A solid calculation of your home financing is the first step towards home ownership. There are four crucial components at the beginning: the purchase price, your equity, the interest rate and the repayment. These four factors are the be-all and end-all, as they determine what you pay each month and how high the total costs for your dream home will be.

Understanding the foundation of your home financing

The dream of owning your own four walls often still feels a long way off until you put it into concrete figures. So before we dive into the calculation formulas, we need to get the basics right. This is really important, because only those who know the cornerstones of their financing can confidently evaluate offers and set the right course for the future.

Precise planning is now more important than ever, as the cost of owning a home in Germany continues to rise. A study by the German Economic Institute (IW) predicts an average price per square meter of 3,081 euros by 2025. This shows how crucial it is to calculate the financing for your home precisely in order to be on a secure footing. You can find out more about price trends directly in the “Housing in Germany 2025” study by the IW Cologne.

The four pillars of your calculation

Every home loan is based on four components that interlock like cogwheels. Let’s take a closer look:

- The purchase price: This is the amount you put on the table for the property itself. But be careful: don’t forget the incidental purchase costs! Land transfer tax, notary and estate agent fees are added on top and can really push up the total amount you need.

- Your equity: This is the money you have saved and which you put directly into the purchase. More equity is always better – it not only lowers the loan amount you need, but also strengthens your negotiating position with the bank. A good rule of thumb is at least 20% of the purchase price.

- The borrowing rate: This is effectively the “net price” charged by the bank for the money borrowed. It is the basis for calculating interest, but it is not the whole truth, as there are no other fees.

- The initial repayment: This percentage indicates how much of the loan you repay in the first year. A higher repayment rate, for example 2% instead of 1%, makes a huge difference: it noticeably shortens the term and saves you a lot of interest costs over the years.

A higher equity ratio is your strongest lever. It not only reduces the risk for the bank, which leads to better interest rates, but also lowers your monthly installment and makes you debt-free faster.

Target interest rate versus effective interest rate: what’s the difference?

This is where many people stumble when comparing offers: the difference between the borrowing rate and the effective interest rate. The borrowing rate often looks temptingly low on paper, but the really decisive factor is the APR.

Why? Because it includes most additional costs and fees, such as processing fees, in addition to the pure borrowing rate. The effective interest rate therefore shows you the actual annual costs of the loan. It is the only way to compare different offers fairly and transparently.

This is precisely why a comprehensive comparison of different financing offers is so incredibly important. In our next article, we explain why a thorough comparison is so important when it comes to real estate financing and how you can best proceed.

Let’s get specific: How to calculate your monthly loan installment

Enough theory, now it’s time to get down to business. We want to make the numbers dance and make the calculation of your home financing really tangible. The linchpin of every calculation is the so-called annuity – the fixed monthly installment, which is made up of an interest and a repayment component.

