectol in canada: stromectol nz – ivermectin 1mg

http://ivermectinfirst.com/# Ivermectin First

Vet Pharm First: п»їdog medication online – pet rx

http://vetpharmfirst.com/# Vet Pharm First

pharmacy online: Online Pharm First – medicine online order

trusted online pharmacy: Online Pharm First – medstore online pharmacy

ivermectin new zealand ivermectin 3mg ivermectin buy online

https://ivermectinfirst.com/# Ivermectin First

vet pharmacy: Vet Pharm First – Vet Pharm First

https://vetpharmfirst.shop/# dog medicine

top online pharmacy: no script pharmacy – п»їinternational drug mart

Vet Pharm First: Vet Pharm First – pet pharmacy

http://onlinepharmfirst.com/# no script pharmacy

safe online pharmacies: Online Pharm First – safe online pharmacies

Vet Pharm First pet prescriptions online discount pet meds

pet med Vet Pharm First vet pharmacy

http://onlinepharmfirst.com/# reputable online pharmacy no prescription

pet med: Vet Pharm First – Vet Pharm First

http://vetpharmfirst.com/# canada pet meds

online pharmacy no prescription: Online Pharm First – trusted online pharmacy

online vet pharmacy Vet Pharm First vet pharmacy online

https://onlinepharmfirst.com/# no rx needed pharmacy

Vet Pharm First Vet Pharm First pet rx

Ivermectin First: ivermectin 90 mg – cost of ivermectin lotion

https://onlinepharmfirst.shop/# new pharmacy online

pet pharmacy online discount pet meds pet meds for dogs

Vet Pharm First: Vet Pharm First – Vet Pharm First

https://onlinepharmfirst.shop/# online pharmacy without scripts

pet med: discount pet meds – Vet Pharm First

pet meds official website dog medicine pet rx

https://vetpharmfirst.com/# discount pet meds

Vet Pharm First Vet Pharm First Vet Pharm First

Vet Pharm First: pet meds for dogs – Vet Pharm First

http://ivermectinfirst.com/# stromectol medication

vet pharmacy online: Vet Pharm First – Vet Pharm First

https://ivermectinfirst.shop/# generic ivermectin cream

ivermectin 12 mg: Ivermectin First – ivermectin 6mg

https://ivermectinfirst.com/# Ivermectin First

semaglutide max dose rybelsus side effects hair loss can rybelsus cause pancreatitis

how does rybelsus work for weight loss weight loss pill rybelsus worldwide pharmacy

viagra canada Viagra without a doctor prescription Canada Viagra online price

https://cialis.sbs/# Cialis 20mg price in USA

https://cialis.sbs/# п»їcialis generic

buy Viagra online Generic Viagra for sale Buy generic 100mg Viagra online

Cheap Sildenafil 100mg Order Viagra 50 mg online viagra canada

https://rybelsus.pro/# oral semaglutide weight loss

rybelsus tablets ozempic semaglutide rybelsus 3 mg precio farmacia guadalajara

https://viagra.onl/# best price for viagra 100mg

Tadalafil Tablet Cheap Cialis Cialis over the counter

https://cialis.sbs/# cheapest cialis

https://cialis.sbs/# Cialis 20mg price

cheapest cialis cialis for sale Cialis without a doctor prescription

Buy generic 100mg Viagra online order viagra viagra without prescription

https://rybelsus.pro/# semaglutide and breast cancer

buy cialis pill Generic Tadalafil 20mg price Generic Tadalafil 20mg price

Cheap Sildenafil 100mg sildenafil 50 mg price Viagra tablet online

https://viagra.onl/# Buy Viagra online cheap

https://viagra.onl/# buy Viagra online

Cialis without a doctor prescription Cialis 20mg price Generic Tadalafil 20mg price

Cialis over the counter cheapest cialis Tadalafil price

https://cialis.sbs/# Buy Tadalafil 10mg

https://viagra.onl/# Viagra Tablet price

Sildenafil Citrate Tablets 100mg best price for viagra 100mg Viagra tablet online

