If you want to fulfill your dream of owning your own home, there’s one question you can’t avoid: How do I finance the whole thing on the best possible terms? The direct way to do this is to make a thorough comparison of mortgage interest rates. Instead of accepting the first best offer from your house bank, a targeted analysis can save you thousands, often even tens of thousands of euros over the entire term. Even tiny differences in interest rates on paper have a huge financial impact in practice.

Why an interest rate comparison is crucial for mortgage financing

Buying a property is probably one of the biggest financial decisions you make in your life. Understandably, many prospective owners focus almost exclusively on the purchase price of the property itself. However, an equally decisive cost factor is often pushed into the background: interest rates. However, a careful comparison of interest rates is not just a formality, but a financial necessity that will shape your budget for years to come.

Imagine for a moment that you need a loan of €300,000. An initial offer is at 3.8% interest, while another, which you receive after a thorough comparison, is at 3.3%. At first glance, this difference of 0.5 percentage points may not seem earth-shattering. In reality, however, it looks quite different.

The power of small numbers

This supposedly small difference means annual interest savings of €1,500. Over a fixed-interest period of ten years, this amount adds up to a whopping €15,000. This is money that you could use instead for unscheduled repayments, a new kitchen or simply for your general quality of life.

The current market conditions make this range all too clear. Depending on the fixed interest rate and loan-to-value ratio, top construction interest rates currently range between 3.38% and 4.13% effectively per year. A comparison of Finanztip data shows that even with the same credit rating and region, interest rates can vary by 0.5 percentage points – which amounts to tens of thousands of euros for a €300,000 loan over ten years. You can read detailed insights into current interest rate developments on this page about mortgage interest rates.

More than just the interest rate

However, a really good comparison goes beyond the mere percentage value. It helps you to find the conditions that exactly match your life situation. Flexible repayment options or the possibility of free special repayments can be just as valuable in the end as a tenth of a percent less interest.

The best interest rate is always the one that best suits your personal life planning and financial situation. A good comparison therefore takes into account not only the figures, but also the flexibility of the contract.

This guide takes you by the hand and leads you through the process step by step. We clarify which factors really influence your interest rate and how to evaluate offers correctly without comparing apples with oranges. Incidentally, the principle of gaining an advantage through a deeper understanding of expenses applies in many areas. Find out, for example, how you can also understand and save costs in other areas.

With the right information, you can make an informed and, above all, cost-saving decision for your own home. You can also read why a comparison is always worthwhile when it comes to real estate financing in our related article: https://www.finanz-fox.de/immobilienfinanzierung-warum-ein-vergleich-sich-lohnt/

Debit interest and effective interest – what really counts

Anyone looking for a mortgage will quickly be confronted with two terms: borrowing rate and effective interest rate. They sound similar, but the small difference between them determines what your loan will really cost in the end. It is absolutely crucial to know this difference before even putting two offers side by side.

The borrowing rate – formerly known as the nominal interest rate – is more or less the pure price that the bank charges for the money borrowed. It only shows the interest costs on the remaining debt. Of course, many providers advertise the lowest possible borrowing rate, because at first glance the figure simply looks unbeatably good.

But in all honesty, this value is only half the truth. Another value comes into play in order to grasp the actual financial burden.

Why the effective interest rate is the better compass

The APR is the figure you really need to pay attention to. It is much more honest because it includes most of the ancillary costs of the financing in addition to the borrowing rate. It is even required by law to be used when comparing loans – and for good reason.

Typically, the effective interest rate includes costs such as these:

- Processing fees (rare these days, but they still exist)

- Possible brokerage commissions

- Fees for maintaining the loan account

- The offsetting of the repayment, which affects the interest burden

Don’t be fooled by a low borrowing rate. Only the effective interest rate allows a real apples-to-apples comparison, because it already reveals most of the additional costs. If you ignore it, you will end up paying more.

Imagine the following scenario: Bank A entices you with a borrowing rate of 3.5%, but charges a hefty processing fee. Bank B offers a “worse” 3.6% borrowing rate on paper, but waives such fees completely. If you add everything up, Bank A’s effective interest rate could be 3.75%, while Bank B actually has the more favorable offer at 3.65%.