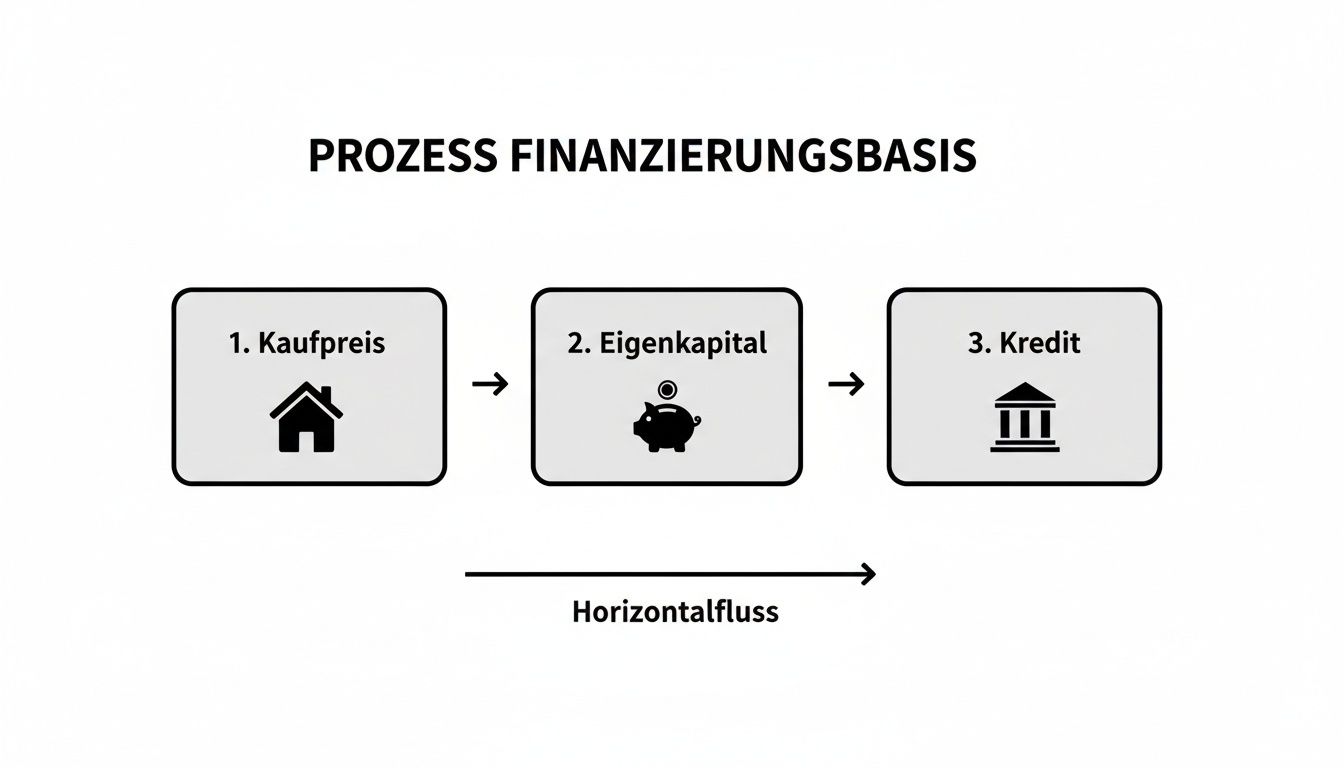

To bring the whole thing to life, let’s simply follow a fictitious family on their journey to home ownership. Let’s say the Meier family has found their dream home for €400,000 and has a solid €80,000 in equity. The first, decisive step is always to reduce the purchase price by the equity. This results in the amount they really need from the bank.

This diagram shows the simple but basic process at a glance:

You can see immediately that the actual loan amount, the so-called net loan, is the true starting point for any further calculation.

The net loan as a starting point

So first we determine how much money the Meier family actually needs to borrow from the bank. The calculation is very simple:

- Purchase price: € 400,000

- Equity: – € 80,000

- Net loan amount: € 320,000

Exactly this €320,000 is the sum to which interest and repayment will later relate. We deliberately leave out the ancillary purchase costs at this point – for good reason. My practical advice: Ideally, these should always be paid in full from the equity capital to avoid taking on even more debt.

Interest and amortization – the two decisive levers

Now the two most important factors for your monthly installment come into play: the interest rate and the initial repayment. For our example, we will use realistic conditions. Assuming the Meier family concludes their financing in April 2025, they could expect a borrowing rate of 3.7% per year for a 10-year fixed interest rate. This is a realistic figure that reflects the market situation. Although current building interest rates have stabilized, they are trending slightly upwards.

The Meier family opts for an annual repayment rate of 2%. This is a solid figure that I often recommend. It ensures a steady reduction in debt without immediately driving up the monthly burden immeasurably.

With these two values, we can easily calculate the load:

- Annual interest component: € 320,000 × 3.7 % = € 11,840

- Annual repayment portion: € 320,000 × 2.0 % = € 6,400

Both amounts together make up the total annual payment, also known as the annuity.