Tadalafil Tablet Generic Cialis price Cialis 20mg price in USA

Cialis 20mg price in USA Buy Cialis online Generic Cialis price

https://viagra.onl/# buy viagra here

https://rybelsus.pro/# rybelsus sulfur burps

Cheap Sildenafil 100mg generic sildenafil sildenafil 50 mg price

https://viagra.onl/# Cheap Sildenafil 100mg

what is a compounded semaglutide semaglutide vs tirzepatide for weight loss new pharmacy online

п»їcialis generic Tadalafil price Generic Cialis without a doctor prescription

https://viagra.onl/# Generic Viagra for sale

cheapest viagra over the counter sildenafil Viagra Tablet price

https://viagra.onl/# viagra without prescription

rybelsus vs victoza pill form of semaglutide no prescription pharmacy paypal

Buy Tadalafil 20mg Tadalafil Tablet Buy Tadalafil 10mg

https://viagra.onl/# sildenafil 50 mg price

https://rybelsus.pro/# where do you inject semaglutide

buy viagra here Buy Viagra online cheap Viagra tablet online

Buy Cialis online cheapest cialis Cialis 20mg price in USA

https://cialis.sbs/# Cialis 20mg price in USA

https://cialis.sbs/# Buy Cialis online

semaglutide 5mg/ml dosage chart do you need a prescription for rybelsus pharmacy no prescription required

retatrutide vs semaglutide rybelsus patient assistance no prescription needed pharmacy

https://rybelsus.pro/# tirzepatide vs semaglutide weight loss

Cialis 20mg price in USA Generic Cialis without a doctor prescription Tadalafil Tablet

https://cialis.sbs/# buy cialis pill

rybelsus fda approval diabetes rybelsus como tomar rybelsus para adelgazar

rybelsus 7mg weight loss how much is rybelsus with medicare top-rated online pharmacies

https://rybelsus.pro/# how much is rybelsus

Cheap generic Viagra online sildenafil over the counter Sildenafil Citrate Tablets 100mg

https://viagra.onl/# Cheap generic Viagra online

rybelsus) semaglutide diet plan menu best online pharmacy no prescription

https://viagra.onl/# viagra canada

rybelsus dosages manufacturer coupon for rybelsus legal online pharmacy

https://cialis.sbs/# Buy Tadalafil 20mg

Cheap generic Viagra Viagra online price order viagra

Generic Cialis price Generic Tadalafil 20mg price Buy Tadalafil 5mg

https://viagra.onl/# Cheapest Sildenafil online

semaglutide 14 mg tablet cost rybelsus how to take worldwide pharmacy online

https://viagra.onl/# Viagra online price

https://cialis.sbs/# Generic Cialis price

rybelsus active ingredient how many mg is 60 units of semaglutide foreign online pharmacy

https://bestbetgiris.online# pusulabet

Cialis over the counter Cialis without a doctor prescription Cheap Cialis

bahiscasino güncel giriş bahiscasino resmi giriş

https://casivipgiris.site# bahiscasino

bahiscasino giris: bahiscasino resmi giriş

https://casivipgiris.site# bahiscasino

pusulabet giriş: pusulabet güncel giriş

pusulabet resmi giriş pusulabet giriş

bahiscasino güncel: bahiscasino güncel giriş

https://bestbetgiris.online# pusulabet giriş

https://easyindiameds.com/# indian pharmacies safe

indianpharmacy com: mail order pharmacy india – pharmacy online

Easy Mex Meds: pharmacys in mexico – Easy Mex Meds

ed meds online canada: Easy Canada Meds – trusted canadian pharmacy

mail order pharmacy india Easy India Meds foreign online pharmacy

mail order pharmacies: Easy Mex Meds – mexican pharmacy online

Easy Canada Meds: Easy Canada Meds – onlinecanadianpharmacy 24

Easy Canada Meds п»їcanadian pharmacy uk delivery buying drugs from canada

http://easyindiameds.com/# п»їlegitimate online pharmacies india

Easy Canada Meds: Easy Canada Meds – online pharmacy canada

Online medicine home delivery: Easy India Meds – online pharmacy without prescription