The hidden costs that even the effective interest rate does not show

As informative as the effective interest rate is, it is not an all-inclusive figure. A few cost factors are left out and can make your financing more expensive than expected. So always take a critical look at the small print and keep an eye out for them:

- Commitment interest: This interest is due if you do not draw down the loan in full within a certain period (often 3 to 12 months). This is a common cost trap, especially for new builds.

- Costs for the land charge entry: The notary and land registry fees are always added on top.

- Valuation costs: Sometimes the bank charges a fee for the valuation of your property.

- Partial payment surcharges: If the money is paid in installments – depending on the progress of construction, for example – extra costs may be incurred.

A really good comparison of mortgage interest rates therefore means: take the effective interest rate as a starting point, but ask specifically about all other possible costs. This is the only way to get a feel for the real total costs. You can also find more practical tips on this in our article on comparing interest rates.

Which factors shape your personal interest rate

When you compare mortgage rates, you quickly realize that there is no one interest rate that fits all. Your personal offer is rather a tailor-made result that is made up of several key factors. You can think of it like a chef whipping up a dish from various ingredients – the bank mixes these factors to assess the risk and therefore your interest rate.

The good thing is that these parameters are not rigid specifications, but active levers. If you understand how they work, you can improve your starting position in a targeted manner and often secure significantly better conditions. Let’s take a closer look at the four most important pillars of your financing.

Fixed interest rates: security versus flexibility

The fixed interest rate determines how long the agreed interest rate remains unchanged for you – periods of 10, 15 or 20 years are common. It can be seen as your protective shield against rising interest rates on the market. A long fixed interest rate gives you maximum planning security because your monthly installment remains absolutely constant over this long period.

However, this security comes at a price. Banks often charge a small interest premium for the promise of a fixed interest rate. Financing with a 20-year fixed interest rate will therefore generally have a slightly higher interest rate than one with only 10 years. The right choice depends heavily on the current interest rate landscape and your personal risk tolerance.

- Long fixed interest period (15+ years): This is the ideal choice in low-interest phases to secure favorable conditions for an eternity. Particularly recommended for security-oriented people who don’t want any nasty surprises when it comes to follow-up financing.

- Short fixed interest period (5-10 years): An option in high-interest phases if you are speculating that interest rates will fall again in the future. This gives you more flexibility, but carries the risk of significantly more expensive follow-up financing if interest rates do rise.

The loan-to-value ratio: Your equity as leverage

The loan-to-value ratio is one of the most important key figures for the bank. It simply describes the ratio of the loan amount to the value of your property, expressed as a percentage. The more equity you have, the lower the loan-to-value ratio – and logically the lower the risk for the bank. This lower risk is directly rewarded with a better interest rate.

A high equity ratio is the strongest lever for a top interest rate. There are often significant jumps in interest rates when loan-to-value ratios fall below 90%, 80% or 60%.

Just a few thousand euros more equity can push you over this magic threshold and save you a considerable amount of interest over the years. It is therefore worth checking very carefully beforehand whether all sources of equity (savings, building society savings contracts, securities) have really been exhausted.

The repayment amount: the turbo to debt freedom

The initial repayment determines how quickly you repay your loan. Of course, a higher repayment rate initially means a higher monthly installment. However, it reduces the remaining debt much faster. The bottom line is that you pay considerably less interest over the entire term and are debt-free much sooner.

Especially in times of low interest rates, an initial repayment of at least 2%, or even better 3%, is highly recommended. A low repayment of just 1% may seem tempting at first glance because the rate is so low. However, it extends the term to over 35 years and drives up the interest costs enormously.

The following table uses the example of a €300,000 loan at 3.5% interest to show the impact of the repayment rate.

How the repayment rate affects your interest costs

| Initial repayment | Monthly installment | Residual debt after 10 years | Interest paid after 10 years |

|---|---|---|---|

| 1 % | 1.125,00 € | 263.818 € | 98.818 € |

| 2 % | 1.375,00 € | 227.636 € | 95.136 € |

| 3 % | 1.625,00 € | 191.455 € | 91.455 € |

You can clearly see that a higher repayment not only leads to a much lower residual debt, but also saves money on interest costs – even in the first ten years alone.

Your credit rating: the foundation of trust

Last but not least, your personal financial situation – your credit rating– plays a decisive role. The bank checks very carefully how reliable you are as a borrower. A stable, high income, a secure job and a clean SCHUFA report are worth their weight in gold here.