Annual annuity: €11,840 (interest) + €6,400 (repayment) = €18,240

Monthly installment: €18,240 / 12 months = €1,520

The Meier family would therefore have to plan with a monthly installment of €1,520. This amount remains exactly the same over the entire 10-year fixed interest period. This creates planning security.

The clever effect: how interest and repayment shift

The real genius of an annuity loan happens inside this constant installment. With each individual payment, you pay off a small part of your debt. This minimizes the interest portion of the next instalment, as the interest is only ever calculated on the remaining debt.

However, because the installment remains constant, your repayment portion automatically increases by exactly the amount by which the interest portion has decreased. You therefore pay off your debts faster and faster over time – a turbo effect that really becomes noticeable over the years!

A good loan comparison not only helps you to find the best interest rate, but also a repayment structure that suits you perfectly. If you want to delve deeper into the topic, you can find out how to easily find the best deal when comparing loans in our article.

The residual debt at the end of the fixed interest period

The residual debt is an absolutely crucial value when calculating your home loan. It tells you how much is still outstanding at the end of the fixed interest period. You will then need follow-up financing for this amount – at the interest rate conditions that apply on the market at that time.

Let’s take a look at our example after 10 years. The following table clearly summarizes the most important key data.

Example calculation for a house financing of €320,000

This table shows the breakdown of the monthly installment and the development of the residual debt for an example scenario.

| Parameters | Value |

|---|---|

| Net loan | 320.000 € |

| Debit interest p.a. | 3,70 % |

| Initial repayment p.a. | 2,00 % |

| Monthly installment | 1.520 € |

| Repayment made after 10 years | approx. 76,500 € |

| Residual debt after 10 yrs. | approx. 243,500 € |

The result is impressive: after 10 years, the Meier family would have already paid off over €76,000 of their loan. The remaining debt of around €243,500 would then be the basis for the new financing round. And a simple rule applies here: the lower this residual debt is, the more relaxed and stronger your negotiating position with the bank will be.

Uncover hidden costs and plan correctly

The purchase price alone is only half the battle. I have often experienced this in my career: many prospective owners are so focused on the large sum for the property that they overlook one of the most expensive traps – the ancillary purchase costs.

These additional items are anything but peanuts. Realistically calculate a surcharge of 10 % to 15 % on the purchase price. This is a huge sum that can cause your financing requirements to skyrocket and throw your entire planning out of kilter.

And here’s the catch: banks are extremely reluctant to finance these additional costs. They almost always assume that you will cover these expenses entirely from your equity. This protects the bank, but for you it means that your buffer must be full to bursting.

The three major ancillary costs in detail

Let’s take a closer look at these “hidden” costs. Basically, there are three major items that you cannot avoid when buying real estate in Germany.

1. the real estate transfer tax

This is often the biggest chunk and varies from state to state. The tax is due on the price stated in the purchase contract and goes directly to the tax office. Only once this has been paid is the so-called clearance certificate issued – without which no transfer in the land register can take place.

- In Bavaria, you are still doing well with 3.5%.

- In North Rhine-Westphalia and Brandenburg, the tax authorities are charging a whopping 6.5%.

This difference alone amounts to €12,000 for a €400,000 house!

2. notary and land registry costs

Nothing works in Germany without a notary. He draws up the purchase contract and ensures that it is legally watertight. He also takes care of the necessary entries in the land register.

You can roughly expect to pay 1.5 % to 2.0 % of the purchase price for this service. Part of this goes to the notary, the other to the land registry for the transfer of ownership and the registration of the land charge for the bank.

3. the broker’s commission

If a real estate agent was involved, they naturally want to be paid too. Since a change in the law at the end of 2020, buyers and sellers share the commission fairly. The exact amount is a matter of negotiation, but as a buyer you usually end up with 2.5% to 3.57% including VAT.