online drugs order mexico online pharmacy pharmacy online

best india pharmacy: Easy India Meds – reputable overseas online pharmacies

top online pharmacy india: india pharmacy – legit online pharmacy

Easy Mex Meds: best pharmacy in mexico – Easy Mex Meds

top 10 pharmacies in india buy medicines online in india online pharmacy

online mexican pharmacy: online drugs order – Easy Mex Meds

https://easyindiameds.com/# india online pharmacy

my canadian pharmacy review: canada ed drugs – canadian pharmacies online

Easy Mex Meds Easy Mex Meds Easy Mex Meds

Easy Canada Meds: Easy Canada Meds – canada ed drugs

pharmacy website india: Easy India Meds – top online pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

canada drugs online Easy Canada Meds global pharmacy canada

pharmacy website india: online pharmacy india – reputable online pharmacy no prescription

http://easycanadameds.com/# pharmacy wholesalers canada

india pharmacy: indian pharmacy paypal – buy online medicine

buy medicines online in india mail order pharmacy india no rx needed pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

pharmacy mexico: Easy Mex Meds – Easy Mex Meds

canadian pharmacy scam Easy Canada Meds Easy Canada Meds

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

Easy Mex Meds: mexico farmacia – Easy Mex Meds

cheapest online pharmacy india: Easy India Meds – international drug mart

canadian online pharmacy reviews Easy Canada Meds canada pharmacy 24h

https://easycanadameds.com/# canadian online pharmacy no prescription

legitimate canadian pharmacies: canadian online drugstore – Easy Canada Meds

Easy Canada Meds: reliable canadian pharmacy – onlinecanadianpharmacy 24

mexican medicine mexico online pharmacy Easy Mex Meds

Easy Canada Meds: canadapharmacyonline – Easy Canada Meds

Easy Mex Meds: mexico pharmacy price list – mexico pharmacy order online

world pharmacy india: Easy India Meds – best online pharmacy no prescription

best india pharmacy Easy India Meds buy online medicine

affordable pharmacy: best online mexican pharmacy – Easy Mex Meds

https://easymexmeds.shop/# mexico online farmacia

п»їlegitimate online pharmacies india Easy India Meds international pharmacy

online shopping pharmacy india: indian pharmacy – no rx needed pharmacy

india pharmacy: Easy India Meds – online pharmacies

Easy Canada Meds Easy Canada Meds canadian pharmacy online store

safe reliable canadian pharmacy: pharmstore canada – canada discount pharmacy

Easy Mex Meds: mexico drug store – mexico medication

escrow pharmacy canada canadian pharmacy world reviews Easy Canada Meds

Easy Canada Meds: Easy Canada Meds – canadian pharmacies

Easy Canada Meds: recommended canadian pharmacies – canada drugs online reviews

http://easymexmeds.com/# Easy Mex Meds

best online pharmacy india best india pharmacy legitimate online pharmacy

canadian pharmacies: Easy Canada Meds – Easy Canada Meds

top 10 pharmacies in india: indian pharmacy online – best online pharmacy

п»їlegitimate online pharmacies india top 10 pharmacies in india online pharmacy

Easy Canada Meds: Easy Canada Meds – canada drugs online review

indian pharmacy paypal: Easy India Meds – online pharmacy without prescription

reputable indian pharmacies cheapest online pharmacy india online pharmacy discount code

top 10 online pharmacy in india: indian pharmacy paypal – best mail order pharmacy

online shopping pharmacy india: Easy India Meds – shop medicine online

https://easymexmeds.shop/# Easy Mex Meds

indian pharmacy online Easy India Meds medicine online

Easy Mex Meds: worldwide pharmacy – pharmacys in mexico

Easy Mex Meds: mexican pharmacies that ship to the united states – mail order pharmacy mexico