This has a positive impact on your credit rating in the eyes of the bank:

- An open-ended employment contract (preferably outside the probationary period)

- A high and regular household income

- No negative SCHUFA entries

- Little to no further consumer credit

Before obtaining offers, you should get your finances in order and perhaps cancel unnecessary loans or unused credit cards. Good preparation can translate directly into a better interest rate offer. You can find comprehensive advice on how to optimize your application in our guide on tricks for a successful loan application.

Compare offers: This strategy will help you find the best overall package

Okay, you’ve got the theory down. You now know which levers are decisive for a mortgage. But how do you proceed in practice when the first offers are on the table? Now it’s getting serious, and a good strategy is worth its weight in gold. It’s not just about chasing the lowest interest rate, but finding the package that really suits you and your life.

The first step is proper preparation. Before you jump into a comparison calculator like the one from Finanz-Fox, you need a solid database. Get everything ready: proof of income, an honest statement of your own capital and a current SCHUFA report. The more accurate your figures are right from the start, the more reliable the first interest rate indications you receive will be.

More than just the number on paper

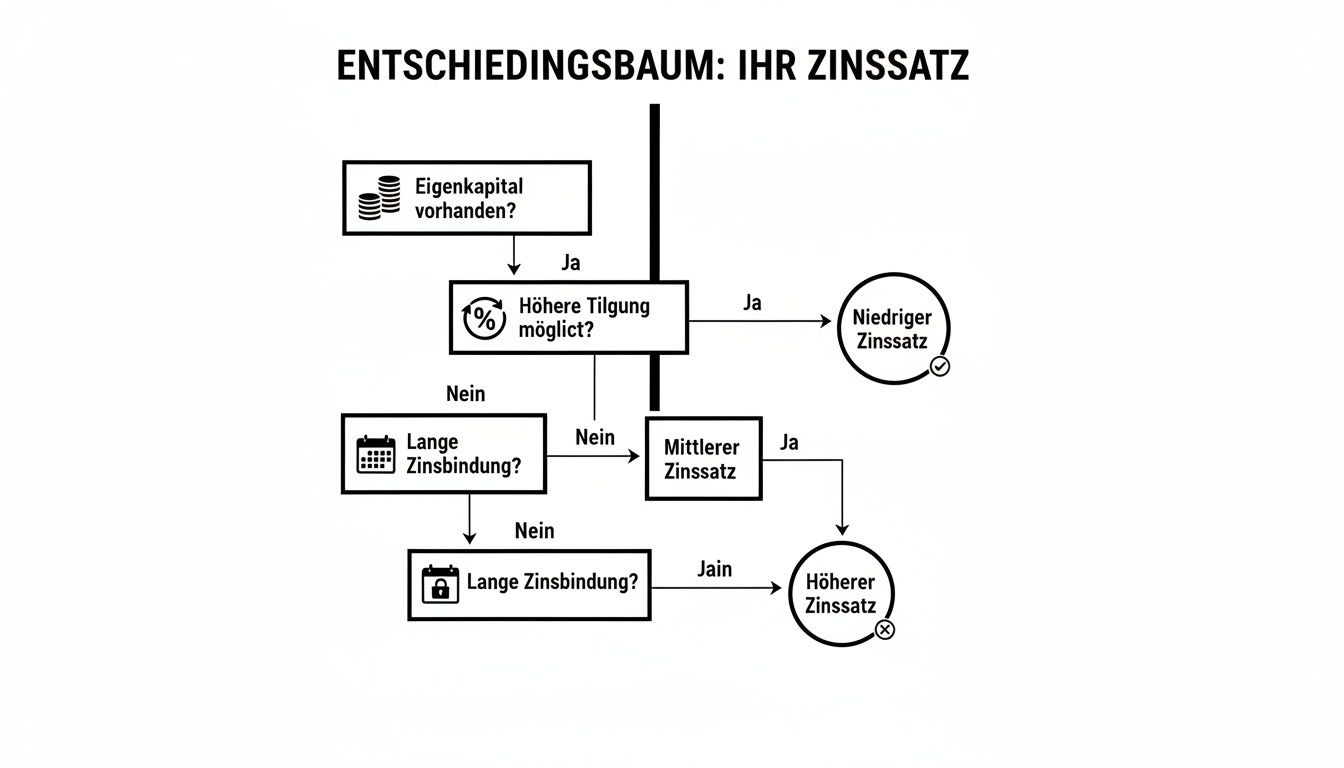

As soon as the first offers arrive, the real detective work begins. Many people make the classic mistake here and just stare at the effective interest rate. But a top offer is much more than that. It is the perfect mix of a fair interest rate and flexible conditions in the small print. Sometimes an interest rate that seems slightly higher at first glance is a far better choice in the long run.