In the case of our example financing with a purchase price of €400,000 in North Rhine-Westphalia, this quickly adds up to over €44,000 in additional costs. This amount must be in addition to the purchase price and dramatically increases the total requirement.

Service charges calculated in the example scenario

Let’s stay with our Meier family and the €400,000 house in NRW. This is how the ancillary costs really come into play here:

| Cost type | Percentage | Amount in Euro |

|---|---|---|

| Real estate transfer tax | 6,50 % | 26.000 € |

| Notary & land registry costs | approx. 1.50 % | 6.000 € |

| Broker commission | 3,57 % | 14.280 € |

| Total ancillary costs | – | 46.280 € |

Whoosh – the actual capital requirement is no longer €400,000, but €446,280. When the Meier family contributes their €80,000 in equity, these ancillary costs are deducted first. This naturally reduces the amount that goes directly towards repaying the house. This makes it all the more important to plan cleverly right from the start. You can find out how to best prepare for the bank interview in our guide on tips and tricks for a successful loan application.

Don’t forget running costs after moving in

Handing over the keys is not the end of the story. As the owner, you will be faced with ongoing costs that will add to your monthly mortgage payment. You must include these in your household budget:

- Property tax: An annual levy to the municipality.

- Homeowners insurance: Absolutely essential to protect yourself against damage caused by fire, storm or water.

- Operating costs: Think of garbage collection, water, sewage, chimney sweeps and so on.

- Maintenance reserve: A golden rule from practice: set aside €1.50 to €2.00 per square meter per month for future repairs. A new roof or heating system is bound to come at some point.

Only if you really include all these items – the one-off ancillary costs and the ongoing expenses – in your home financing calculation will you have an honest picture of your financial future and avoid any nasty surprises.

Clever use of special repayments and subsidies

When you calculate your home financing, the result is not a rigid formula that is set in stone for the next few decades. Think of it more like a dynamic plan. There are a few very clever levers that you can use to actively intervene, become debt-free much faster and save thousands of euros in the process.

The two most effective instruments for this are state subsidies and the option of special repayments. They give your financing the flexibility it needs to react cleverly to a salary increase, an inheritance or a bonus. You could also say that they are the turbo for your repayment plan.

State subsidies as start-up aid

The state has an interest in people being able to fulfill their dream of owning their own home. That is why there is a whole range of subsidy programs that you should definitely be aware of. These can be low-interest loans or even direct grants that you don’t have to pay back. A solid understanding of these options is part of any good financial plan.

The first port of call is almost always the Kreditanstalt für Wiederaufbau (KfW). There is a suitable program for almost every project:

- KfW Home Ownership Program (124): This supports the purchase or construction of your owner-occupied home with a low-interest loan of up to €100,000. This is an ideal supplement to the main financing from your bank.

- Energy-efficient construction and renovation (program 261): If you build particularly energy-efficiently or make an old property fit for the future, KfW rewards this with extremely attractive loans and often also high repayment subsidies.

Important to know: You do not apply directly to KfW, but always via your house bank. And the most important thing is to submit the application before you start building or buying. So make sure you plan for these funds right from the start so that you don’t give anything away.

Special repayments: The key to rapid debt relief

While subsidies are a fantastic start-up aid, the special repayment is your wild card for the entire term. An unscheduled repayment is nothing more than a payment that you make out of turn in addition to your monthly installment. The best thing about it: 100% of every single euro goes directly towards reducing your remaining debt.

This direct deduction has enormous leverage. It immediately reduces the loan amount on which interest is due next month. This lowers your interest burden and speeds up the entire repayment process enormously.

The option to make unscheduled repayments is not a matter of course. Make sure that the loan agreement stipulates a sufficient amount of free unscheduled repayments – usually 5% of the original loan amount per year.

Let’s take a look at a concrete example. Let’s take our loan of € 320,000 with 3.7 % interest and 2 % repayment. Without any extras, the full repayment would take around 35 years.