reputable indian pharmacies Easy India Meds pharmacy online

Easy Mex Meds: Easy Mex Meds – Easy Mex Meds

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

Easy Mex Meds Easy Mex Meds Easy Mex Meds

http://easymexmeds.com/# Easy Mex Meds

pharmacy website india: Easy India Meds – shop medicine online

Easy Canada Meds: reddit canadian pharmacy – Easy Canada Meds

northwest pharmacy canada www canadianonlinepharmacy northwest pharmacy canada

reputable indian online pharmacy: indian pharmacies safe – online drugs order

Easy Canada Meds: canadian pharmacy com – canadian drug

Online medicine order world pharmacy india shop medicine online

best india pharmacy: Easy India Meds – overseas pharmacy no prescription

los algodones pharmacy online: farmacia mexicana online – Easy Mex Meds

order medication from mexico Easy Mex Meds Easy Mex Meds

http://easyindiameds.com/# mail order pharmacy india

mexican mail order pharmacy: medications can i buy mexico – affordable pharmacy

canadian pharmacies shipping to usa Easy Canada Meds Easy Canada Meds

canadian pharmacy reviews: Easy Canada Meds – Easy Canada Meds

indian pharmacy online: top online pharmacy india – us pharmacy no prescription

Easy Mex Meds: Easy Mex Meds – reliable rx pharmacy

https://easyindiameds.shop/# buy medicines online in india

mail order pharmacy india top 10 pharmacies in india overseas online pharmacy

world pharmacy india: Easy India Meds – legal online pharmacy

Easy Canada Meds: Easy Canada Meds – Easy Canada Meds

indian pharmacies safe best online pharmacy india new pharmacy online

indian pharmacy paypal: best india pharmacy – express scripts mail order pharmacy

progreso mexico pharmacy online: Easy Mex Meds – mexican meds

india online pharmacy online pharmacy india online pharmacies

https://easyindiameds.com/# indian pharmacies safe

online pharmacy india: world pharmacy india – medicine online order

Easy Canada Meds: Easy Canada Meds – trusted canadian pharmacy

Easy Canada Meds canadian pharmacy oxycodone Easy Canada Meds

canadapharmacyonline com: canadian 24 hour pharmacy – Easy Canada Meds

top 10 pharmacies in india: Easy India Meds – legal online pharmacy

Easy Mex Meds mexican drug stores mexican pharmacy near me

canada drugs online review: Easy Canada Meds – Easy Canada Meds

https://easycanadameds.shop/# Easy Canada Meds

farmacias online usa: Easy Mex Meds – mexico medicine

indian pharmacy paypal Easy India Meds no script pharmacy

reputable canadian online pharmacy: pharmacy wholesalers canada – Easy Canada Meds

canadian pharmacy world: Easy Canada Meds – Easy Canada Meds

п»їlegitimate online pharmacies india buy prescription drugs from india shop medicine online

stendra fresh pharm online pharmacy

pharmacy fresh pharm safe online pharmacies

https://freshpharm24.com/ online pharmacy no rx

Fresh Pharm online pharmacy without scripts

https://freshpharm24.com/product/viagra pharmacy no prescription required

online pharmacy secure medical online pharmacy

https://freshpharm24.com/product/viagra online pharmacy no prescription needed

generic viagra online pharmacy without scripts

online pharmacy reliable online pharmacy

Fresh Pharm online pharmacy without scripts

https://freshpharm24.com/product/cialis no prescription needed pharmacy

Fresh Pharm shop medicine online

https://freshpharm24.com/ online pharmacy without prescription

https://freshpharm24.com/ pharmacy websites

pharmacy legal online pharmacies in the us

viagra fresh pharm best online pharmacy

Fresh Pharm best online pharmacy

https://freshpharm24.com/product/stendra online pharmacy

Fresh Pharm 24 trusted online pharmacy

https://freshpharm24.com/ top-rated online pharmacies

https://freshpharm24.com/ worldwide pharmacy online

Fresh Pharm 24 best online pharmacy

online pharmacy overseas online pharmacy

https://freshpharm24.com/ online pharmacy no rx

Fresh Pharm 24 foreign online pharmacy

generic stendra online pharmacy without scripts

https://freshpharm24.com/ legal online pharmacy

generic stendra online pharmacy without prescription

https://freshpharm24.com/ worldwide pharmacy online

https://freshpharm24.com/product/norvasc overseas online pharmacy

Fresh Pharm 24 no prescription pharmacy paypal

online pharmacy pharmacy no prescription required

https://freshpharm24.com/product/norvasc online pharmacy discount code

Fresh Pharm best mail order pharmacy

generic norvasc no rx needed pharmacy

Cialis 20mg price in USA Buy Cialis online Generic Cialis without a doctor prescription