This graphic gets to the heart of the matter and shows the three most important levers banks use to set your interest rate. This is the basis for any good comparison.

You can see immediately that equity, repayment and fixed interest rates are directly intertwined. Together they form the foundation on which your conditions are built.

In order not to lose the overview here, you need a system. A simple comparison table can work wonders when it comes to comparing offers fairly and transparently.

The ultimate checklist for your offer comparison

This table is your most important tool. It forces you to look beyond just the interest rate and evaluate the offers as a whole. Take the time to fill it out carefully for each offer.

Checklist for a comprehensive comparison of offers

| Criterion | Offer A (e.g. house bank) | Offer B (e.g. online provider) | Offer C (via intermediary) |

|---|---|---|---|

| Effective annual interest rate | 3,75 % | 3,85 % | |

| Monthly installment | 1.350 € | 1.375 € | |

| Special repayment option | No free option | Up to 5% of the loan amount p.a. free of charge | |

| Repayment rate change | Not possible | 2x free of charge during the term | |

| Commitment interest | 0.25 % p.m. after 3 months | 0.25 % p.m. after 9 months | |

| Fees (total) | |||

| Residual debt at the end of the fixed interest period |

This structure helps you to recognize the true strengths and weaknesses of an offer and to make an informed, objective decision.

A typical scenario from practice

Let’s imagine the whole thing in concrete terms. You compare offer A and B from the table. At first glance, the situation seems clear: offer A attracts 3.75%, while offer B is 3.85%. Who wouldn’t go for the more favorable interest rate? But, as is so often the case, the devil is in the detail.

Offer B gives you the freedom to repay up to an additional 5% of the loan amount each year – completely free of charge. So if you are expecting a salary increase, a bonus or perhaps a small inheritance, you can massively reduce your residual debt and save thousands of euros in interest costs in the end. Offer A simply does not have this flexibility.

And it gets even better: with offer B, you can adjust the repayment rate twice free of charge. This is an invaluable advantage if life doesn’t go according to plan. Whether it’s parental leave, a job change or an unexpected expense – you can lower your rate temporarily and increase it again later.

A low interest rate is worth nothing if the contract forces you into a rigid corset. Genuine flexibility is often the harder currency than the last tenth of a percentage point in interest rates.

Another sticking point, especially for new builds: the commitment interest. With offer B, you have a full nine months before the bank wants to see money for parts of the loan that have not been drawn down. That’s six months more buffer than with offer A. With the usual construction delays, this can quickly save you hundreds of euros.

In this case, offer B would be the wiser and, above all, safer choice for most people, even if the interest rate is slightly higher. Because this loan adapts to your life – and not the other way around.

To delve even deeper into the matter and sharpen your comparison skills, we recommend our further guide, which explains how a loan comparison is made easy. After all, a systematic approach is and remains the safest way to find suitable financing.

Typical mistakes when comparing interest rates – and how to avoid them elegantly

On the way to owning your own home, you naturally want to do everything right, especially when it comes to financing. But when it comes to comparing interest rates, there are a few classic pitfalls that can quickly turn a dream into an expensive nightmare. The good thing is: if you know them, they are easy to avoid.

Probably the biggest mistake is to blindly trust your own bank. Sure, the advisor has known you for years, but when it comes to mortgage loans, this loyalty is rarely rewarded with the best conditions. The house bank only has its own products on the shelf and simply ignores the huge rest of the market.

A clear comparison, for example via platforms such as Finanz-Fox, often reveals this: Other banks or specialized providers offer significantly better interest rates. Over the years, we are quickly talking about savings of several tens of thousands of euros.