What happens if you manage to make a special repayment of just €5,000 each year – for example from your Christmas bonus or a bonus?

- The total term is suddenly reduced from 35 years to only around 27 years. So you will be debt-free a full eight years earlier!

- The interest savings over the entire term amount to over €50,000.

These figures impressively demonstrate the power of even small but regular unscheduled repayments. It’s the most direct way to actively reduce the cost of your home loan and achieve financial freedom faster. If you want to delve deeper into the basics of different types of loans, take a look at our article on everything you need to know about installment loans.

Choosing the right financing partner

So, the figures are finalized, the ancillary costs have been factored in and the special repayments have already been booked in your mind – your home financing is perfectly calculated. Congratulations! But to be honest, that was just the compulsory part. Now comes the freestyle and perhaps the most important decision on your way to home ownership: choosing the right financing partner.

The market is a veritable jungle of offers from house banks, nimble direct banks, building societies and independent brokers. Everyone lures you in with the supposedly best interest rate. But don’t be dazzled by the large number in front of the decimal point. There is so much more to it than that.

More than just the borrowing rate counts

One mistake that I see again and again in my practice is the almost hypnotic fixation on the borrowing rate. At first glance, an offer can seem unbeatably cheap, but on closer inspection it turns out to be an expensive trap due to rigid contract details. The only sensible comparison value is the effective annual interest rate, as this already includes most of the ancillary loan costs.

But even that is not the whole story. As is so often the case, the devil is in the small print. You can recognize a really good offer by the flexibility it offers you for your life.

Ask these questions before you sign anything:

- Special repayments: Can I deposit money out of turn, free of charge? How much? The minimum annual margin should be 5% of the loan amount.

- Repayment rate change: What happens if my income changes? Can the repayment rate be adjusted? Many good providers allow at least two free changes during the term.

- Commitment interest: When does the interest clock start ticking if I only need the money gradually, for example for a new build? A long period without commitment interest can save you thousands of euros.

Believe me, these points are often worth their weight in gold – much more than the last tenth of a percentage point in the interest rate.

The power of broad market comparison

In the past, the path was clear: you went to your bank. That was the first and often the last step. Today, that would be a cardinal financial mistake. The key to the best conditions lies in a comprehensive market comparison. Platforms such as Finanz-Fox open the door to offers from hundreds of banks with just a few clicks.

Imagine that: Appointments with ten different banks, submitting the same documents each time, waiting for offers. This is not only incredibly tedious, but also grueling. An independent broker takes this work off your hands.

A good financial advisor is like a personal pilot through the jungle of interest rates. He knows not only the paths, but also the shoals of the contracts and negotiates the best route for you – from the first click in the calculator to the final signature.

Current figures on real estate financing show just how dynamic the market is. In the first half of 2025, the institutions of the Association of German Pfandbrief Banks (vdp) alone granted real estate loans worth 70.1 billion euros. That is a whopping 17% increase on the previous year. The residential real estate business in particular grew strongly with an increase of 22 percent to 46 billion euros. These figures are literally crying out to take advantage of the competition. If you would like to know more about this development, the vdp provides a detailed analysis of real estate financing.

From selection to application

A competent advisor or a good comparison platform will guide you through the entire process. It starts with the initial orientation, where you run through various scenarios in the online calculator. Here you can get a feel for the figures yourself by juggling terms, repayments and equity.

As soon as the direction is clear, it’s time for the detailed planning. Your consultant will help you compile all the necessary documents, check them for completeness and submit them to the appropriate banks. This not only speeds up the process immensely, but also increases your chances of success. At the end of the process, you will receive tailor-made offers from which you can choose the best one at your leisure. A compilation of different loan providers can be very helpful to give you an initial overview.

In this way, you not only secure a top interest rate, but also financing that really suits you, your family and your future plans. And that is precisely the basis for a relaxed life in your own four walls.