https://sildenafilvip.shop/# Viagra Tablet price

https://sildenafilvip.shop/# Sildenafil Vip

best price for viagra 100mg Sildenafil Vip Cheap generic Viagra online

https://cialisvip.online/# Buy Tadalafil 20mg

Buy Tadalafil 5mg Cialis Vip buy cialis pill

https://sildenafilvip.com/# Generic Viagra for sale

http://cialisvip.com/# Buy Tadalafil 5mg

ivermectin for sale stromectol Vip stromectol cream

Generic Viagra online Sildenafil Vip Viagra generic over the counter

http://sildenafilvip.com/# cheapest viagra

https://sildenafilvip.com/# Sildenafil Vip

Generic Cialis price Tadalafil Tablet Cialis over the counter

https://sildenafilvip.shop/# Sildenafil Vip

http://stromectolvip.com/# ivermectin 500ml

Viagra Tablet price over the counter sildenafil Order Viagra 50 mg online

cheapest cialis Cialis Vip п»їcialis generic

http://stromectolvip.com/# ivermectin 3 mg tablet dosage

https://sildenafilvip.com/# buy Viagra over the counter

ivermectin canada stromectol Vip ivermectin 5

http://sildenafilvip.com/# Sildenafil Vip

https://sildenafilvip.com/# Sildenafil Vip

Cialis over the counter Cialis without a doctor prescription Buy Cialis online

http://cialisvip.com/# Cialis Vip

Tadalafil price Cialis over the counter Buy Cialis online

https://stromectolvip.online/# ivermectin oral solution

cheapest cialis Generic Tadalafil 20mg price Buy Cialis online

https://stromectolvip.com/# ivermectin pills human

https://sildenafilvip.com/# Sildenafil Vip

Cheap Viagra 100mg Sildenafil Vip Viagra tablet online

https://cialisvip.online/# Buy Tadalafil 20mg

https://cialisvip.com/# Buy Cialis online

order viagra Generic Viagra for sale viagra canada

http://stromectolvip.com/# stromectol cvs

Tadalafil price Buy Cialis online Cialis over the counter

https://sildenafilvip.com/# best price for viagra 100mg

ivermectin drug ivermectin cream canada cost stromectol ivermectin tablets

https://sildenafilvip.shop/# Sildenafil Vip

Generic Viagra for sale Viagra online price over the counter sildenafil

Generic Cialis without a doctor prescription Cialis Vip Tadalafil Tablet

http://cialisvip.com/# Cialis Vip

Buy Tadalafil 5mg Cialis without a doctor prescription Cialis over the counter

https://sildenafilvip.com/# Sildenafil Vip

http://cialisvip.com/# Cialis Vip

cialis for sale Tadalafil price Tadalafil price

buy ivermectin for humans uk ivermectin price canada stromectol over the counter

https://cialisvip.online/# Generic Cialis price

https://stromectolvip.com/# stromectol 12mg

ivermectin 3 mg stromectol Vip purchase oral ivermectin

https://stromectolvip.online/# ivermectin generic name

ivermectin 9 mg stromectol Vip ivermectin stromectol

https://stromectolvip.com/# ivermectin 3mg tablets

Tadalafil Tablet Cialis Vip Cialis 20mg price in USA

http://cialisvip.com/# Buy Tadalafil 10mg

ivermectin stromectol how much does ivermectin cost stromectol cost

https://stromectolvip.online/# cost of ivermectin pill

ivermectin buy online stromectol Vip stromectol how much it cost

ivermectin oral oral ivermectin cost ivermectin brand

https://cialisvip.com/# Buy Tadalafil 10mg

cheapest cialis Cialis Vip Cialis 20mg price

https://semaglutideglp1.shop/# rybelsus class

glp-1 victoza liraglutide pharmacy

online pharmacy discount code pharmacy no prescription required online pharmacy discount code

http://victopharm.com/# legal online pharmacies in the us

us pharmacy no prescription Victo Pharm online pharmacy no rx

glp 1 LiraglutideGlp1 liraglutide pharmacy

does rybelsus work for weight loss semaglutide glp1 can you just stop taking rybelsus