More than just interest: what really matters

Another very human mistake is to only go for the lowest effective interest rate. But a single figure does not make a good offer. Sometimes flexible contract terms are worth just as much – it’s all too easy to overlook them when you’re stubbornly focusing on the percentage.

So take a close look at these crucial details in the small print:

- Special repayment options: Are you allowed to use unexpected money, such as a bonus payment or a small inheritance, to get rid of your debt faster and without penalty interest?

- Repayment rate change: Does the contract give you the freedom to adjust your monthly installment if something changes in your life?

- Commitment-free period: How long does the bank give you to draw down the loan before charging fees? A buffer of 6 to 12 months is worth its weight in gold, especially for new builds.

An offer that is perhaps 0.1% more expensive but allows you to make free unscheduled repayments of 5% per year may end up being the much wiser decision. This flexibility is an invaluable wild card that pays off in the long term.

Fixed interest rates and the invisible costs

A third, often serious mistake: choosing a fixed interest rate that is too short simply because interest rates are low at the moment. If you only commit for five or ten years in order to push the interest rate down one last time, you are taking an enormous risk. If interest rates skyrocket by the end of this period, the follow-up financing will come as a nasty surprise and could blow your entire budget. It is better to secure the good conditions for 15 years or longer.

And last but not least: the ancillary costs. They are almost always underestimated. Notary, land registry, land transfer tax and perhaps the estate agent – these easily add up to 10-15% of the purchase price. This money usually has to come directly from equity. If you plan too tightly here, you run the risk of the entire financing falling through. A realistic calculation of these items is therefore essential. You can find more background information on various financing models in our guide on the art of financing and installment loans.

Frequently asked questions about interest rate comparisons

Anyone looking to compare mortgage interest rates will come across the same crucial questions again and again. That’s quite normal. Here I have summarized the most common points from my consulting experience for you – short, crisp and straight to the point.

When is the best time to compare interest rates?

Start looking around as soon as the idea of owning your own home starts to take shape. I recommend developing an initial feel for the market six to twelve months before you plan to buy or start building. That way you can see where the journey is heading.

Things get really serious four to eight weeks before you have to sign the contract. This is the time to obtain binding, up-to-date offers. A little tip: If you want to secure today’s interest rates for a project in the future, a forward loan could be a clever option. This creates planning security.

The classic mistake? Starting too late. If you’re pressed for time, you tend to accept the first offer that comes along and often overlook expensive pitfalls. Take your time – your financial future is at stake.

Does the location of the property play a role in interest rates?

Yes, absolutely. Where your dream home is located is an important factor for the bank. Banks assess their risk not only according to your personal creditworthiness, but also according to how the real estate market is developing in the respective region. In booming metropolitan areas with stable prices, the risk for the bank is lower.

Why? It’s simple: the property is the collateral for the loan. If it sells well in an emergency, the bank is more relaxed. In structurally weak regions, where prices may even fall, the bank may add a small risk premium to the interest rate. This is why the zip code is one of the first questions in any interest rate calculator.

Can I simply change banks with my current financing?

Theoretically yes, but in practice it is almost never a good idea. If you want to get out of the contract while the interest rate is fixed, the bank will demand a hefty early repayment penalty. This sum is often so high that it wipes out any interest rate advantage with a new provider.

The interest rate comparison only becomes really interesting again towards the end of the fixed interest period. You should start obtaining offers for follow-up financing at least 12 to 24 months before expiry. It is often much cheaper to switch to a new bank than to blindly accept your bank’s renewal offer.

How does an intermediary benefit me compared to going directly to my bank?

Imagine it like this: Your house bank only has its own products on the shelf. An independent broker, on the other hand, has the key to the entire supermarket – he has access to the offers of hundreds of banks, savings banks and insurers.

This gives you decisive advantages:

- You save an enormous amount of time: instead of making dozens of inquiries yourself, you get the most suitable options served up on a silver platter.

- You secure better conditions: The broad market comparison significantly increases the chance of getting the best possible interest rate for your situation.

- You benefit from real expert knowledge: A good advisor knows the tricks, helps you to prepare your application in the best possible way and negotiates with the banks on your behalf at eye level.

You don’t want to search through countless banks yourself, but want to find the best offer from the entire market directly? The experts at Finanz-Fox will do just that for you. Start your no-obligation comparison now at https://www.finanz-fox.de and secure your top conditions.