Frequently asked questions about calculating home financing

After such an in-depth journey through the figures of home financing, a few very specific questions often remain unanswered. This is completely normal, because with such a big decision you simply want to be prepared for everything. I’ve put together a list of the most frequently asked questions that I’m asked again and again in consultations to take away the last uncertainties.

How high should the initial repayment really be?

This is one of the most important factors in your financing and the answer is always a bit of a balancing act. A solid rule of thumb that has proven itself over the years is to start with an initial repayment of at least 2%. This will ensure that you pay off a significant portion of the loan right from the start and not just pay interest for years.

However, especially in times of low interest rates, it can be extremely smart to be bolder and go for 3% or even more. Why? Every euro you pay off more shortens the overall term of your loan and ultimately saves you a huge amount in interest costs. Of course, a higher repayment also means a higher monthly charge. So it has to fit in with your income, your life planning and your need for security.

My practical tip: Just play it through. A good financing calculator will show you down to the cent how a small change in the repayment can pulverize your remaining debt after ten years and the total costs. This will help you find the perfect middle ground between being debt-free quickly and a rate that lets you sleep well at night.

What happens if interest rates rise after the fixed interest period?

This is probably a concern for most home builders: What if interest rates are suddenly much higher at the end of my 10- or 15-year fixed-rate period? This is a real risk. If the interest rate rises, this can push up your monthly installment for the follow-up financing significantly, even if you want to continue repaying in the same way.

Fortunately, you are not defenceless. There are proven strategies:

- Choose a long fixed interest rate: Give yourself peace of mind right from the start and opt for a fixed interest rate of 15, 20 or even 25 years. This may cost a tiny interest surcharge today, but you are buying yourself absolute planning security for an extremely long time.

- Make unscheduled repayments: As already discussed, every unscheduled repayment is a direct attack on your remaining debt. The smaller the residual debt at the end of the fixed interest period, the less painful a possible interest rate increase on the new installment will be.

- Check a forward loan: If the end of your fixed interest rate period is approaching (up to 5 years in advance is possible), you can secure today’s interest rates for the future with a forward loan. Although this is a bet on rising interest rates, it is one that can really pay off and save nerves.

Can I finance a house with little equity?

The short answer: Yes, it is possible. Financing with very little or even no equity at all is possible. This is referred to as 100% or even 110% financing if the ancillary purchase costs are also covered by the loan. But – and this is a really big but – you take on a significantly higher risk and end up paying noticeably more.

Banks pay well for the increased default risk, usually through a hefty interest premium. Your monthly installment will therefore be higher from the outset.

As an absolute minimum, you should always try to pay at least the ancillary purchase costs (expect around 10-15% of the purchase price) out of your own pocket. Financing with a solid buffer of 20% equity or more is almost invariably the safer and, over the entire term, the cheaper way to own a home.

How much house can I afford?

This question should be at the very beginning, even before you open the first real estate portal. The answer to this question can only be found in a ruthless and honest budget calculation. Sit down and compare everything that comes in with everything that goes out.

This will give you a clear picture:

- Add up your income: Net salary, any rental income, child benefit, etc.

- Deduct fixed costs: Your current rent (which is eliminated), insurance, savings plans, current loans, subscriptions.

- Estimate variable costs: Be honest about your food, leisure, car or vacation expenses. It’s easy to count yourself poor here.

- Plan a buffer: Think about unforeseen things. A buffer for a broken washing machine or car repairs is a must.

The amount that remains at the bottom line is what you would theoretically have available for a loan installment. As a rule of thumb, banks calculate a maximum monthly charge of 35-40% of the net household income. The possible loan amount can then be derived fairly accurately from this rate.

Calculating a home loan can seem like a mountain at first glance, but with the right knowledge and tools, it becomes a predictable path. Use our calculator to get a feel for your figures and test different options. At Finanz-Fox, we are happy to accompany you on this journey – from the first click to handing over the keys. Start your no-obligation comparison now at https://www.finanz-fox.de.