https://victopharm.com/# reliable online pharmacy

overseas pharmacy no prescription Victo Pharm top online pharmacy

https://liraglutideglp1.shop/# victoza weight loss

cheap victoza cheap victoza buy liraglutide online

trusted online pharmacy Victo Pharm online pharmacy without scripts

https://semaglutideglp1.com/# rybelsus is used for

trustworthy online pharmacy Victo Pharm best rx pharmacy online

victoza generic LiraglutideGlp1 generic liraglutide

top online pharmacy online pharmacy no prescription needed foreign online pharmacy

https://semaglutideglp1.shop/# is rybelsus used for weight loss

pharmacy order online Victo Pharm new pharmacy online

http://liraglutideglp1.com/# buy victoza online

can you cut rybelsus in half glp-1 drugs for weight loss semaglutide otc equivalent

hair loss semaglutide glp-1 rybelsus used for weight loss

https://semaglutideglp1.shop/# п»їrybelsus

liraglutide otc LiraglutideGlp1 buy liraglutide

https://liraglutideglp1.shop/# cheap victoza

semaglutide missed dose side effects glp-1 rybelsus 9mg

https://victopharm.shop/# legal online pharmacies in the us

online pharmacy without prescription Victo Pharm legit online pharmacy

trusted online pharmacy no script pharmacy best rx pharmacy online

no rx needed pharmacy Victo Pharm online pharmacy no prescription

buy Viagra online Buy Viagra online cheap – generic sildenafil

https://urohealthdaily.com/# Sildenafil 100mg price

Viagra tablet online buy Viagra over the counter – over the counter sildenafil

Cheap generic Viagra online buy Viagra over the counter sildenafil over the counter

viagra canada buy viagra here – Viagra online price

Viagra tablet online Sildenafil 100mg price – viagra without prescription

https://urohealthdaily.shop/# Viagra online price

best price for viagra 100mg UroHealth Daily – Generic Viagra online

Viagra Tablet price generic sildenafil – generic sildenafil

best price for viagra 100mg UroHealth Daily – Order Viagra 50 mg online

buy viagra here Cheap generic Viagra – Cheap Viagra 100mg

buy Viagra over the counter Sildenafil 100mg price – Cheapest Sildenafil online

https://urohealthdaily.com/about-to-buy-viagra-read-this-first/# viagra without prescription

Viagra tablet online UroHealth Daily – Buy Viagra online cheap

Cheapest Sildenafil online UroHealth Daily – Cheapest Sildenafil online

Buy Viagra online cheap Order Viagra 50 mg online – Buy generic 100mg Viagra online

Cheap generic Viagra online UroHealth Daily – Order Viagra 50 mg online

viagra without prescription sildenafil 50 mg price Viagra tablet online

Cheap generic Viagra online UroHealth Daily – Generic Viagra online

Generic Viagra for sale UroHealth Daily – viagra canada

Sildenafil 100mg price sildenafil online – Order Viagra 50 mg online

Tadalafil Tablet Buy Tadalafil 20mg – Buy Tadalafil 10mg

http://mensrxguide.org/# Buy Tadalafil 10mg

Generic Cialis price MensRxGuide Cialis over the counter

Buy Tadalafil 5mg MensRxGuide – cheapest cialis

Cialis 20mg price in USA Cialis 20mg price – cheapest cialis

Cialis without a doctor prescription http://mensrxguide.org/# Tadalafil price

https://mensrxguide.org/# Buy Cialis online

cialis for sale MensRxGuide – Buy Tadalafil 5mg

Generic Cialis price MensRxGuide – Tadalafil Tablet

Generic Tadalafil 20mg price https://mensrxguide.org/# Generic Tadalafil 20mg price

Buy Tadalafil 10mg Generic Cialis price – Buy Tadalafil 20mg

cheapest cialis MensRxGuide Buy Cialis online

Generic Cialis price Buy Tadalafil 5mg – Buy Tadalafil 20mg

Cialis without a doctor prescription http://mensrxguide.org/# Cialis over the counter

https://mensrxguide.org/# п»їcialis generic

buy cialis pill MensRxGuide – Tadalafil price

cialis for sale Cialis 20mg price in USA – Tadalafil Tablet

Cialis without a doctor prescription MensRxGuide – Tadalafil price